Easy Credit Hacks That Will Actually Get You Results

Credit repair can be a long and arduous process, especially if you have very bad credit. Getting results from credit repair can take months, and it takes years to build or rebuild a solid credit history.

However, there are some “credit hacks” that you can use to improve your credit on a much shorter time scale.

In this article, we’re going to tell you the best credit hacks to improve your credit score as well as credit card hacks that work to help you save you money on interest. In addition, we’ll also provide some credit-building hacks for those with thin credit files and credit repair hacks to help you fix bad credit.

Here are the credit hacks we’ll be covering in this article. You can click on the bulleted list items below to jump directly to each hack.

Pay down high-balance cards first to improve your credit utilization

Pay off low-balance accounts to reduce the number of accounts with balances

Time your payments so that you have a $0 balance on your statement date

Build credit fast by piggybacking on someone else’s good credit

Consider applying for a credit-builder loan

Increase your credit limit

Ask your credit card issuers for lower interest rates

Set up automatic bill payments

Pay down high-interest balances first to save money on interest and pay off debt faster

Transfer your balance to a card with a lower interest rate

Dispute inaccurate information on your credit report (such as inquiries or derogatory items)

Delete collections from your credit report

Time your credit inquiries carefully when shopping for credit

Get a rapid rescore from your mortgage lender

Manually update your credit report yourself

Now let’s delve deeper into each credit of these credit hacks.

Credit Score Increase Hacks

Pay down high-balance cards first to improve your credit utilization

If your focus is primarily on boosting your credit score fast, you may want to consider paying down your high-balance cards first. The reason for this can be explained by the importance of individual credit utilization ratios, which refers to the utilization ratios of each of your revolving accounts.

From what we have seen, individual utilization ratios may be even more important than your overall utilization ratio. Having one or more maxed-out accounts, for example, can drag down your score even if your overall utilization ratio is low.

Therefore, by paying down your high balances first, you can get those accounts out of the high-utilization danger zone and into a utilization range that is less damaging to your credit score.

Pay off low-balance accounts to reduce the number of accounts with balances

One of the factors that are considered within the overall “credit utilization” category is the number of accounts that have balances. Having fewer accounts with balances is better for your score. In fact, the ideal credit utilization scenario is having a zero balance on all but one of your accounts and having one account with a utilization ratio in the 1-3% range.

Therefore, if you can pay some of your accounts down to zero, you should see a boost to your score. Accounts with small balances are low-hanging fruit because you don’t have to spend as much money to get them to a zero balance.

You can read more tips on how to improve your credit utilization in our article about utilization ratios.

Time your payments so that you have a $0 balance on your statement date

To ensure that your credit report shows low credit utilization, time your payments so that you have a low balance (or no balance) when your accounts report to the credit bureaus.

When it comes to credit utilization, you might think that as long as you pay your credit card balance in full by the due date every month, then you should show a 0% utilization for that account. However, this assumption is not necessarily correct. The reason for this is that the date when your credit card issuer reports to the credit bureaus is often not the same as your due date.

That means that your account is reporting at some other time during the month when your card does have a balance on it. If you use a significant portion of your credit limit, that utilization could be hurting your score.

To correct this, if you want to have your accounts show a 0% utilization ratio, try using this credit hack: Instead of waiting for your statement to arrive and then paying your balance on the due date a few weeks later, you need to pay your balance to $0 before the statement closing date. Then, your statement will close with a $0 balance and that’s what will report to the credit bureaus.

Alternatively, you can pay your bill on your normal schedule and then refrain from using your card for the next entire billing cycle. Since you have paid off the balance and not made any new charges, your account will show a $0 balance at the end of the reporting cycle.

Either way, if you can shift the timing of your payments so that your account reports a 0% utilization, that could provide a significant benefit to the credit utilization portion of your credit score.

Credit-Building Hacks

Build credit fast by piggybacking on someone else’s good credit

One of the easiest and fastest ways to build credit is called credit piggybacking, which refers to the practice of becoming associated with someone else’s good credit for the purpose of helping you build your own credit history.

Piggybacking credit can help you build credit quickly, whether you open a joint account, get a cosigner, or become an authorized user.

There are three main ways to piggyback credit.

Get a co-signer or guarantor

Having a co-signer or guarantor with good credit can go a long way toward helping you qualify for credit because the co-signer or guarantor is essentially promising to assume responsibility for the debt if you default.

The downside of this strategy is that since the position of the co-signer or guarantor comes with a lot of risks, it can be difficult to find someone to take on this role for you.

Open a joint account

Since both applicants are considered when opening a joint account, you can benefit from your partner’s good credit as well as the fact that the income of both applicants can be counted. If you maintain the joint account for a while, this can allow you to build up a credit history with a primary account.

However, many banks no longer offer joint credit cards, so your options for opening a joint account may be limited. Plus, if your relationship with the other account holder ever takes a turn for the worse, it can make managing the account difficult, and you may end up needing to close the account altogether.

Become an authorized user

Becoming an authorized user on a seasoned tradeline (i.e. a credit account that already has at least two years of positive payment history associated with it) is the fastest way to build credit. Instead of opening your own primary account and waiting for it to age, you can add years of credit history to your credit profile within a few weeks or even days.

Consider applying for a credit-builder loan

If you have bad credit or if you have never used credit before, you might be feeling discouraged about the prospect of getting credit anytime soon. It can feel impossible to get credit if you have a thin credit file or a history of derogatory marks on your credit report.

A credit-builder loan can be a useful tool for those struggling to build credit. Here’s a summary of how they work:

Credit-builder loans are typically for small amounts (e.g. a few hundred to a thousand dollars).

A credit-builder loan functions like a backward version of a traditional loan: instead of receiving the funds upfront and paying the money back later, you first make all of the monthly payments and then receive the loan disbursement once you have already paid off the loan.

For this reason, these types of loans are low-risk for lenders, which is why even those with bad credit or thin credit can still qualify (provided your income is sufficient for you to make the monthly payments).

The lender reports your payment history to one or more of the major credit bureaus, which allows you to build a credit history.

For more information on how these loans work and whether a credit-builder loan might be a good strategy for you to consider, check out our article, “Credit-Builder Loans: Can They Help You?”

Credit Card Hacks

Increase your credit limit

Increasing your credit limit is one of the best credit hacks. Check out our article for more tips on how to request a credit line increase.

Increasing your credit limit can be one of the easiest and fastest ways to boost your credit score. However, you’ll want to strategize a little before requesting credit line increases from your lenders.

You can read more in our article on the topic, but here’s a quick rundown of how to increase your credit limit:

If your financial situation has improved since opening your credit cards, it might be a good time to request a credit line increase. For example, if you have received a raise at work or your credit score has increased, that could indicate to lenders that you can handle a higher credit limit responsibly.

Wait until you have been a responsible cardholder for at least six months and you don’t have too many inquiries on your credit report to make your request. Also, don’t request an increase if you have already requested one within the past six months.

Check with your credit issuer to see whether they will need to do a hard inquiry or soft inquiry. If you don’t want to get a hard inquiry on your credit report, ask if there is an amount they may be able to approve without doing a hard pull on your credit.

You can make your request for a credit limit increase online or over the phone. Be prepared to provide some financial information and to explain why you are asking for additional credit. Calling your bank and talking to a representative may give you more opportunities to negotiate than if you make the request online.

So, how does this hack improve your credit score?

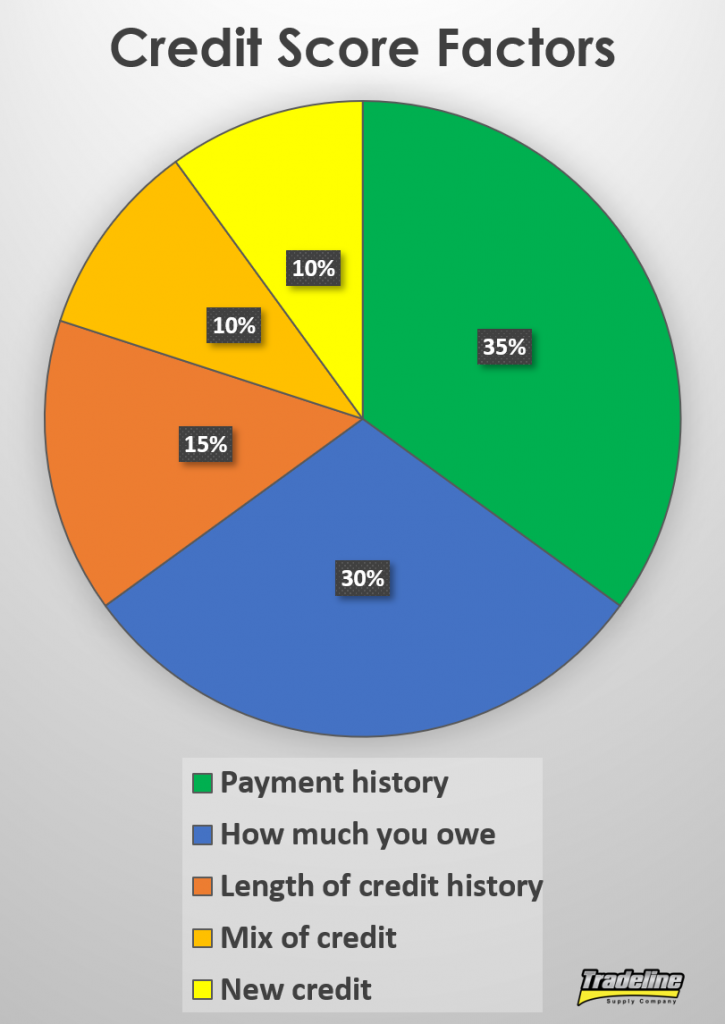

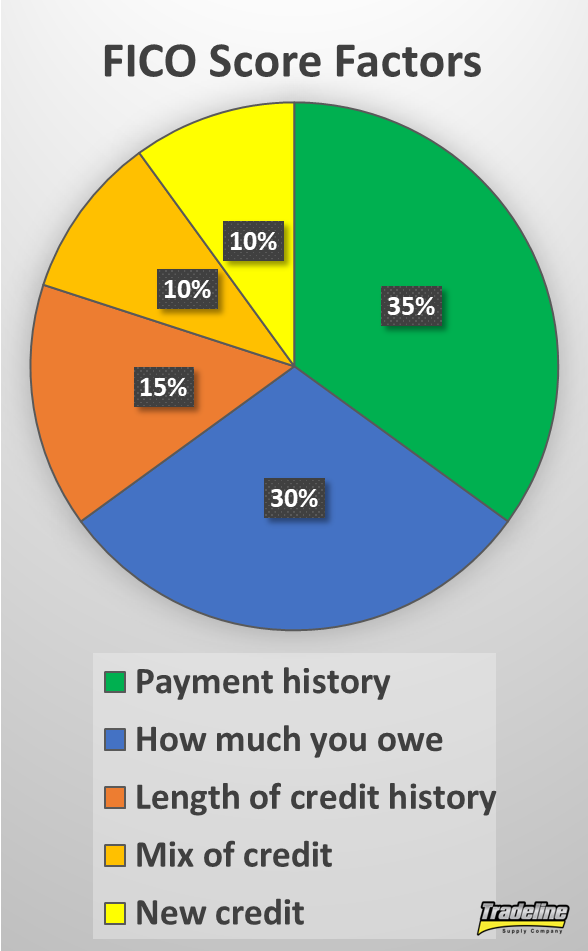

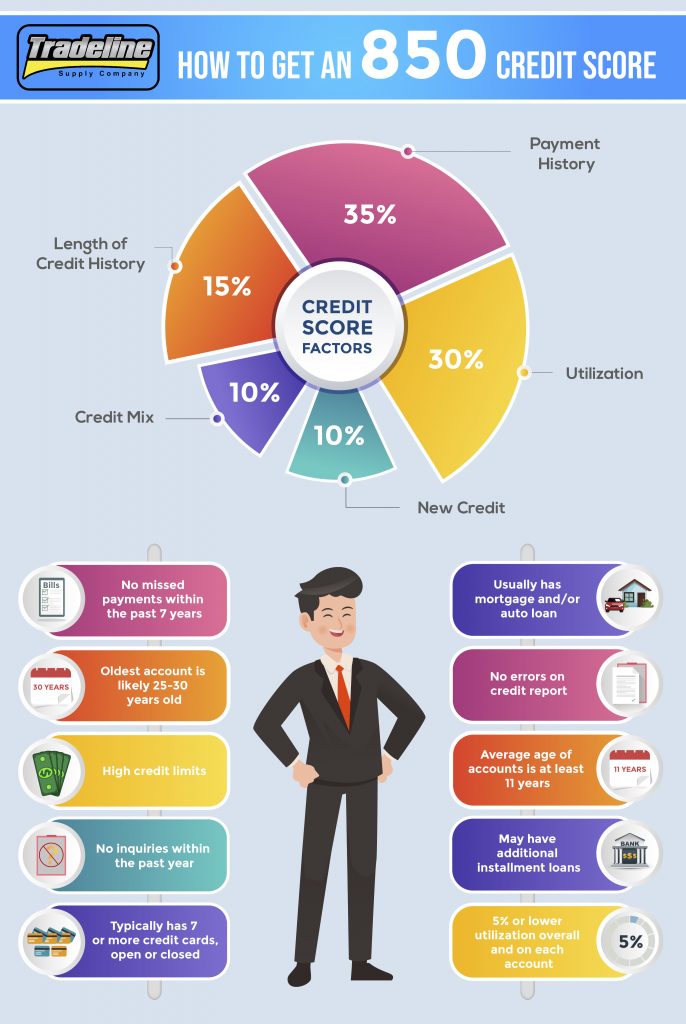

Your credit utilization ratio, also called your debt-to-credit ratio, makes up about 35% of your FICO score and about 20% of your VantageScore. It’s defined as the ratio of how much debt you owe to the amount of credit you have available. This can be calculated for your revolving credit accounts in aggregate by adding up all of your balances and dividing by the sum of all your credit limits for those accounts.

Increasing your credit limit improves both your overall and individual utilization ratios, thus helping your credit score.

Ask your credit card issuers for lower interest rates

This is another credit card hack that is easier and quicker than you might think. All you need to do is call up each of your credit card issuers and ask them to lower your interest rate.

Try calling your credit card issuers and asking for lower interest rates—odds are good that they will grant your request.

Again, you’ll want to do a little homework before asking for a lower interest rate. Research interest rates on cards from other issuers and see if your bank can match a lower number. Explain why you’ve been a good customer and why you feel your rate should be lowered. Also, describe how your financial situation may have improved since you opened the card.

You can find a detailed script to help you negotiate on creditcards.com.

Although this tip doesn’t directly affect your credit score, it can still be hugely beneficial, especially if you are one of the 37% of American households that carry balances on their credit cards from month to month.

Lowering your interest rate decreases the debt burden that comes from interest charges each month, allowing you to pay off your debt faster. Paying off your debt faster means improving your utilization ratio, which leads to a better credit score!

Although this hack isn’t guaranteed to work, the worst that could happen is that your lenders deny your request and your interest rates stay the same. On the other hand, it could save you hundreds or even thousands of dollars in interest. Plus, you can be optimistic about your chances: polls show that over three-quarters of consumers who ask for a lower interest rate are successful in their request.

Set up automatic bill payments

Setting up automatic payments is one of the best things you can do for your credit, especially if you struggle to remember due dates or if you have accidentally missed payments in the past. Payment history is the number one factor that influences your credit score, so even one late payment can have a serious impact on your credit.

Setting up automatic payments for all of your accounts can help prevent you from accidentally missing a payment.

Take human error out of the equation by setting up automatic payments for all of your loans and credit cards. That way, you’ll never accidentally miss a payment, so you can continue to build up a positive payment history each month without even thinking about it.

Pay down high-interest balances first to save money on interest and pay off debt faster

When it comes to paying off debt, the way to save the most money on interest is to pay off your high-interest balances first. This method is called the “debt avalanche” because you’re starting with the highest interest rates and working your way down from there. (In contrast, the “debt snowball” method involves paying your debt in order of smallest to largest balances).

As with the previous hack, by saving money on interest, you can chip away at your credit card debt faster, decreasing your credit utilization and increasing your credit score.

Transfer your balances to a card with a lower interest rate

Another popular way to get some relief from paying those astronomical interest charges every month is to transfer your credit card balances to another credit card that has a lower interest rate.

This hack works best if you have good enough credit to qualify for a balance transfer credit card. These credit cards are marketed specifically for this purpose and they typically come with special introductory offers, such as 0% APR on balance transfers for a certain number of months.

A balance transfer can help you save money on interest charges and may improve your credit utilization ratio.

Here’s how the balance transfer process works:

When you apply for the balance transfer credit card, you tell the credit card issuer the amount you want to transfer and which bank(s) you want to transfer a balance from.

Once you have been approved for the balance transfer card, the credit card issuer essentially pays off your balances at the other banks with the credit on your new card.

Your debts (plus a balance transfer fee, usually around 3-5%) have thus been transferred to your new card.

Since your balance transfer card likely has a low promotional interest rate or perhaps even zero interest for a while, you have some extra time to pay off your debt without being crushed by interest, which means you can pay off your debt faster.

As a bonus, this credit card hack can also help your credit utilization, because you are adding some available credit to your credit profile by opening a new account.

The pitfall to watch out for with this method is that it opens up the possibility of you running up your credit cards again and potentially ending up even deeper in debt than you were before. If you think having access to additional credit is going to tempt you to spend more, then it’s probably best for you to avoid this credit hack.

Credit Repair Hacks and Bad Credit Hacks

Dispute inaccurate information on your credit report (such as inquiries or derogatory items)

Check your credit report for errors that could be damaging your score and dispute them with the credit bureaus.

If you have any errors on your credit report that are bringing your score down, such as credit inquiries or derogatory items that don’t belong to you or are otherwise being reported incorrectly, then this hack could definitely give your credit a boost.

First, you need to obtain a copy of your credit report to check for errors. You can order one from each of the three credit bureaus for free once a year at annualcreditreport.com and you can order your Innovis credit report for free directly from their website.

Then, thoroughly check your credit report for any inaccuracies, such as late payments that you actually made on time, duplicate accounts, or negative information that is more than seven years old (which means it should have been deleted by the credit bureaus already).

To fix the errors on your credit report, you can dispute the items with the credit bureaus by following the instructions found on each of your credit reports. However, there are a couple of other things you should keep in mind in order to ensure your dispute process goes smoothly.

Look up a sample credit dispute letter, such as the sample letter offered by the Federal Trade Commission, that you can use as a model for writing your own letters.

Write one dispute letter for each credit report error and send in your letters one at a time. If you try to dispute several items at once, you run the risk of the claim being dismissed as “frivolous.”

Be sure to include as much evidence as possible that supports your claim when submitting your dispute. Without documentation proving that the item is being reported incorrectly, the credit bureaus could dismiss your dispute.

Send your letters along with the necessary documentation via certified mail so that you can get proof that the bureaus received them.

In addition, you should also talk to the creditor that is reporting the inaccurate date to the credit bureaus in order to fix the problem at the source and prevent the error from showing up on your credit report again in the future.

Once the credit bureaus receive your dispute letters, they have 30 days to investigate the issue. If they cannot verify the information to be accurate, then they have to either update the item with the correct information or remove the item from your credit report.

For more information on the types of credit report errors to watch out for and how to fix them, see “How to Fix the Most Common Credit Report Errors.”

Delete collections from your credit report

For this credit hack, dispute collection accounts on your credit report that are inaccurate or outdated to have the credit bureaus update them or delete the collections altogether.

If you have collection accounts on your credit report, it may be possible to get them deleted, depending on the circumstances.

As we discussed above, if a collection account on your credit report is being reported incorrectly or doesn’t belong to you, then you can certainly dispute the inaccurate information and have the credit bureaus update or remove the item.

If, on the other hand, the collection accounts on your credit report are legitimate, then your options for removing them are limited.

Some consumers try to negotiate a “pay for delete” arrangement with the debt collector, in which the debt collector agrees to stop reporting the collection to the credit bureaus in exchange for you paying some or all of the debt. However, this strategy is risky and it does not always work in the consumers’ favor. If you do try this approach, be sure to get the agreement in writing from the collection agency.

In addition, deleting a paid account might not even increase your credit score depending on which credit scoring algorithm is being used. Simply paying the collection may be enough to boost your credit score, since some scoring models (FICO 9, VantageScore 3.0, and VantageScore 4.0) don’t penalize you for having paid collections on your credit report.

If you want to delete a collection account without paying it, unfortunately, your only legitimate option is to wait for the collection to be removed from your credit report automatically, which happens seven years after the date that you were first delinquent on the account.

If you’re concerned about collections on your credit report, definitely make sure to check out our ultimate guide to collection accounts.

Credit Report Hacks

Time your credit inquiries carefully when shopping for credit

If you’re planning to shop for credit in the future, you’ll probably be getting some hard inquiries from lenders on your credit report.

Lenders typically need to check your credit history before they can decide whether or not to extend you credit, so when you apply for a loan or credit card, the lender will often request a “hard pull” of your credit report from one or more of the credit bureaus.

While it’s unlikely that inquiries alone will ruin your credit score, since each inquiry can potentially subtract a few points from your credit score, it is still important to be mindful of the frequency and the timing of your credit applications in order to minimize the impact of inquiries on your credit report.

Thankfully, though, you can still shop around for the best loan without being punished by the credit scoring algorithms. FICO and VantageScore know that it’s financially smart to shop for the best rates, not risky. Therefore, they each have ways of accounting for this behavior so that your loan applications don’t have an outsize impact on your credit score.

When applying for credit, try to minimize the impact of credit inquiries by grouping your applications within a specific time frame.

FICO scores group together inquiries that occur within a certain time frame for student loans, auto loans, and mortgages. Older FICO scores allow a 14-day window for consumers to apply for multiple loans of the same type (such as mortgages), while newer FICO scores allow a 45-day window.

Each inquiry for the same type of loan within the given time period gets grouped together and only counted as a single inquiry. However, note that this rule does not apply to credit cards, for which each inquiry will be counted separately.

With VantageScore, all inquiries that are made with a 14-day period are grouped together, regardless of the types of accounts—even credit cards.

To simplify this information into a general rule, if you can complete all of your hard credit inquiries for a given type of loan within 14 days of each other, then the inquiries will be grouped together and you can avoid ending up with way too many inquiries on your credit report.

Get a rapid rescore from your mortgage lender

Once you’ve tried some of these credit hacks and optimized your credit report, the fastest way to see your results reflected in your credit score is to get a rapid rescore. For those who are about to apply for a mortgage but need to quickly update their credit report first, a rapid rescore can be an extremely valuable tool.

Find out more about rapid rescores in “This Is How a Rapid Rescore Can Boost Your Credit Score Fast.”

Manually update your credit report yourself

To trigger a manual update of your credit report, obtain verification of your tradeline’s new status from your creditor and then forward the letter to the credit bureaus.

Since rapid rescores can only be provided by mortgage lenders, if you’re not in the market for a mortgage but you need to update your credit report in a hurry, you’ll need to update your tradelines manually.

To do so, once you have made the desired changes to your tradelines (e.g. paying down your balances or correcting errors), contact your creditors and ask them to send you a letter verifying the new account information. Then, forward this letter to the credit bureaus so they can update the information in your credit report.

By initiating the update manually, you can bypass the period of time that you would otherwise have to wait until your next reporting period.

Conclusions on Hacks to Improve Your Credit

While there is no substitute for the time and effort required to establish and maintain a respectable credit history, that doesn’t mean that you can’t try some of these credit-boosting hacks to help you improve your credit right away and perhaps even save some money on credit card interest and fees.

Just make sure not to lose sight of the most important goal, which is to build good credit over time and keep your credit report in good condition long-term.

Let us know what you think of these credit hacks! Which are the best credit hacks in your opinion? Do you have any creative credit hacks that you would add to this list?

Read more: tradelinesupply.com

Many people are uncertain about what may happen to their credit when they get married and what can happen to their credit if they get divorced.

Many people are uncertain about what may happen to their credit when they get married and what can happen to their credit if they get divorced.

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast. Derogatory items on your credit report can be a big problem for your finances. These negative marks can stay on your

Derogatory items on your credit report can be a big problem for your finances. These negative marks can stay on your