Collection Accounts on Your Credit Report: The Ultimate Guide

Collections are one of the worst things to have on your credit report. They can damage your credit score significantly for a long time—up to seven years. This helpful guide explains what collections are, how they affect your credit, how collection agencies try to re-age debt, how to get collections removed from your credit report, and more.

What Is a Collection Account?

A collection account is a debt account that has been sold by the original creditor to a third-party debt collection agency. This happens you (the borrower) are delinquent on payments long enough (generally 180 days) for the lender to charge off the loan, which means they consider the account to be a loss—but that doesn’t mean you’re off the hook.

Once the account has been charged off, the original creditor closes your account and often transfers or sells it to a debt collection agency or a debt buyer. (Debt buyers typically focus on purchasing debt accounts and they hire debt collection companies to attempt to collect the debt.)

When Does the 7 Year Credit Rule Start on Your Credit Report?

Regardless of who the debt was transferred to or when it was transferred, the Fair Credit Reporting Act (FCRA) allows collections to legally be reported by the credit bureaus for up to seven years after the date of the first delinquency (also known as “DOFD” for “date of first delinquency”).

The seven-year rule for collections begins on the date of first delinquency.

What does this mean exactly? How do you figure out the date of the original delinquency of an account?

According to Experian, the date of the original delinquency is the first reported late payment. As an example, if you have a 30-day late reported and never catch up on payments, then the delinquency would later get reported as a 60-day late and eventually as a 90-day late.

The seven-year period after which the delinquency falls off begins with the first missed payment, the 30-day late. If the debt is sold to a collection agency, the original account and the collection account will both be removed from your credit report seven years after the initial delinquency, says Experian.

Medical collections are slightly different in that a 180-day grace period must be provided to allow insurance benefits to be applied. Therefore, the seven-year timeline starts after 180 days, not after a 30-day late.

The date that a collection account is charged off or transferred to another company does not change the DOFD and therefore should not change the date that the delinquency falls off of your credit report.

How Often Do Collection Agencies Report to Credit Bureaus?

Collections agencies can begin reporting to the credit bureaus as soon as they acquire your account. After that, they will typically report to the credit bureaus every month, like most other types of tradelines on your credit report. Therefore, if you have a collection account, you will most likely see the collection agency reporting every month.

Should You Pay the Debt Collector or the Original Creditor?

If you already have an account in collections, meaning the original creditor has already closed your account and transferred it to another owner, you should not pay the lender that the loan was originally from. The debt now belongs to someone else, so it would be pointless to pay the original creditor.

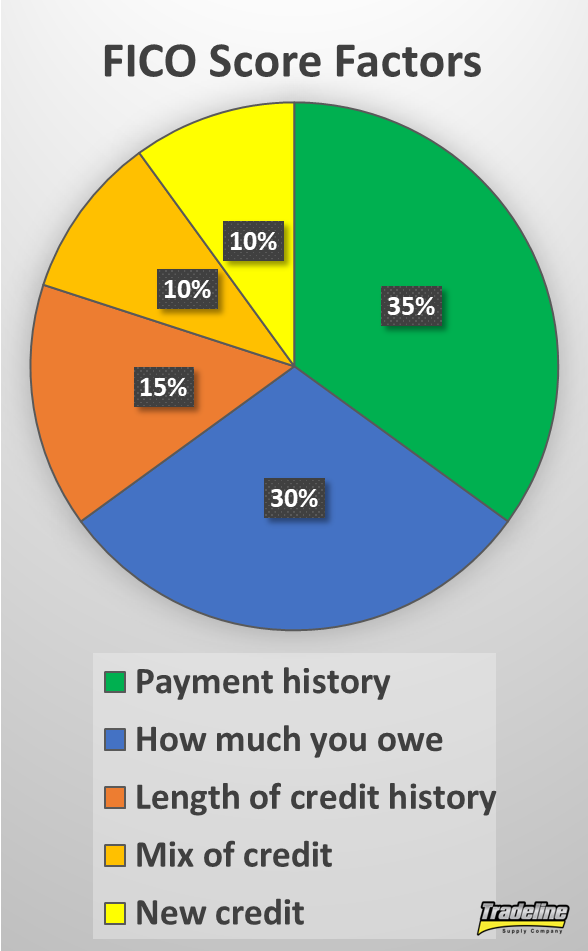

How Do Collections Affect Your Credit Score?

Having one or more collection accounts on your credit report can quickly lead to bad credit. A collection account on your credit report means you failed to make sufficient payments on a debt, which is a big red flag to lenders that you might default on a loan again. Therefore, your credit score will likely suffer a significant drop if you have an account go to collections.

Collections are major derogatories, so they can lead to bad credit. afeCredit.com, CC 2.0.

However, collections with low balances may not impact your score at all, depending on which credit scoring model is being used to calculate your score, such as VantageScore or a FICO credit score.

FICO scores 8 and 9 ignore both paid and unpaid collections that had an original balance of less than $100.

FICO 9, VantageScore 3.0, and VantageScore 4.0 don’t count paid collection accounts against you and treat medical collections as less important than other types of collection accounts.

Unfortunately, with FICO 8 and previous versions of FICO, which most lenders today still use, all collections are highly damaging to your credit score, regardless of what type of account they are or whether the collections have been paid or not.

Does Paying Off Collections Improve Your Credit Score?

Unfortunately, paying off a collection won’t necessarily improve your credit score right away. Why?

As we said, with all FICO scores except FICO 9 (which is not widely used yet), both paid and unpaid collections are considered to be major derogatories on your credit report. Since a paid collection is still a major derogatory mark, paying off your collection likely won’t help your credit score if the scoring model used is FICO 8 or earlier.

On the other hand, since FICO 9, VantageScore 3.0, and VantageScore 4.0 ignore paid collection accounts, your score should rebound after paying off a collection with these credit scoring models.

Can a Collection Agency Change the Open Date of a Collection?

The open date of a collection is the date that the collection account was acquired by a debt collector. Every time the debt changes hands, the new collection account will thus have a new open date.

The open date does not affect how long the collection remains on your credit report because it’s the date of first delinquency (DOFD) that determines when the collection will be removed from your credit. While each debt collector will have a different open date, the DOFD cannot be changed unless it was reported incorrectly.

Can a Collection Agency Report an Old Debt as New?

You may have heard of another date pertaining to collection accounts: the “date of last activity” (DLA).

You might have heard it said that you should never make payments on a collection because that action would change the DLA on the account. If the DLA changes, so the advice goes, this “resets the clock” on the seven-year period after which the collection will fall off your credit.

In reality, debt collectors cannot change the DLA—only the credit bureaus can do that. Furthermore, the DLA does not affect the timeline of your collection account.

As we know, the seven-year period begins at the DOFD, not the DLA, and not the open date of the collection. The collection agencies are not legally allowed to change the DOFD, so there should be no legitimate way for them to “restart” the seven-year timeline. Yet there are many cases in which consumers report that their collection accounts are suddenly being updated as new accounts, even if they are several years old. What is going on in these situations?

This shady practice is the collection agency re-aging the debt.

It’s illegal to re-age a collection account by incorrectly changing the DOFD.

When a debt collector acquires an account, they sometimes improperly update the DOFD to be the same as the date opened. If you make a payment on the collection, they may replace the DOFD with the DLA, which is the date that you made the payment. This explains why the seven-year clock seems to restart in these situations.

But guess what? Re-aging a collection is illegal. Collection agencies cannot legally report an old debt as a new collection.

If a collection agency keeps updating your credit report with incorrect information and the date of first activity or the date opened on your credit report is wrong, you have the right to dispute that account and have it updated or removed from your credit report.

Double Jeopardy Credit Report

A “double jeopardy” credit report is when you have multiple collections for the same account on your credit report. This can happen when the debt is being reported by both the original creditor and the collection agency on your credit report or when the debt is sold to another collection agency.

Experian explains why there may legitimately be duplicate accounts on your credit report:

“When an account is charged off, or written off as a loss, it remains on your credit report for seven years from the original delinquency date leading up to the charge off.

Often, the original creditor will transfer or sell the account to a collection agency. In that case, the original account will be updated to show transferred/closed, and will no longer show a balance owed because the debt is now owed to the collection agency. However, your report will still show the history of the account, including the amount that was written off.

Since you now owe the collection agency, it will report the current balance owed.”

In this case, having multiple accounts for the same collection on your credit report is normal and should not change the impact the collection has on your credit score.

A true case of double jeopardy on your credit report involves duplicate collection accounts on your credit report being reported as open collections, which would be even more of a disaster for your credit than having a single open collection account.

Multiple Collection Agencies Same Debt

If your credit report looks as Experian describes, with the old collection accounts accurately reporting as closed, there may not be much you can do besides wait seven years for the collections to fall off your credit report.

However, if the original creditor and/or multiple collection agencies report the same debt as if they are all separate open collection accounts, that may be an error that you need to dispute with the credit bureaus.

How to Remove Collections From Credit Report

It may be possible to remove collections from your credit report depending on the situation.

How to Dispute a Collection on Your Credit Report

If a collection on your credit report is inaccurate or a duplicate collection account, you can dispute the collection account on your credit report. This doesn’t necessarily guarantee that the collection will be removed from your credit report, though, because the account could be updated with the correct information rather than removed.

The Federal Trade Commission provides a guide to disputing errors on credit reports as well as a sample FCRA dispute letter. Alternatively, some consumers may prefer to hire a credit repair service to assist with disputing inaccurate information.

How to Remove Paid Collection Accounts From Credit Report: Pay for Delete Collections

Even once you have paid a collection, you may find that it is difficult or impossible to remove it from your credit file. However, if you do want to try to remove zero balance collections from your credit report, one method that consumers use to do this is the “pay for delete” strategy.

You may be able to negotiate a “pay for delete” agreement with the debt collector.

With the pay for delete method, you negotiate with the debt collector to have them stop reporting the collection to the credit bureaus in exchange for your payment, whether you negotiate to pay the full amount owed or settle the debt for a lesser amount.

It may not be necessary to hire a pay for delete service, since you can look for a sample pay for delete letter online, although a credit repair service might be helpful in this situation as well.

Keep in mind that debt collectors are not obligated to accept the offer outlined in your deletion letter, so this strategy is not a guaranteed success.

If the collection agency does agree to delete the collection once you pay it off, it’s best to get verification of this agreement in writing before you make any payments.

Does Pay for Delete Increase Credit Score?

Remember that FICO 9, VantageScore 3.0, and VantageScore 4.0 don’t penalize paid collections, so it may not be a problem to have a paid collection on your credit report if your lender uses one of these credit scores. In this case, the deleted collection won’t increase your credit score.

However, with FICO 8 and earlier FICO scores, paid collections do hurt your credit, so a successful “pay for delete” arrangement could lead to a credit score increase after collection removal.

On the other hand, you may be shocked to learn that it is possible that deleting a collection could actually make your credit score go down. This is because there are certain scorecards or “buckets” within each credit scoring model that categorize consumers based on what is in their credit file and calculate their score differently depending on what bucket they are in.

As a hypothetical example, let’s say you have one collection on your file and you get that collection deleted. Perhaps you used to be in a scorecard of consumers with one or more major derogatories on file and after the deletion, you get reassigned to a different scorecard in which the consumers have no major derogatories. Since you are now in a higher bucket, your credit score would be calculated differently, and your score could actually decrease compared to what it was when you were in the lower bucket.

How to Remove Collections Without Paying

The only legitimate way to get an unpaid collection removed from your credit report is if the collection is more than seven years old or if it is being reported incorrectly.

If the collection is older than seven years, it should have been removed from your credit report already, so you can dispute that account with the credit bureaus to have it removed.

If the account is being reported inaccurately, such as if the date of first delinquency or the date opened on your credit report is wrong, you can also dispute the account and have it updated or removed as described above.

Conclusions on Collections

If you have a collection account on your credit file, you might end up with bad credit for a while, but it’s not the end of the world. Collections must be removed from your credit file after seven years whether they were paid or not, and the damage to your credit score will lessen as the collection ages.

Some credit scoring models don’t count paid collections against you, so you might see a credit score increase after paying off a collection. Alternatively, you could try to negotiate a pay for delete agreement with the debt collector.

If you have an old or inaccurate collection on your credit report, you can dispute this with the credit bureaus and have it corrected or removed.

Finally, the best thing to do to help your credit recover after a collection is to focus on building credit and maintaining a positive credit history going forward.

Read more: tradelinesupply.com

If you have credit cards with low credit limits, you may be interested in increasing your credit limit. In this article, we’ll talk about why your credit limit is important, reasons to increase your credit limit, when and how to request a credit line increase, and more. Keep reading for everything you need to know about how to increase your credit limit.

If you have credit cards with low credit limits, you may be interested in increasing your credit limit. In this article, we’ll talk about why your credit limit is important, reasons to increase your credit limit, when and how to request a credit line increase, and more. Keep reading for everything you need to know about how to increase your credit limit.

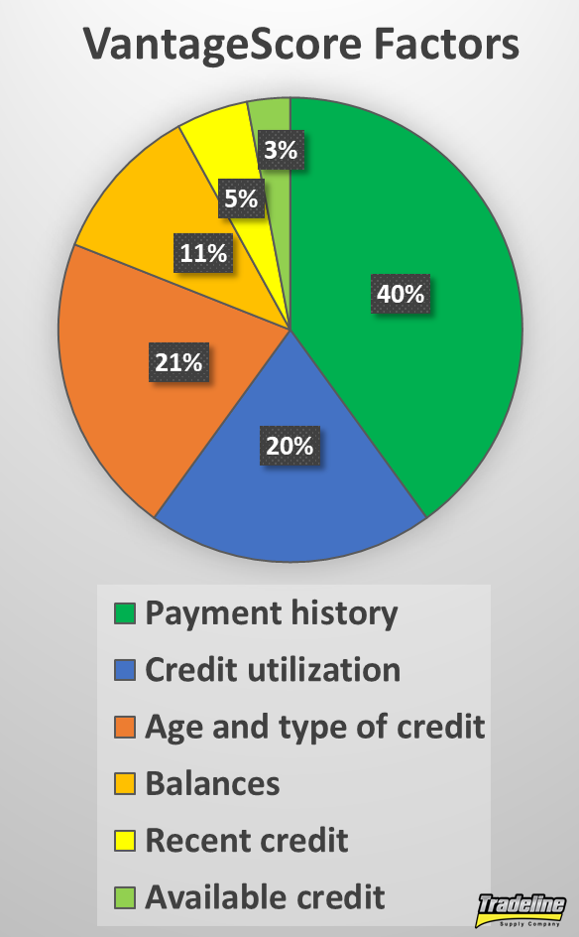

When it comes to credit scores, there’s a lot of confusion and misinformation out there. Our credit scores impact our lives in more ways than you might think, yet, unfortunately, they are complicated and difficult to understand. In this article, we’ll clear up what credit scores are, why they matter, how to build credit, and how to improve your credit score.

When it comes to credit scores, there’s a lot of confusion and misinformation out there. Our credit scores impact our lives in more ways than you might think, yet, unfortunately, they are complicated and difficult to understand. In this article, we’ll clear up what credit scores are, why they matter, how to build credit, and how to improve your credit score.