Common Mistakes Made When Buying Tradelines

Use our list of common mistakes below to make sure you get the most out of your authorized user tradelines. Don’t make the same mistakes we’ve seen before!

1. Having fraud alerts or credit freezes on your account

If you have fraud alerts or credit freezes on your account, new tradelines simply will not post on your credit report.

Fraud alerts essentially freeze your account, so new information cannot be added. If you have fraud alerts on your credit file, you must contact each credit bureau directly to have the fraud alerts removed before you will be able to add new tradelines to your file.

2. Not knowing how tradelines work

The most important factor in purchasing tradelines, in our opinion, is to understand how tradelines work. Without this understanding, it is easy to let commissioned salespeople lead you astray and sell you tradelines that are not the best for your particular situation.

If you are new to tradelines, then be sure to check out our Tradelines 101 infographic for a crash course on the basics as well as the large library of educational articles in our Knowledge Center.

3. Not understanding how credit scores work

Before buying tradelines, it is vital to have a general understanding of how your credit score works. There are tons of useful resources online that can walk you through what factors affect your credit score, such as our guide to building credit with tradelines. Knowledge is power, and understanding how credit scores work is worth the investment since your credit score can affect everything from your finances to your job.

The power of a tradeline does not necessarily depend on its price tag.

4. Judging the power of a tradeline strictly by price

When buying tradelines, putting price first is not wise. It is easy to assume that the more expensive a tradeline is, the more powerful it is, but this is not always the case.

For example, someone with a very established credit profile might look at a $1,000 tradeline and just assume that it is the one they want. However, if that $1,000 tradeline does not significantly improve their current average age of accounts or lower their already low utilization ratios, it may not have very much of an effect, or it could even hurt their credit!

Simply adding more of what you already have is not necessarily an improvement. Our Tradeline Calculator is the perfect tool to calculate where your numbers currently stand and how they may be affected by new tradeline data. Make sure to only select tradelines that will actually help you.

5. Not realizing that the power of a tradeline is always going to be relative to what is in your credit report

The power of tradelines is always going to be relative to what is already in your credit file.

For example, if your average age of accounts is already 10 years old, an 8-year-old tradeline may not necessarily help you very much, since you are not improving that variable.

On the other hand, if someone’s average age of accounts is only 1.2 years old, an 8-year-old tradeline may be more powerful for that person. Tradelines do not affect people in the exact same way because everyone’s credit file is unique.

For more information on choosing the best tradelines for your particular situation and goals, our buyer’s guide to choosing a tradeline is a valuable resource.

6. Relying strictly on buying tradelines

It is not smart to rely only on purchasing authorized user tradelines when building or rebuilding credit. In general, tradelines that you can purchase are usually authorized user positions on credit cards, which are revolving accounts.

While this can be very powerful, almost all credit scoring models will take into account your total mix of credit, and it is more favorable to have a good mix of different kinds of credit accounts.

Some additional examples of different types of credit accounts may include auto loans, mortgage loans, installment loans, etc. Having a good mix of credit types is ideal. For more detailed information on how to optimize your credit mix, check out our article, “Credit Mix: Do You Need to Care About Types of Credit?“

In addition, if your credit report has delinquencies such as collections or late payments, tradelines may not solve your problems. You may need to consider repairing your credit before adding tradelines or in tandem with your tradeline strategy. [Disclosure: This article contains affiliate links.]

The age of a tradeline, also referred to as “seasoning,” is often even more important than its credit limit.

7. Valuing limit more than age

Many people initially focus only on how large of a credit limit a tradeline has. They often think that the tradeline with the largest credit limit is automatically the best tradeline.

For example, they might ask, “Should I get the $30,000 tradeline, or do you think the $20,000 one is enough?” However, this question is flawed from the start.

While there may be some validity to this strategy, we feel that a tradeline’s age is even more important than its credit limit, as we discuss in detail in our Tradeline Buyer’s Guide, “Why Age is the Most Valuable Factor of a Tradeline“, and “The #1 Secret on How to Unlock the Power of Tradelines.”

As a real-life example, it is not uncommon for someone to open a new credit card (possibly with a high limit) and that person’s credit score drops initially. Perhaps the reason the person’s score goes down is a new account has no payment history and may pose a higher risk in the eyes of the credit bureaus until a pattern of on-time payments is established. In this example, a new high-limit primary account actually made their credit score go down initially.

It could be the case that a tradeline with a $1,000 limit is actually the best for them because maybe that one has a lot of age and meets their strict budget. Everyone should consider the age and the limit together when buying tradelines and use the Tradeline Calculator as the first step in assessing your situation.

8. Buying cheap tradelines as a test

Some people will use the strategy of buying a cheap tradeline to see what that does first, and if it works a little, then they will buy a better one next time. We feel this strategy is a mistake.

For one, it ends up costing more in the long run, because now they have to buy two tradelines (one cheap one and one better quality one) when the person would probably be better off just getting one high-quality tradeline to begin with.

Also, buying that cheap tradeline may be working against the goal of improving the average age of accounts because in general, cheap tradelines do not have very much age. So when you add a tradeline with little to no age and then later add a tradeline with age, the first tradeline with little to no age ends up lowering the average age of accounts, thus making it more difficult to improve that average.

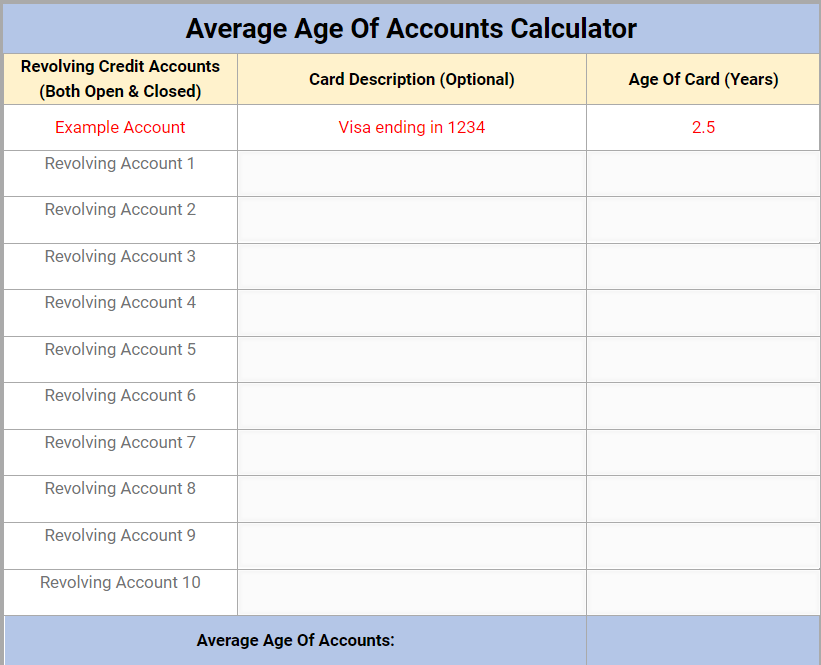

![]()

Calculating your average age of accounts is crucial when choosing the best tradelines for your credit file.

9. Not doing the math on the average age of accounts

You would be surprised to find how difficult it is to significantly change an average, especially when there are multiple accounts in the equation.

As an experiment, imagine there are 5 accounts that are all 2 years old so the average age of accounts is 2 years old. Now guess how old a new 6th account would have to be in order to make the average age of accounts be 5 years old. (Take some time to guess this answer.)

The answer: 20 years old! Seriously, do this math. 2 + 2 + 2 + 2 + 2 + 20 = 30 divided by 6 accounts = 5 years average age of accounts. The easiest way to do the math for yourself is by using our Tradeline Calculator.

Even most “experts” at other companies do not do this math correctly and often guess wrong, and therefore give bad advice to customers as to which tradelines to buy.

10. Not getting old enough tradelines

If you look at the example above, you will see how easy it is to underestimate how old of a tradeline you may really need in order to significantly improve your average age of accounts. Age is essential. Do not underestimate how difficult it is to significantly change an average. Use the Tradeline Calculator to know for sure.

11. Not buying your tradeline far enough in advance before the reporting date

When you place an order for a tradeline, there is a processing time in order for the tradeline company to receive the funds. For example, with our eCheck payment method, it may take up to 5 business days to receive the funds.

Then, the credit partners have up to two days to add the authorized user. The credit card company may then have their own processing time for updating their records internally. Next, the banks update the credit bureaus, and finally, the credit bureaus publish their records.

For this reason, our “Purchase By Date” is typically around 11 days prior to the beginning of the reporting period. So as long as you purchase the tradeline by the Purchase By Date, we guarantee that your tradeline will post in the next reporting cycle.

12. Urgently needing a tradeline to post, but only buying one tradeline and betting your entire outcome on that one posting

Our posting success rate is the highest in the industry, but even given this fact, credit report data is not always going to be perfect.

In other words, although rare, non-postings do occur, and if you are betting your entire outcome on the results of one tradeline, you may want to consider hedging your bets and buying two tradelines to be safe.

Not to mention that buying two may provide better results anyway. Plus, we offer package deals where you can get 10% off your second tradeline, 20% off your third, and 30% off your fourth.

In short, two is often better than one for many reasons. If it is extremely critical to get a tradeline to post, it is safer to just buy two.

13. Buying tradelines instead of paying down your debt

If you have credit cards with high utilization, it is usually best to pay those debts down before buying tradelines.

Having credit cards with high utilization ratios is a negative factor in your credit report. This negative factor will always play a part in your overall credit picture as long as it exists.

The only real way to solve this problem is to pay down your credit cards. You should do the math using our Tradeline Calculator to see where your money is better spent, but in general, paying down your debt is usually the best advice.

14. Thinking tradelines will fix high utilization

Tradelines should not be thought of as the solution to high utilization on your credit cards. While tradelines can affect your overall utilization ratio, having individual cards with high utilization will still be a factor in your overall credit picture.

In other words, you should not only take into account your overall utilization ratio, but also the individual utilization of each of your credit cards and the number of cards that have high utilization vs. low utilization. Again, the solution to the problem is paying your cards down.

For more details on the variables of credit utilization and how tradelines come into play, check out “What Is the Difference Between Individual and Overall Utilization?”

15. Not factoring in closed accounts when calculating your average age of accounts

Many credit scoring models factor closed accounts into their equation. For example, some people with zero open accounts can still have a good credit score. Clearly, the closed account data is still part of the equation.

Therefore, it is wise to factor in your closed accounts when calculating your average age of accounts.

16. Not getting an extension if you need one

If you end up needing your tradeline to stay active on your credit report for longer than two reporting cycles, you don’t have to buy a whole new tradeline when the time is up. We offer unlimited extensions in 1-cycle increments at half the cost of the original purchase price.

Simply let us know at least 2 weeks before the scheduled removal date if you’d like an extension.

Make sure to use trusted platforms that provide secure online transactions.

17. Buying tradelines from an unethical company

Unfortunately, in this industry, it can be hard to know who to trust. It is essential to do your research and choose a company you trust so you don’t waste your money on low-quality tradelines, tradelines that don’t post, or tradelines that are overpriced.

You also need to be sure to only use reliable platforms that provide secure online transactions. Warning signs that could indicate that a company lacks integrity include fake reviews, unavailable or poor customer service, and websites that are not secure or do not look professional.

18. Asking what the average boost of credit score is

We do not guarantee any boost of your credit score and we also cannot say what the average credit score boost from tradelines is. Tradelines affect everyone differently. One tradeline may help one person while that same tradeline may hurt another, and have no effect on someone else.

All tradelines will be relative to what you already have in your credit file. There is no meaningful average effect of tradelines in general.

Be sure to read “How to Choose a Tradeline” and use our Tradeline Calculator to understand how buying a tradeline could affect your specific situation.

19. Asking for a specific credit score

Although we do not guarantee any boost of your credit score, often when we hear a variation of the following question. The request goes something like this… “I currently have a 520 credit score but I want to be over 700. What tradeline do you recommend to accomplish this?”

Again, we are unable to answer these kinds of questions, but in talking about this topic in general, who says that it is even possible to go from a 520 to over 700 anyway? Not us. (Although we are not saying it is impossible either.) We just do not advise on these types of credit score requests.

But going back to talking in general, if someone has a 520 credit score they probably have some serious derogatory accounts in their credit. If they have such derogatory accounts in their credit file, their credit score will probably not be a 700 regardless of what other tradelines may exist in their credit file. So in this example, the question itself is flawed, since it may be impossible to begin with.

Even in less extreme examples, no one knows the exact credit score algorithms, so no one can say with certainty. Therefore, it is best to not ask that question, because whoever answers that question is making a wild guess and they could easily be wrong and give you bad advice.

Steer clear of CPNs, which could get you caught up in felony identity fraud.

20. Buying tradelines for a CPN

We do not sell tradelines to those trying to use CPNs.

The reason for this is that the Social Security Administration and the Federal Trade Commission have both stated that CPNs are not legitimate and that the use of CPNs to obtain credit is fraud and a federal crime. We highly recommend avoiding any person or business trying to sell you a CPN.

21. Thinking that buying a high-limit tradeline automatically means that you will also get approved for a high-limit credit card

Having a high-limit authorized user tradeline does not automatically guarantee that you will get approved for your own high-limit credit card. Most banks that offer credit cards will typically also consider your income, expenses, credit score, and possibly several other factors relating to your ability to repay debt in order to make a decision on whether or not they are willing to extend credit to you.

22. Mistaking tradelines for credit repair

Buying tradelines is not credit repair. Credit repair seeks to correct inaccurate items on your credit report. If you have inaccurate items on your credit report, you definitely want to get those items removed. [Disclosure: This article contains affiliate links.]

While credit repair is typically associated with removing items from your credit report, buying tradelines adds information to your credit report. Credit repair and tradelines work best together, as you can see in our Credit Repair vs. Tradelines infographic and our article on The Future of Credit Repair and Tradelines.

23. Having extremely bad credit to begin with

If you have bad credit, you may need to fix your credit in order to get the maximum benefit possible from tradelines.

Occasionally we get a call from someone who might tell us that they are currently 90-120 days late on 2-3 accounts and their credit score is in the dumps. Can we help someone with extremely bad credit? The answer is probably no.

Again, we are not able to advise on credit scores (only general information) but in our opinion, if they are currently that far behind on bills and have multiple major derogatories on their credit report, there is no way they can have good credit without correcting the situation.

After all, a credit score is meant to calculate the likelihood of someone defaulting on a credit account, and if they are proving that they are currently in default, then their credit score is going to reflect that. The best advice is to pay those accounts current if they are trying to improve their credit.

24. Buying tradelines from the wrong banks that don’t post well

The truth is that most banks across the country do not post authorized user data very reliably. In other words, with most banks, the odds of a non-posting are very high.

Our company has tried out almost all of the common banks, and due to our high volume of tradeline sales, we have amassed a large amount of data. We know which banks post well and which ones do not. In fact, just about every other tradeline company out there sells tradelines from many more banks than we do.

The reason for this is not because we do not have that inventory available. It is because our integrity level when it comes to the reliability of our postings is so important to us.

The truth is that any company who sells tradelines from more banks than we do automatically has a higher non-posting probability and a lower integrity level. Saying it bluntly, we have the highest posting success rate in this industry because we only work with the best of the best banks that post the most reliably. All other tradeline companies have a lower posting success rate because they work with banks that are less reliable.

In addition, we provide guidelines to follow to get your tradelines to post as often as possible.

If you have a bankruptcy or collection with a bank, tradelines from that bank may not post for you.

25. Having filed bankruptcy with the bank you are ordering a tradeline with

It is possible that some banks will not work with a person if they have filed bankruptcy with that bank. They may be in a sort of “blacklisted” status with that bank.

This can also apply to authorized user positions. Therefore, if you owed a debt to a particular bank when filing for bankruptcy, it is best to choose a tradeline from a different bank as a precaution.

26. Having outstanding collections against the bank you are ordering a tradeline with

Similar to the point made above regarding bankruptcies, having outstanding collections with a certain bank could also pose an issue. The collection status is probably less of a risk of non-posting than the bankruptcy status, but it is still worth mentioning as a potential problem.

27. Thinking that primary tradelines are the best option

![]()

Since there are many different credit scoring algorithms, everyone actually has many different credit scores.

Often the main goal of someone shopping for tradelines is to eventually open their own primary accounts. However, we regularly get calls from people asking if we sell primary accounts. The answer is no, we do not.

Being the primary borrower on an account means someone extended credit to that individual and they are financially responsible for that account. In other words, that person is actually issued credit.

We know of some options within the tradeline industry where companies really will issue credit and that accomplishes the “primary tradeline” desire that some consumers have, however, they are usually relatively low limits, and of course, they have no age since it is a brand new account.

So is a primary account with a low limit and no age better than an authorized user tradeline with a high limit and lots of age?

From what we have seen, if we had to choose between these two scenarios above, we believe the authorized user tradeline with age and a higher limit would be the more powerful choice.

28. Not realizing that you have many different credit scores

Each major credit bureau has its own algorithms and reporting methods, and even within each credit bureau, there are many different versions of credit scoring models. Often, the score that is used depends on what kind of company is ordering the report.

For example, not only might your credit score be different at each credit bureau, but the score might also be different depending on whether you are applying for a mortgage, a credit card, a car loan, or trying to rent an apartment.

The credit scoring algorithm used might be one of many different versions of the FICO score, or it could be a VantageScore.

It is possible that each person has over 30 different credit scores. If you google “how many credit scores do I have,” you can read more about this.

The authorized user must use the correct address that is on file with the credit bureaus to ensure the tradeline will post.

29. Not using the correct address that is on file with the credit bureaus

When adding an authorized user to a credit card, it is important that the authorized user provides the correct address that is on file with the credit bureaus. The authorized user’s address is a data point that helps identify the person, and if that does not match up, there can be issues with the tradeline posting.

Check your credit reports to confirm that the address in your file is correct and then make sure to provide this same address when purchasing your tradelines.

30. Having no credit score at all

There are instances where some people do not have any credit score at all. There may be several reasons why this is the case.

For one, maybe the person just never had any credit at all. If this is the case, then getting a tradeline to post should not be a problem.

Another possibility is that the person had derogatory items on their credit report and participated in some sort of aggressive credit sweep or credit repair deletion service that essentially deleted everything from their credit report.

In these types of scenarios, getting a tradeline to post can be a problem. Sometimes there may be blocks on that person’s credit file that prevent the new authorized user account from posting.

31. Not having enough tradelines or having only authorized user tradelines in your credit file

As we mentioned, having a good mix of various credit types is important to building good credit. Therefore, you do not want your entire credit profile to be made up of authorized user tradelines exclusively.

In general, the best credit profiles belong to people who have multiple tradelines from a variety of different types of credit, including credit cards, auto loans, mortgages, installment loans, etc.

If you are not sure how many authorized user tradelines you might need, our article can help: “Buying Tradelines: How Many Tradelines Do I Need?”

32. Not having a tradeline alert set up

A tradeline alert is a notification that a new or updated tradeline has posted to your credit file. To set one up, you will need to sign up for a credit monitoring service.

We ask our customers to make an account with Credit Karma, a free online service that automatically notifies you when new accounts have been added to your TransUnion or Equifax credit report. Credit Karma is also how you will verify whether or not your tradeline has posted.

33. Entering your personal information incorrectly when placing an order

As we alluded to above, there are certain pieces of information that need to match up in order for a tradeline to post to your credit report, such as your name and address. In order for the banks and credit bureaus to verify your identity and link the tradeline to the correct credit profile, the personal information you provide when buying tradelines needs to be 100% accurate, or else there is a chance that your tradelines will not post.

Unfortunately, people often make mistakes when typing in their names and addresses, which can result in their tradelines not posting. Be sure to double-check all of your information for accuracy and correct any typos before placing your order to ensure that your tradelines post to your credit report.

For more tips on how to avoid a non-posting, see our article on how to get tradelines to post.

34. Being unaware of our non-posting policy

Although we are proud to have the best posting rate in the industry, we can’t prevent the occasional non-posting because unfortunately, the banks and the credit bureaus are not always 100% accurate in their reporting processes.

If your Credit Karma credit report has been updated after the last date within the reporting period and your tradelines still haven’t posted, you can follow these instructions to request a refund or exchange for the non-posting tradeline.

When buying tradelines, use some best practices to get your tradelines to post so there is a lower chance of having to deal with a non-posting.

Still feeling unsure about tradelines? Check out our Tradeline FAQs.

What mistakes have you seen when it comes to authorized user tradelines? Are there any common mistakes that you would add to this list?

Read more: tradelinesupply.com

If you have credit cards with low credit limits, you may be interested in increasing your credit limit. In this article, we’ll talk about why your credit limit is important, reasons to increase your credit limit, when and how to request a credit line increase, and more. Keep reading for everything you need to know about how to increase your credit limit.

If you have credit cards with low credit limits, you may be interested in increasing your credit limit. In this article, we’ll talk about why your credit limit is important, reasons to increase your credit limit, when and how to request a credit line increase, and more. Keep reading for everything you need to know about how to increase your credit limit.

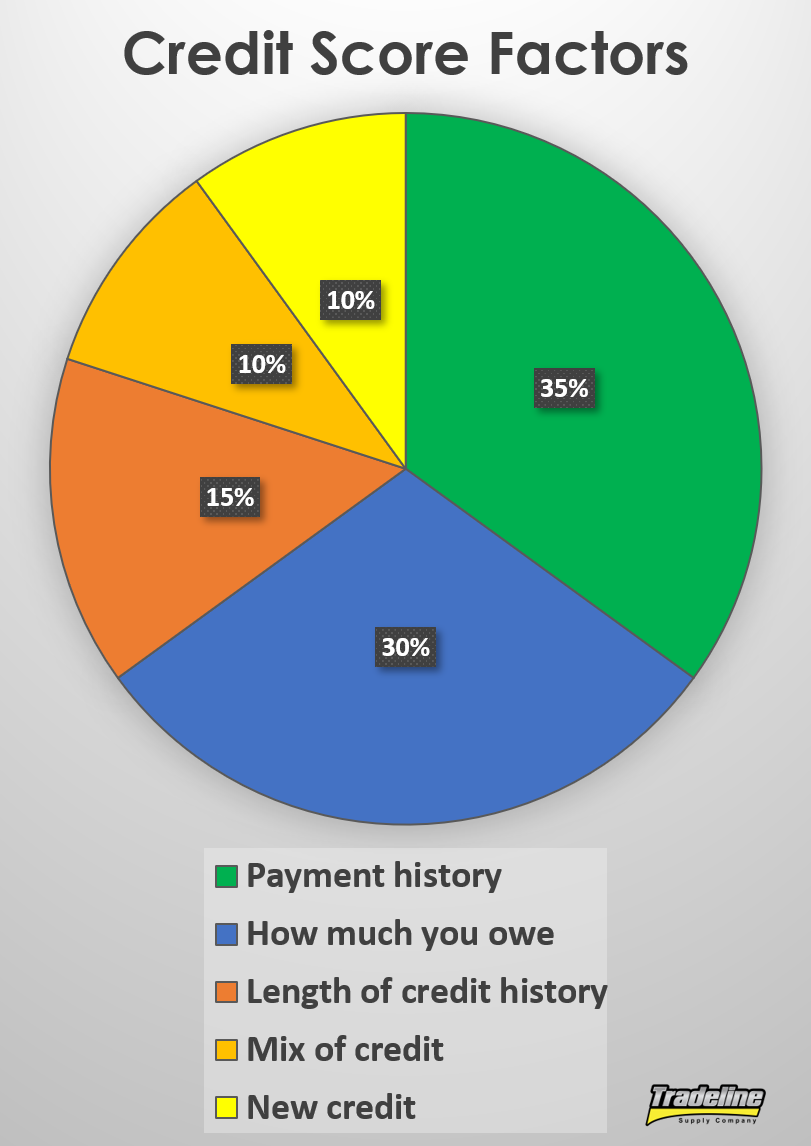

When it comes to credit scores, there’s a lot of confusion and misinformation out there. Our credit scores impact our lives in more ways than you might think, yet, unfortunately, they are complicated and difficult to understand. In this article, we’ll clear up what credit scores are, why they matter, how to build credit, and how to improve your credit score.

When it comes to credit scores, there’s a lot of confusion and misinformation out there. Our credit scores impact our lives in more ways than you might think, yet, unfortunately, they are complicated and difficult to understand. In this article, we’ll clear up what credit scores are, why they matter, how to build credit, and how to improve your credit score.