Did you know that sometimes credit reports can become “mixed” or “confused”? This situation is rare, but it is good to be aware of nonetheless. In a recent Credit Countdown video, credit expert John Ulzheimer explained what these terms mean. Plus, he also describes some other types of rare credit file issues.

Keep reading for more on mixed files and watch the video version at the end of this article.

What Is a Mixed Credit File?

A mixed credit file erroneously contains information from more than one consumer within the file. This is due to a mistake at the credit reporting agency where the matching logic software that is used to match a consumer’s information to their credit file ends up matching the wrong consumer’s information with someone else’s credit file.

If you have a mixed credit file, that means you have someone else’s data in your file that should not be there, whether the information is good or bad. Of course, it can be especially problematic if the incorrect information is derogatory.

The good news is that mixed credit files are extremely uncommon. On the rare occasions when mixed files do occur, it is often between two people who have the same names and addresses and possibly similar Social Security numbers, as may be the case with family members who share a name and live at the same address.

Mixed credit files are also sometimes referred to as “confused” files because the credit reporting system has confused one consumer with another.

What Is a Duplicate Credit File?

A duplicate file simply means that there are multiple credit reports in your name at the credit reporting agency. According to John, having duplicate credit files can be an issue if one of the files generates a credit score that is lower than the others.

Professionals in the credit industry may refer to instances of duplicate files as “dupes” for short.

While duplicate files may occasionally cause problems, the credit reporting agencies have ways to resolve the issue by merging the dupes.

Mixed files occur when the credit reporting system’s matching logic incorrectly attaches one consumer’s information to a different consumer’s credit file.

What Is a Fragmented Credit File?

Another type of inaccurate credit file is known as a fragmented file or a “frag.”

Fragmented files lack some of the information that is supposed to be on your credit report, so only a fragment of your credit file is present.

Missing information on your credit file can, of course, prevent your credit score from being as high as it should be, since you might be lacking important credit history, or it may be otherwise not fully representative of your full credit profile.

Conclusions

Mixed files, duplicate files, and fragmented files are all cases in which your credit report may be inaccurate. It should be stressed that these situations occur very rarely, so they will most likely not apply to you. However, if you find yourself dealing with one of these file types, contact the credit reporting agency so that they can resolve the issue for you.

Head to our Knowledge Center for more articles like this, or visit our YouTube channel to see more videos on tradelines and credit!

When purchasing tradelines, there are some cases where it is best to get a single tradeline and other cases when multiple tradelines might be more appropriate. To help you decide, we’ve provided some examples for each scenario below.

When to Buy Two or More Tradelines

Thin Credit File (Too Few Accounts)

Balance out derogatory accounts with positive tradelines.

Credit scoring models value a mix of several different types of credit accounts, so a thin file with only a few accounts might be limited in what it can achieve. In this case, adding a few tradelines would be ideal because it would help increase the number of accounts in the file.

On the other hand, someone with no credit at all or an extremely thin file can also experience significant benefits from adding one tradeline, since they didn’t have much there to begin with. Of course, more than one tradeline will help even more.

Balancing Out Derogatory Accounts

Accounts that have negative marks such as late payments and collections can really drag down credit. Derogatory accounts need to be outweighed by positive accounts, so one’s credit report should contain at least 2-3 positive tradelines for every negative account. Therefore, multiple tradelines may be necessary to balance out derogatory accounts damaging one’s credit.

Maximizing Results

For those looking to get maximum results, buying several of our best tradelines would be the ideal plan. This becomes increasingly important for people who already have good credit (680 FICO or higher) because it is much more difficult to significantly impact one’s credit report with a file that is already relatively strong.

There is also a point of diminishing returns on tradelines for those with already high credit scores, so situations like this require purchasing the absolute best quality tradelines in order to achieve positive results.

In other instances, the goal may be extremely important and the risks of failing to meet that goal may be significant. In situations where the outcome is very important, we recommend using the maximum strength possible.

Of course, the risk is that there are no guarantees on what the results will be, but at least you can be sure that you received the maximum benefit possible from tradelines. The rest is up to you.

Posting to a Specific Credit Bureau

In time-critical situations, purchasing additional tradelines will help protect against potential non-postings.

If it is important for a tradeline to post to a specific credit bureau, this is a good time to consider purchasing more than one tradeline.

Unfortunately, banks and credit card companies are not always 100% accurate in their reporting process, so while we guarantee that each tradeline will post to at least any two out of the three major credit bureaus, we do not have any control over which of the three bureaus the tradelines will post to.

Because there is always a degree of uncertainty with tradelines, if you are looking to get a tradeline to post to a specific bureau, purchasing extra tradelines will help provide the added security you need.

Important Time-Sensitive Events

Similarly, if something important and time-sensitive is going on that depends on the tradelines posting, the safest bet is to get more than one tradeline. Again, we do offer a money-back guarantee in the event that a non-posting occurs, but the fact is that non-postings do occasionally happen due to inconsistent reporting by the banks.

In time-critical situations, there may not be time to exchange a non-posting tradeline for a new one and wait for the new one to post. If you are counting on tradelines to post within a certain time frame, investing in additional tradelines will help hedge against potential non-postings.

When to Buy One High-Quality Tradeline

It’s usually best to purchase one high-quality tradeline if there are budget constraints.

Budget Constraints

If your budget is constrained to a certain dollar amount, it is usually better to purchase one high-quality tradeline rather than dividing that amount between two tradelines that are not as high in quality.

This is because credit scores consider both your average age of accounts and the age of your oldest account. A single account with lots of age has more potential to increase those numbers, while two accounts with less age may not offer as much improvement or might even dilute the credit file.

Here is a hypothetical example to consider. Let’s say your current average age of accounts is 2 years. If you were to spend the same amount of money in either case, would it be better to buy two tradelines that are both 4 years old, or one tradeline that is 8 years old?

If you decided to buy the two 4-year-old tradelines, this would increase your average age of accounts to about 3 years ([2 + 4 + 4] / 3 = 3.3) and your oldest account would be 4 years old.

On the other hand, if you were to buy one 8-year-old tradeline, this would bump up your average age of accounts to 5 years ([2 + 8] / 2 = 5) and your oldest account would be 8 years old.

In the second scenario, you end up with a higher age for both of these important credit history factors. Be sure to check out our tradeline buyer’s guide and tradeline calculator to help determine the best plan of action for your situation.

Current credit file

After adding 2 4-year-old tradelines

After adding 1 8-year-old tradeline

Average age of accounts

2 years

3 years

5 years

Age of oldest account

2 years

4 years

8 years

It is more difficult to affect the average age of accounts when there are many accounts, so one high-quality tradeline tends to be the best choice for very thick files.

Extending the Age of Your Oldest Tradeline

The age of the oldest account in your credit file is a very important data point. If the goal is simply to extend the age of the oldest tradeline in the credit report, then of course only one tradeline is needed. The tradeline just needs to be older than the oldest account that is currently on file, but obviously, the more age the better, so we recommend going significantly older.

Very Thick File (15 or More Accounts)

A very thick file with a large number of accounts will “dilute” the power of any tradelines that are added. Since there are so many tradelines already in the file, it will be more difficult to affect the average age of accounts. Therefore, one premium tradeline with a lot of age and a high credit limit will be a better fit for a very thick file, rather than multiple less potent tradelines.

Focusing on Credit Limit

Some consumers are less concerned with the age of the tradelines and more concerned with the credit limit for their specific circumstances. If a high credit limit is the main priority, it will usually make more sense to purchase one tradeline with a high credit limit rather than multiple tradelines that have lower credit limits.

If a high credit limit is the goal, usually one tradeline is enough.

The strategy on this topic may vary depending on what you are trying to accomplish and what your goals are, but in general, if you can accomplish the goal with one tradeline, that would probably be the better option.

Modest Goals

Depending on what a person’s goals are, they may not need to get the maximum results possible. For smaller goals, one tradeline may be all they need. However, it is always best to try to overshoot the goal in order to have some extra insurance in making sure the goal is truly achieved.

No Credit File or an Extremely Thin File

As we mentioned previously, adding a few tradelines to a thin credit file is ideal because it greatly increases the number of accounts in the file.

Adding just one tradeline to a very thin credit file can make a big difference.

However, it’s also important to keep in mind that someone with no prior credit history or an extremely thin file may still find value in buying just one tradeline, since adding one account to a baseline of zero or one existing accounts is still a significant change.

As an example, adding one tradeline to a credit report that previously only had one account in it represents a 100% increase in the number of accounts in the file! This not only adds valuable age and payment history but also impacts the “credit mix” factor in credit scoring.

Key Takeaways on How Many Tradelines to Buy

To summarize when you should consider purchasing a single tradeline versus when you should consider investing in more than one tradeline, we have included the main points of this article in the table below.

When to Buy Two or More Tradelines

When to Buy One High-Quality Tradeline

If you have a thin credit file (too few accounts)

If you have budget constraints

If you need to balance out derogatory accounts

When you want to increase the age of your oldest tradeline

When you want to maximize results

If you already have a very thick file (15 or more accounts)

When you need a tradeline to post to a specific credit bureau

If you want a high credit limit

If you need a tradeline for an important, time-sensitive event

If you have modest goals

If you have no credit file or an extremely thin credit file

If you are wondering how many tradelines you need, remember that the power of tradelines is always going to be relative to your current credit file and it is important to consider what will be the best fit for your specific situation.

In some situations, it may be important to maximize results using multiple powerful tradelines, such as when you are trying to accomplish a major goal or when there are serious hurdles to overcome. In other cases, one good tradeline might be all you need.

Whatever the case may be for you, it is always best to understand how tradelines work first and foremost and avoid making any common mistakes.

In simplest terms, the safest option is always to overshoot your goal and stick with the highest quality tradelines within your budget, and remember that in most cases, age is key. If budget is a big concern, then it’s usually best to just buy one of the highest quality tradelines your budget allows.

What are your thoughts on this article about how many tradelines to buy? We would love to hear your feedback, so leave a comment below!

Using a credit card is easy — you use the card to buy things and then pay the credit card bill.

A credit card can sometimes be difficult, however, when dealing with your credit file. From a missed payment to a loan that isn’t yours that’s incorrectly listed on your credit report, there are all kinds of ways your credit score can drop. And not all of them are from something you did wrong.

Consumers have protections under the law regarding their credit reports — which is where credit scores and credit problems are listed for lenders to check before offering you credit. Errors on a credit report can drop your credit score, making it harder to get a loan, credit card, rent an apartment, or qualify for insurance coverage, among other things.

The main law that protects consumers from credit errors is the Fair Credit Reporting Act, or FCRA. Here are some of the rights you have under this law and how to use it to protect your credit:

View credit reports

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months. You can do one check every four months from each of the three — Equifax, Experian and TransUnion — if you really want to be on top of it.

Start by going to AnnualCreditReport.com to request your credit file online. Only use that website and don’t use a copycat site that charges fees for what should be a free service. You’ll need to verify your identity to get online access. You can also request your credit file through an automated phone system or the mail.

The FCRA applies to all consumer reporting agencies. You can also look at reports from other consumer reporting agencies that collect noncredit information about you. These include rent payments, insurance claims, employers and utility companies. The Consumer Financial Protection Bureau lists the reporting companies and how to request a free report from each.

Check your credit score

The law allows you to request a credit score, though it’s legal for credit agencies and other businesses to charge you a fee for this service. Some credit cards provide scores for free, so check with your credit card issuer first.

A credit score isn’t the same as a credit report. Information in a credit report determines a credit score, and each credit bureau can use a different scoring model that requires it to provide different information. You have different credit scores, depending on which factors are weighed more heavily.

Monitoring your credit is vital. Make sure that you review your credit report for any inaccuracies.

Know who can view your credit report

The FCRA doesn’t allow a credit reporting agency to share your credit file with someone who doesn’t have a valid need. Some inquiries, such as from a potential employer or landlord, require your written consent. And, they can only check your credit report, not your credit score.

The credit reporting agencies can share your credit report for legitimate reasons, such as when you’re applying for credit, insurance, housing or with a current creditor.

Disputing errors

Getting a credit report in your hands can lead to all sorts of eye-opening concerns. Anything that’s listed as negative should be checked for accuracy. Here are some things to look out for:

Eviction that wasn’t legal.

Creditor listed that you didn’t have an account with.

Loan default.

Wrong name.

Wrong address.

Wrong Social Security Number.

Incorrect loan balance.

Closed account reported as open.

A loan you didn’t initiate.

Some errors may be simple to resolve and others you may need to do more research on before disputing them to ensure they’re incorrect.

For example, you may not recognize the name of a creditor and assume you don’t have an account with them. But it may just be a store credit card you recently applied for that is listed by the issuing bank’s name. Or maybe a home or auto loan was sold to a new loan servicer.

Other errors could be reason to suspect identity theft, or there could just be wrong information that’s bringing down your credit score.

If you suspect identity theft, such as someone taking out a credit card in your name, then file a police report and report it to your credit card company and the credit reporting agencies.

To dispute erroneous information, use certified mail to send the credit bureau a letter and copies of documents explaining the error. If a loan still shows an outstanding balance and you have written proof that it was paid off, for example, send a copy to the credit agency.

Credit agencies have 30 days to investigate and respond to your dispute, unless they deem it frivolous.

If it corrects an error, it must send you a free copy of your credit report through AnnualCreditReport.com so you can see that the corrections have been made.

A time limit to negative information

The FCRA doesn’t allow credit bureaus to report negative information that’s more than seven years old, though it allows some forms of bankruptcy to remain on a credit report for 10 years.

There’s also a time limit for positive credit information such as on-time payments and low balances — up to 10 years after the last date of activity on the account.

Rejections based on credit report

If your application for credit, job, insurance or housing has been denied because of information in your credit report, the law gives you the right to know this information.

The landlord, employer or other entity that denied your application must notify you and give you the name, address and phone number of the credit reporting agency that provided the information.

The FCRA allows you to get a free copy of your credit report from that reporting agency within 60 days of the action against you. That’s in addition to the three free credit reports allowed annually.

To best deal with a potential rejection ahead of time, it’s smart to check your credit report before applying for credit, rental unit or related use of your credit report and check it for errors. Give yourself enough time to fix them.

Go to court

If these actions or a complaint with the CFPB doesn’t resolve your dispute, you may be able to sue for damages in state or federal court. You can sue a credit reporting agency or related parties for violating any of the above rights.

However, it’s worth knowing that your right to legal action doesn’t start until after the creditor or credit reporting agency has been notified of an error and has a chance to fix it. In other words, you’ll only be awarded damages if the adverse action happened after you reported the error.

So if you didn’t get approved for a mortgage because of a mistake on your credit report, it’s unlikely you’ll be compensated for losing out on the house if you lost out on it before reporting the mistake.

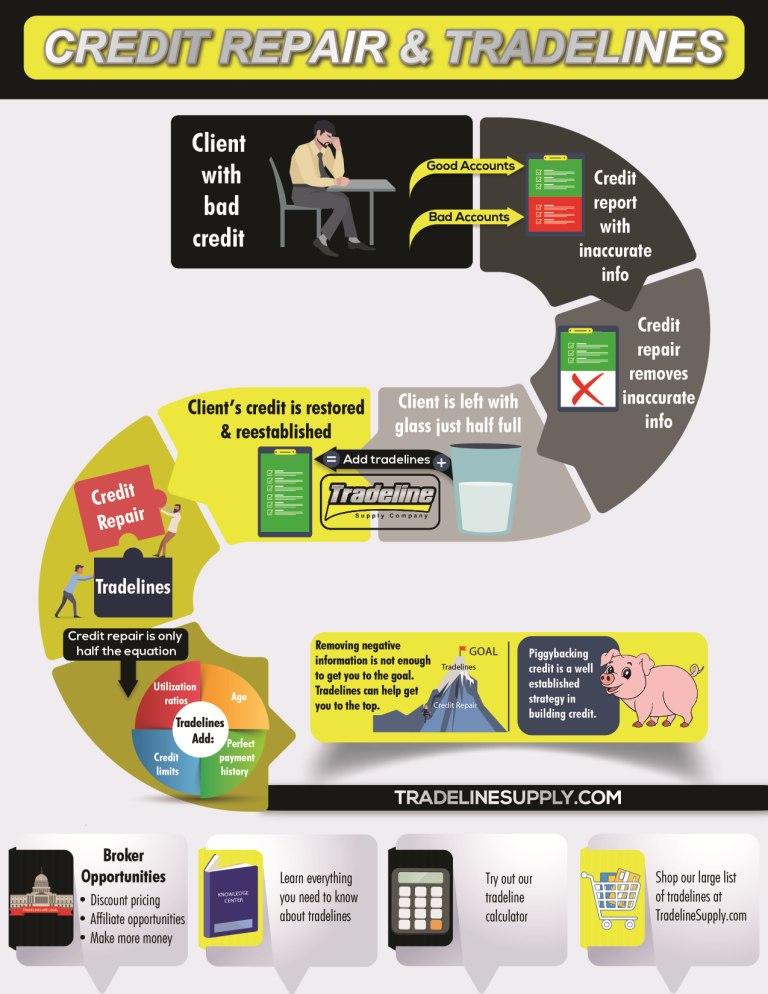

Perhaps the title “Credit Repair vs Tradelines” is not entirely accurate, but this is a common way that many consumers think of the two industries and even many credit repair companies as well. In truth, as our infographic illustrates, the two services really go hand-in-hand.

However, there are several differences that we will highlight in order to understand the full range of credit-related options. Be sure to check out our article below the infographic for all the details.

What Is Credit Repair?

The term “credit repair” can have different definitions depending on who you ask. Generally, however, credit repair is considered to be the process of mending poor credit that is a result of errors in your credit report or identity theft. This is accomplished by disputing inaccurate information in your credit file with the credit bureaus, who will investigate the claim and take appropriate action.

For example, if you have collections on your credit report that are being reported with inaccurate information, you can dispute the collection account and have it updated or removed from your credit report.

Sometimes people also use the term credit repair to mean fixing bad credit in general, using traditional methods such as bringing all accounts current and paying down debts.

For those who are seeking credit repair services through a company, you are probably interested in the process of repairing bad credit by disputing inaccurate negative information in your credit file. If your credit score is lower than the average range, going to a credit repair business may seem like an appealing option.

However, keep in mind that credit repair has its limitations. Since credit repair services focus on removing information from your credit file, once that is accomplished, there may not be much left in your file to show that you have a credit history at all. This is especially true of questionable credit repair companies who use dishonest methods to aggressively “sweep” your credit file of legitimate information.

In order to truly improve your credit score, it is important not only to remove inaccurate negative information but to also work on rebuilding your credit.

Credit repair focuses on removing inaccurate information from your credit report.

Tradelines vs. Credit Repair: What’s the Difference?

Addition and Subtraction

As we discussed above, credit repair can be thought of as the process of removing negative information from your credit report. In contrast, tradelines add information to your credit report.

A tradeline is simply any account in your credit file, so adding tradelines by definition bulks up your file. This can be helpful for people with short or thin credit histories, or those who are recovering from a period of bad credit and trying to rebuild their credit.

A short credit history means the age of your credit file is not very long, while a thin credit history means you have only a few accounts in your credit profile, if any. Credit scoring models factor in both the length of your credit history and your mix of credit, so having a thin or short credit file will likely result in a lower credit score rating.

Being added as an authorized user to tradelines that are in good standing and have a higher age (known as “seasoned” tradelines) could improve both of these factors by increasing your length of credit history and diversifying your mix of accounts.

In addition, seasoned tradelines for sale from a reputable company will have perfect payment histories and relatively low utilization ratios, which impact important components of your credit.

Tradelines can post to your report quickly, while the credit repair process may take longer.

How Long Does Credit Repair Take to See Results?

The credit repair process typically takes 1-6 months or longer, depending on how many disputes you need to make. Once you submit your disputes to the credit bureaus, they have 30 days to research the dispute and 5 more days to respond once they have completed the investigation. Sometimes, additional information may be needed, which can add more time to the process.

If you have a lot of errors to dispute, you may have to submit them a few at a time, which is why getting results can take several months.

Tradelines, however, can post to your credit report in as few as 11 days, and sometimes even faster. It just depends on the reporting period of the tradeline you are adding.

How Much Does Credit Repair Cost?

The cost of credit repair services can vary widely depending on the company, which services you need, and how long the process takes. Many credit repair organizations charge a monthly fee for their work in addition to an initial fee for pulling your credit reports. Typically, the monthly fees range between $60 to about $100 per month for basic credit repair services. [Disclosure: This article contains affiliate links.]

Purchasing tradelines, on the other hand, usually involves paying a one-time fee (unless you choose to extend the tradeline for additional time).

Is Credit Repair Worth It?

If you have bad credit, paying for a credit repair service is an option that you may want to consider, especially if you have a lot of errors on your credit report or if you have been the victim of identity theft and you need some help disputing fraudulent accounts.

If you do decide to hire a credit repair service to help you clean up your credit, make sure you research each company thoroughly and choose a legit credit repair company. Unfortunately, the industry has not earned the best reputation. Be sure to know your rights laid out by the Credit Repair Organizations Act (CROA) so you can protect yourself from being taken advantage of by shady credit repair companies.

Not everyone needs the help of a credit repair company to begin with. If you have one or two simple errors on your credit report, you may feel that you will be able to go through the credit repair process on your own and have those errors successfully removed or updated.

To answer the question of whether paying for credit repair is worth it, you’ll have to take a look at your credit report and decide whether the damage is extensive enough to warrant hiring a professional credit repair service or whether you want to try DIY credit repair.

How Credit Repair and Tradelines Work Together to Fix Your Credit

Credit repair and tradelines naturally go hand-in-hand. In one sense, tradelines pick up right where credit repair ends. Again, credit repair helps to “clean up” credit and tradelines help build or re-establish positive credit history.

One really should not exist without the other; the two techniques are most effective if done in tandem. Since credit repair removes information from your credit file, it may be necessary to add positive information to your file in the form of tradelines in order to truly rebuild your credit.

Tradelines can help to build or rebuild credit.

Buy Tradelines or Fix My Credit: Which Should I Do First?

It does not necessarily matter which one comes first. Both can exist at the same time.

However, if you have bad credit due to inaccurate derogatory information on your credit report, those variables will have an impact on your overall credit picture and could lead to tradelines having a diminished effect. In this case, the most effective course of action would be to repair your credit before adding tradelines.

On the other hand, it is never a bad time to have good things on your credit report. The timing of which strategy should come first ultimately depends on your individual situation and your own timeline.

For example, some credit repair programs take quite some time to accomplish. As we mentioned, is not uncommon for certain credit repair programs to take many months to complete. In these cases, tradelines may fit in at any given time during the credit repair process.

Credit repair and tradelines work best when used together as part of your overall credit strategy.

Why Don’t All Credit Repair Companies Offer Tradelines?

Surprisingly, not all credit repair companies sell tradelines or even know about tradelines. Sometimes tradeline companies are seen as competition to credit repair businesses because clients may end up spending money on tradelines as opposed to credit repair services.

However, as we have seen, credit repair works best when paired with tradelines. The best credit repair companies will provide you with all of the information and options that you need to make an informed decision about your financial future.

Conclusion

While tradelines and credit repair can both be effective in improving your credit, they are not the same thing. Rather, they are complementary strategies that work best when used together.

Don’t mistake tradelines for credit repair—think of tradelines as a way to build or re-establish credit. The best course of action for your credit is to evaluate your own unique situation and ask how tradelines can complement your credit repair strategy.

We all know that credit history is important because it’s how lenders, landlords, and sometimes even employers assess our creditworthiness. Anytime you apply for a loan or credit card, the lender will use your credit file to determine whether they think you are eligible for credit and what your interest rate will be.

But did you know that all credit is built from tradelines? Although this fact is not often discussed, it’s just as important to understand when it comes to building credit. Keep reading to find out why all credit begins with tradelines.

Although building good credit may seem complicated, it all boils down to properly managing your tradelines.

What Is a Tradeline?

A tradeline is any account that appears on your credit report. This includes both revolving accounts and installment loans.

Revolving accounts are accounts that can be used repeatedly without paying them off in full every month, so they may fluctuate in balance and minimum payment. Examples of revolving accounts include credit cards and home equity lines of credit. An installment loan is a loan that is repaid over time with a set number of scheduled payments, e.g. a mortgage, auto loan, or student loan.

All of these different types of accounts are tradelines. Essentially, whether you have good or bad credit depends entirely on how you manage your tradelines.

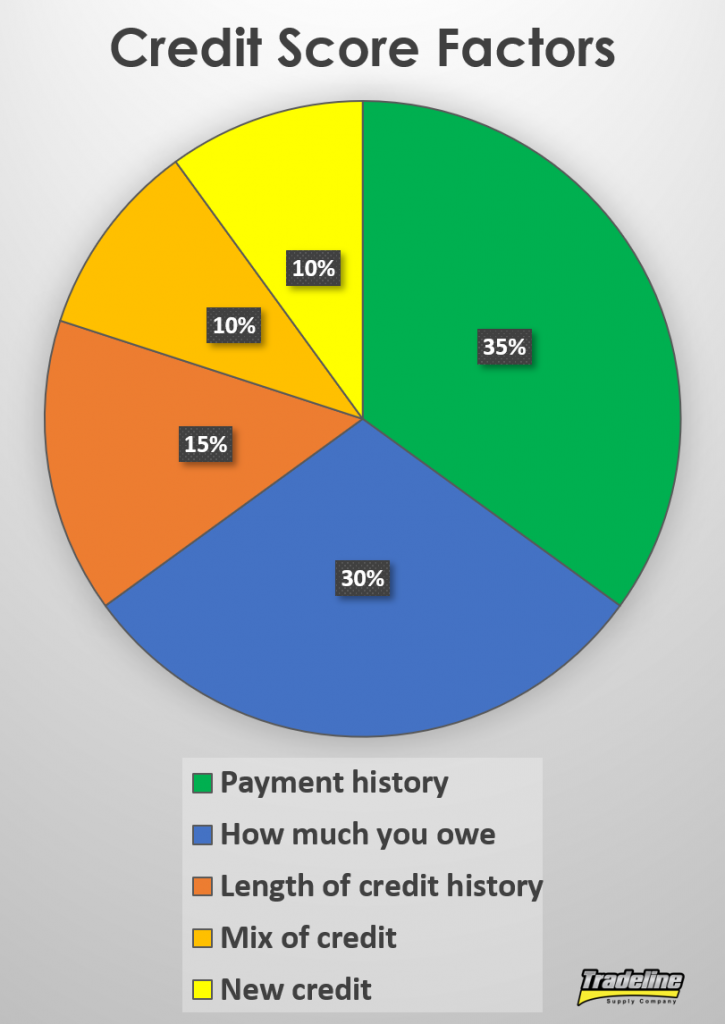

Although each credit reporting bureau keeps the specifics of their credit scoring models a closely guarded secret, the general categories that factor into credit scores are widely known. In general, here’s what goes into a credit report, which is then used to calculate your credit score:

Credit scores are comprised of five main factors. (Click this image to pin to your Pinterest board!)

Payment history, approximately 35%: Paying the amount due on your tradelines on time every month is extremely important. Late or missed payments could result in derogatory marks that bring down your score. It’s a good idea to have several different tradelines that are in good standing since this category is weighted so heavily. If you do have a derogatory tradeline, it is important to maintain a perfect payment history on the rest of your tradelines to balance out the negative mark on your report. You always want your good history to outweigh the bad.

Utilization, or how much you owe, approximately 30%: Your utilization ratio is the ratio of how much you owe on all your revolving accounts (e.g. credit cards) to your total available credit, expressed as a percentage. Credit bureaus may consider both your overall utilization ratio and the utilization ratio of each individual tradeline. The lower your utilization, the better—it is generally recommended to keep your utilization below 30% but having it lower than this is even better. Therefore, tradelines with high utilization can hurt your score, while tradelines with low utilization can help your score.

Length of credit history, approximately 15%: This category considers factors like the average age of your tradelines, the oldest tradeline in your credit file, and the ratio of “seasoned” to non-seasoned tradelines. A seasoned tradeline is generally considered to be one that is at least two years old, at which point it is believed that the tradeline begins to have a more positive impact on your credit file. The older your tradelines are, the better impact they will have on your credit report. Since length of credit history goes hand-in-hand with payment history, together making up 50% of your credit score, generally, age is the most powerful factor of a tradeline.

Credit mix, approximately 10%: Creditors want to make sure that you can manage different types of credit, so they look for a balanced mix of different tradelines in your report. The most important thing is to have tradelines in both of the two major categories: revolving credit and installment loans.

New credit, approximately 10%: Credit scoring models take into account any new inquiries and new tradelines that you have added in the past 6 to 12 months. Generally, opening a new primary tradeline can have a temporary negative effect on your score, since it has no age and the person has not demonstrated their payment behavior on that account for very long.

Every major factor that goes into your credit file directly depends on your tradelines. Therefore, by adding authorized user tradelines, you can potentially affect each of these five factors.

Mismanaging your tradelines can lead to bad credit. Photo via CafeCredit.com.

There are a few things that could show up in your credit file that are not technically tradelines, such as collections, judgments, bankruptcies, and foreclosures. However, these bad credit items can all be thought of as the result of not properly managing your tradelines. Let’s examine each example.

A collection occurs when you have not been making payments on a tradeline and the creditor sells your debt to a collection agency.

A judgment against you happens when you default on a tradeline and a judge orders you to pay back the debt.

You might declare bankruptcy if you cannot pay off your tradelines and need to be released from the legal requirement to pay them.

Foreclosure is when a mortgage lender takes possession of the mortgaged property when the borrower fails to make payments on the mortgage tradeline.

How to Build Credit

The best way to build a good credit record is to open a variety of tradelines and keep them in good standing by making payments on time and keeping the utilization low. The fact is that you simply cannot build credit without tradelines.

Opening a credit card is a common way to establish a credit file and start building credit, but it is not the only option. Other paths to building credit include taking out student loans, auto loans, or secured loans. Unfortunately, building credit is often considered as a catch-22 because lenders are hesitant to provide credit to those with no credit history, so it can seem like it takes credit to get credit.

To overcome this obstacle, many people rely on the positive credit history of others to establish their own credit file.

Parents sometimes add their children as authorized users to their credit cards to help them establish credit early.

The Consumer Financial Protection Bureau estimates that about 25% of consumers first acquire credit history via an account on which someone else was also responsible. Some of these consumers open a joint account with a co-borrower, while others become authorized users on someone else’s primary tradeline.

As an example of this, parents are commonly advised to add their children as authorized users to their credit cards in order to help them establish a positive credit history early in life. In fact, it is estimated that about 20-30% of Americans have at least one authorized user tradeline in their credit file.

Unfortunately, many people do not have the same opportunity to benefit from a family member’s authorized user tradelines. Studies have shown that minorities and lower-income demographics are less likely to have authorized user tradelines, which means they are likely to face difficulty in establishing a credit history.

We are proud to help reduce financial inequality by providing equal opportunities to those who may not have a friend or family member who can provide the benefits of an authorized user tradeline.

Tradelines and Your Credit

It is crucial to be knowledgeable about credit since credit is such an integral part of your financial well-being. Since all credit is essentially built on tradelines, it is equally important to understand the way tradelines may affect your credit.

Sometimes gaining access to tradelines can be a challenge for people who are either new to credit or who have had problems in the past and are trying to re-establish their credit. Traditionally, some people have had the privilege of relying on family and friends to help share credit, but new innovations have created equal opportunities for those who may not have the same opportunity. We are proud to provide quality tradelines for sale at affordable prices at TradelineSupply.com.

Were you surprised to learn that all credit is built from tradelines? Let us know by leaving a comment!

Did you know that sometimes credit reports can become “mixed” or “confused”? This situation is rare, but it is good to be aware of nonetheless. In a recent Credit Countdown video, credit expert John Ulzheimer explained what these terms mean. Plus, he also describes some other types of rare credit file issues.

Did you know that sometimes credit reports can become “mixed” or “confused”? This situation is rare, but it is good to be aware of nonetheless. In a recent Credit Countdown video, credit expert John Ulzheimer explained what these terms mean. Plus, he also describes some other types of rare credit file issues.

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months. You can do one check every four months from each of the three — Equifax, Experian and TransUnion — if you really want to be on top of it.

The FCRA entitles you to review your credit file from each of the three main credit bureaus for free once every 12 months. You can do one check every four months from each of the three — Equifax, Experian and TransUnion — if you really want to be on top of it.