Nearly half of Americans believe a credit score and a credit report are the same thing, according to a study by the American Bankers Association. That’s a big problem because it means many of us are seriously misinformed about how the credit system works.

Since credit is such an integral part of our financial ecosystem, it affects nearly all of us at some point in our lives. Your credit health can determine not only your access to credit and the cost of using credit but also employment opportunities, housing options, and more. Not understanding how credit works, therefore, can have serious consequences.

We want to help address this problem by making it easy to understand what your credit report is and why it’s important, the difference between your credit report and credit score, how to get a free credit report, and how to dispute errors on your credit report.

What Is a Credit Report and Why Is It Important?

A credit report is a detailed report on your credit history prepared by a credit reporting agency, also known as a credit bureau. The three main credit bureaus are Experian, Equifax, and TransUnion, and we’ll discuss each below. What is in your credit report can be different for each bureau, since they are private companies that do not share information.

What Is in a Credit Report?

Credit reports contain identifying information such as your name, social security number, and current and previous addresses. They also contain a detailed summary of your credit history, which includes items such as the following:

Credit reports include a list of your credit accounts and financial records.

A list of current and past tradelines (credit accounts), along with the date opened, credit limit, balance, and payment history of each account Inquiries into your credit history

Public records of bankruptcies, foreclosures, tax liens, etc. Accounts in collections

How Far Back Do Credit Reports Go?

The information in your credit report usually goes back about 7-10 years.

Current accounts should show up on your credit report as long as they are open.

Negative information, such as collections, will fall off your credit report seven years after the delinquency occurred. Closed accounts that were closed in good standing fall of your credit report in 10-11 years.

What Is the Difference Between a Credit Report and a Credit Score?

A list of all your credit accounts and related personal information

A three-digit number between 300 and 850 meant to represent your creditworthiness

Information in your credit report is used to calculate your credit score

Reflects the information in your credit report

You are legally entitled to get a free credit report from each bureau once a year

You are not legally entitled to check your credit score for free (although some credit card companies may offer this to customers)

Does not include your credit score

Does not include information on your credit history

Does Checking My Credit Report Hurt My Score?

While this is a common misconception, you can rest assured that checking your credit report won’t lower your credit score. Checking your own credit is what’s known as a “soft inquiry” or “soft pull,” which doesn’t hurt your credit. “Hard” inquiries can ding your score, but these are used by creditors when making lending decisions, not for checking your own credit report.

How to Get a Free Credit Report

By law, everyone is entitled to receive one free credit report from each of the three major credit bureaus once every 12 months. You can order all three at the same time or order each individual report one at a time.

Some people like to spread them out and get a free credit report from a different bureau every four months so that they can regularly check their credit reports for errors and inconsistencies. Each credit bureau is a private, for-profit company, and they don’t share information, so you could have errors on one of your credit reports but not the others.

Free credit monitoring websites like CreditKarma provide free credit reports and scores.

The best way to check your credit report for free is to order your free credit report from annualcreditreport.com. In fact, this is the only website authorized to provide the annual free credit report you are legally entitled to, according to the FTC—so beware of other sites claiming to offer free credit reports or free trials, especially if they ask for your credit card information.

However, there are now several free credit report websites that earn money through advertising and are thereby able to offer free credit monitoring services. Sites that offer completely free credit reports include:

You can also check your credit report for free if you have been denied credit because of the information in your credit report. You are entitled to get a free credit report from the bureau who provided the report that the lender used to make their decision.

You are entitled to a free credit report if you are unemployed and applying for jobs.

For example, if the lender who denied you credit looked at your Experian credit report, you can request your Experian free credit report. The adverse action letter informing you of the reason for your denial should have instructions on how to request your free credit report.

There are a few more cases in which you can qualify for an additional free credit report, including:

If you are unemployed and planning to look for work.

If you receive government assistance.

If you are a victim of identity theft.

Although experts recommend checking your credit reports at least once a year, the Consumer Financial Protection Bureau (CFPB) estimates that less than one in five consumers get copies of their credit reports each year. Don’t miss out on this opportunity to get your credit report for free so you can make sure your credit report is accurate and identify any problems before they get worse.

Can I Get a Free Credit Report Directly From the Credit Bureaus?

You can also get your credit report directly from each of the credit bureaus, but you may have to pay a fee if you go this route. If you want to get a credit report for free, your best bet is to order from annualcreditreport.com.

However, some people may want to check their credit reports more than once a year, so we’ll discuss additional options for obtaining your credit reports below.

Experian Credit Report

You can get a free Experian credit report that refreshes every 30 days through Experian’s website. They also offer paid options that come with additional information. The Experian free credit report does not include a free credit score.

Equifax Credit Report

You can get your TransUnion and Equifax free credit reports on third-party websites.

While you cannot get an Equifax free credit report from the bureau directly, you can pay a fee to access your Equifax credit report and score. To get your Equifax credit report, visit their website.

You can also view your free Equifax credit report and score through CreditKarma, which updates once a week.

TransUnion Credit Report

Accessing your TransUnion credit report requires signing up for a paid monthly subscription service with TransUnion. However, you can get a free TransUnion credit report from CreditKarma or NerdWallet.

How to Dispute Errors on Your Credit Report

Unfortunately, studies have shown that as many as one in five consumers may have errors on their credit reports, and about one in 20 have errors that are significant enough to potentially lower their credit scores. This means it is crucial to monitor your credit reports regularly and be aware of how to fix errors on your credit report.

The credit bureaus offer online forms to submit credit report disputes, but experts warn against using this option, as it does not allow you to write a detailed explanation of why you are disputing the information or provide sufficient supporting evidence. This leaves room for the credit reporting agency to deny your claim because you did not provide enough information.

The best way to dispute a credit report is to write a detailed credit report dispute letter and mail it to the bureau along with plenty of documentation verifying your identity and supporting your claim.

Once a dispute has been filed, the bureaus typically have 30 days to investigate the claim. If they verify that the item is accurate, it will remain on your report; if not, they must either update the item with the correct information or delete it entirely.

Errors on your credit report can, unfortunately, lead to bad credit. For this reason, checking your credit report regularly and disputing any errors is an essential step in maintaining your financial health.

It’s important to check your credit report for errors regularly.

If you have a lot of errors on your credit report or if you have been the victim of identity theft, it may also be worth considering hiring a reputable credit repair service to assist you in the dispute process.

Which Errors Can You Dispute?

The law requires that the information in your credit reports must be accurate, complete, timely, and verifiable. Anything that does not meet these requirements can be disputed.

Technically, you can dispute anything in your credit file, but that doesn’t mean you should try to dispute things that you know are accurate. The credit bureaus are allowed to ignore “frivolous” claims, and if they verify something to be true, it will stay on your credit report.

For more tips on how to dispute a credit report, check out this article from creditcards.com.

Quick Credit Report Facts

A credit report is a detailed report on your credit history prepared by one of the credit bureaus: Experian, Equifax, and TransUnion.

The information in your credit report is used to calculate your credit score.

Checking your credit report does not hurt your score.

You are entitled to a free credit report from each of the three bureaus once a year, which you can order from annualcreditreport.com.

You can dispute errors on your credit report by mailing a credit report dispute letter and supporting documentation to the credit bureau.

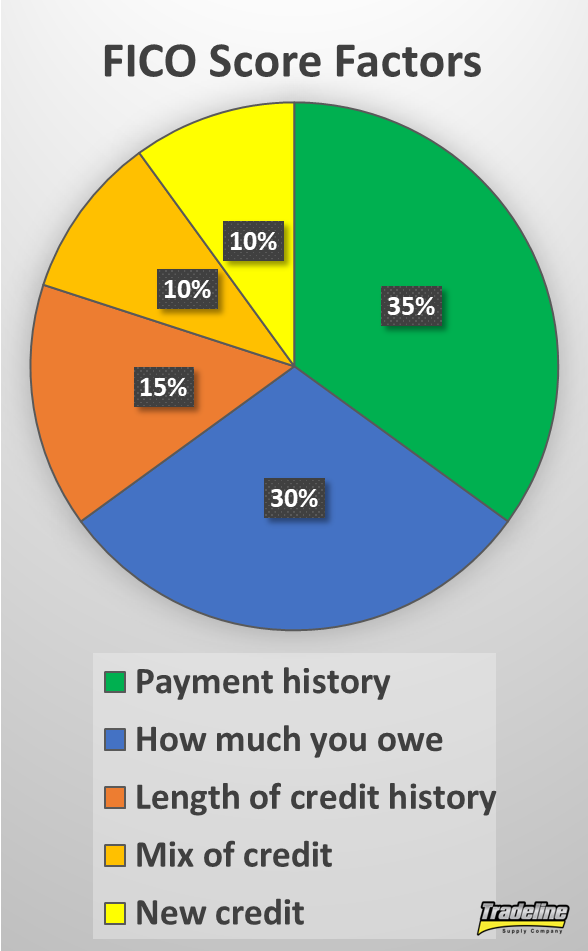

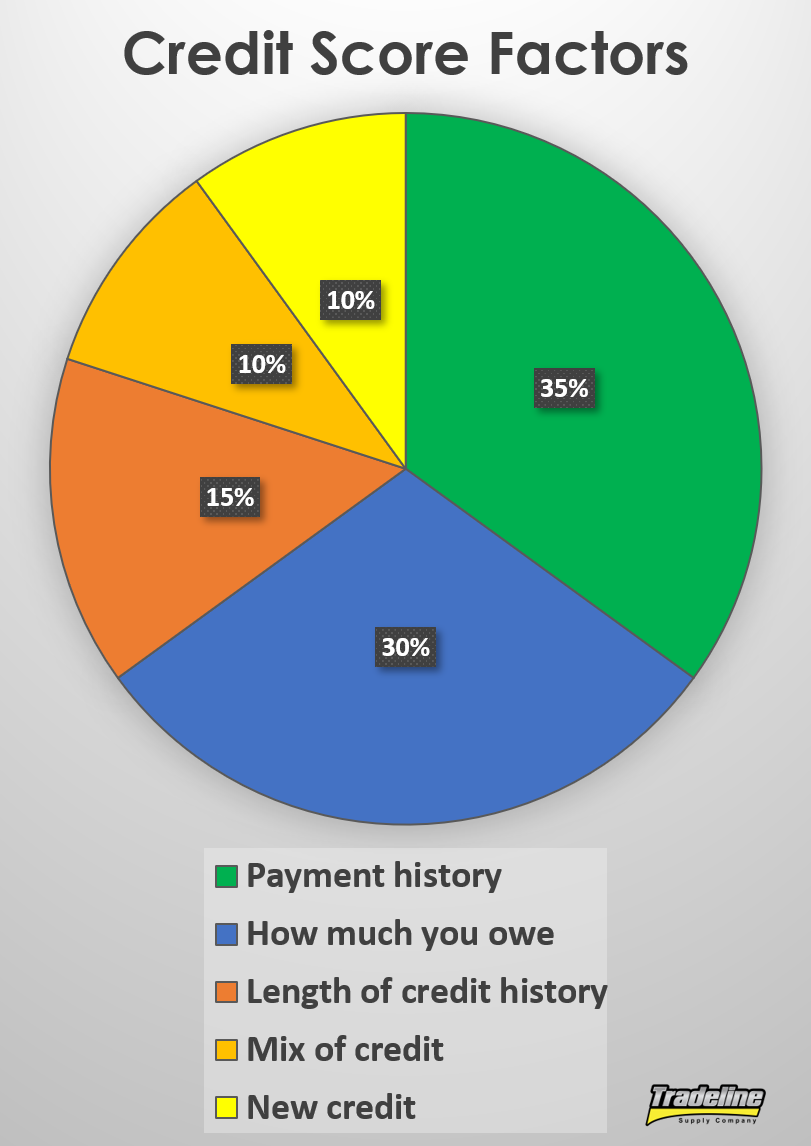

Length of credit history, also referred to generally as credit “age,” is one of the five main factors in the credit score algorithm, making up roughly 15% of one’s credit score.

FICO breaks up this general category into three parts:

How long each individual account has been open

How long certain types of accounts have been open (e.g. revolving accounts vs. installment accounts)

The amount of time since those accounts were last used

Since a longer credit history provides more evidence that you have responsibly handled credit, generally, those with longer credit histories tend to have higher credit scores than those with shorter credit histories. When it comes to age, more is always better.

Account Age & Payment History Are Linked Together

Age always goes hand-in-hand with payment history, which contributes about 35% of your credit score, making it the most heavily weighted category. Obviously, an account needs to have age in order to have a payment history, and as an account ages, it acquires more payment history.

Age also affects the power of blemishes in your payment history. For example, a missed payment can cause a big drop in your credit score at first, but as the account ages, the effect will gradually be diminished until the missed payment falls off of your credit report completely.

Since the length of credit history (i.e. age) and payment history categories are closely linked, we can add them together to find out their combined power, which turns out to be 50% of a credit score! Therefore, age-related factors are going to be extremely important when it comes to choosing tradelines.

Some Age Levels May Hold More Weight Than Others

Since age is such a big part of credit, there is a lot of speculation about the specific age-related factors that may play a role in credit scoring algorithms. For example, it is commonly believed that there are certain age levels after which an account has a more powerful positive impact on one’s credit.

In other words, the positive effect of age on an account is not thought to be a gradual and continuous increase in score over time, but rather, a series of jumps upward that happen at certain points in time, such as after a specific number of years or months have passed.

As we said, many speculate on this topic, and we don’t pretend to have the definitive answer. FICO, VantageScore, and other credit scoring companies intentionally keep the details of their credit scoring formulas under wraps. However, based on the examples that we have seen, we have come up with our own observations on the question of which age levels are particularly beneficial for credit.

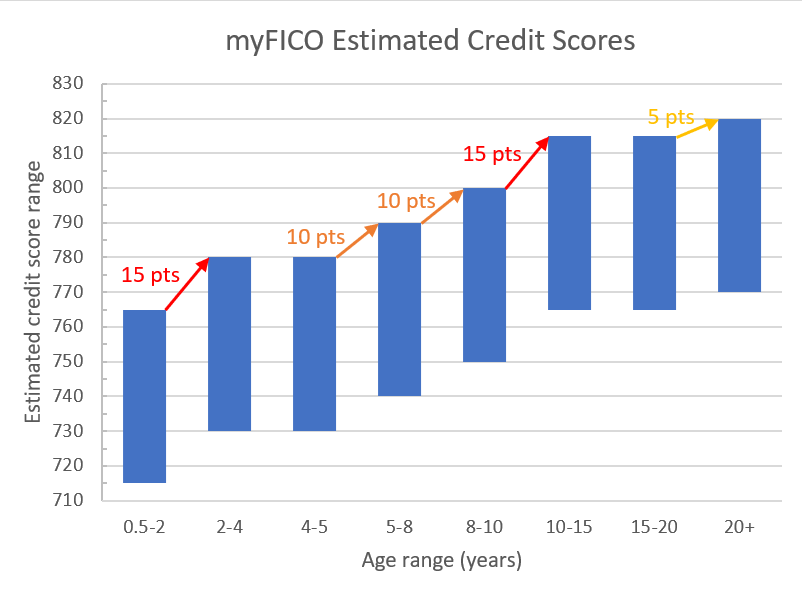

Age Bracket Experiment

To test out our theory, we conducted an experiment. We chose to use the myFICO Score Estimator specifically since this credit score estimator is owned by FICO themselves, who are the creators of the most widely used and trusted credit score. It stands to reason that using a product straight from the source of the FICO score would give the most accurate findings.

Educational scores such as the VantageScore use different algorithms and are not widely used by lenders. Therefore, since our priority is to understand our FICO score, the FICO score estimator will be the most useful.

We used this credit score estimator to estimate credit score ranges with a different age of oldest account each time, holding all other inputs constant. To minimize any negative impact from other factors that could affect the results, such as late payments or high balances, we chose the options that should represent the best impact on credit while still establishing a credit history.

How Do Credit Card Age Levels Affect Credit?

Here are the answers we gave to each question in the credit score estimator:

How many credit cards do you have? 1

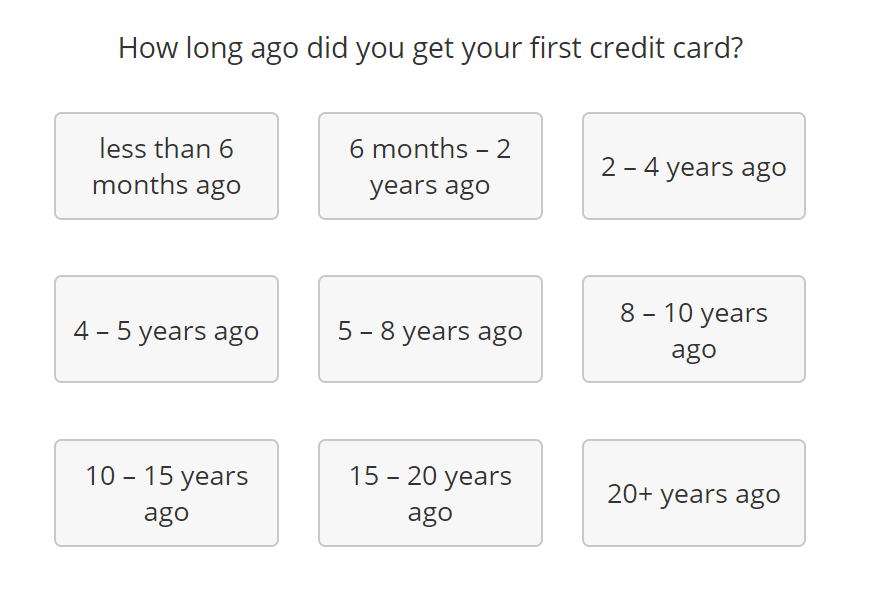

How long ago did you get your first credit card? (This is what we were testing, so it changed each time.)

How long ago did you get your first loan? (i.e., auto loan, mortgage or student loan, etc.) Never

How many loans or credit cards have you applied for in the last year? 0

When was the last time you opened a new loan or credit card? More than 6 months ago

How many of your loans and/or credit cards currently have a balance? 0-4

Besides any mortgages, what is the total balance on all your loans and credit cards combined? Less than $500

When did you last miss a loan or credit card payment? Never

How many of your loans and/or credit cards are currently past due? 0

What percent of your total credit card limits do your credit card balances represent? 0% to 9%

In the last 10 years, have you ever experienced bankruptcy, repossession or an account in collections? No

FICO’s Age Brackets

If you take the quiz, you’ll notice that the myFICO credit score estimator gives a hint as to potentially important age levels right in the first question.

The myFICO credit score simulator gives a hint as to potentially important age levels in the first question.

We tested each of the options shown in the screenshot while keeping all other answers the same, as we described. Keep in mind that the score estimator does not give a single number for the answer, but a range of 50 points (e.g. 730-780). You can see the results of our credit score experiment below.

The myFICO Score Estimator predicts that when all other factors are held constant, credit score increases occur after 2 years, 5 years, 8 years, 10 years, and 20 years. The biggest jumps happen at 2 years and 10 years, but the highest credit score can be achieved after 20 or more years.

The myFICO credit score simulator shows credit score boosts after 2 years, 5 years, 8 years, 10 years, and 20 years.

Based on this information, here’s how we would divide up the age levels of tradelines:

Level 1

0.5 – 2 years

Level 2

2 – 5 years

Level 3

5 – 8 years

Level 4

8 – 10 years

Level 5

10 – 20 years

Level 6

20+ years

Why Age Is Top Priority When Buying Tradelines

We have already discussed why we believe age is usually the most important factor when making the decision to purchase tradelines in our buyer’s guide to choosing a tradeline. Since age and payment history are always interconnected, together making up half of the power of a credit score, it is usually most effective to focus on getting a tradeline with as much age as possible.

The information we learned from the myFICO score simulator just goes to show how true that is. There can be a significant difference in the power and value of a tradeline that is 11 years old versus 9 years old or one that is 2 years old versus 1 year old.

Also, keep in mind the importance of your average age of accounts. According to FICO, those with the highest credit scores have an average age of accounts of about 12 years, compared to just 6 years for those with fair credit. Recall from our buyer’s guide that you might be surprised by how old a tradeline would need to be in order to get your average age of accounts up to the next level!

FICO also says that those with credit scores of 795 and above have 27 years of credit history on their oldest tradeline, while those with credit scores of 635 only have 12 years of history on their oldest account.

Credit score

Average Age of Accounts

Age of Oldest Account

Conclusion on the Importance of the Age of a Tradeline

When attempting to understand any system, it is always best to go straight to the source to acquire the most accurate information. Fortunately, FICO provides tools such as their myFICO Score Estimator for everyone to use to experiment with their own credit-related variables.

The payment history of an account is always attached to time; in other words, the age of a tradeline will automatically include the payment history as well. With the length of credit history representing approximately 15% of your credit score, combined with payment history representing approximately 35%, together these add up to approximately 50% of your credit score. This is why the age of a tradeline is almost always the most important variable to consider.

As we can see from the results from this case study, it is also clear that there are key age brackets that hold more weight than others. Knowing this information allows you to set strategic goals and allows you to plan your credit growth more effectively.

Therefore, when choosing tradelines you should keep age as a top priority and aim for the age thresholds that hold the most weight. Make sure to use our tradeline calculator to help you with these calculations so you get the most out of your tradelines.

Myths and misinformation about credit scores, credit reports, and credit repair are extremely common. Unfortunately, many people believe these myths, and their credit suffers as a result of taking incorrect actions.

Let’s get to the bottom of these credit myths and learn the truth about them so you can start improving your credit the right way.

Myth: Everyone automatically has a credit score.

Fact: 1 in 5 adults in the United States do not have credit scores.

A report by the Consumer Financial Protection Bureau (CFPB) found that one-fifth of adults in the United States do not have enough credit data to calculate a credit score by traditional methods. These consumers are called “credit invisibles.”

Low-income consumers are particularly susceptible to credit invisibility due to lack of access to traditional credit products. Some consumers may be credit invisible for other reasons, such as a voluntary decision not to use credit.

For those that do not use credit for whatever reason, it is likely that they do not have enough of a credit history to generate a credit score.

Consumers that are credit invisible may be able to generate a credit record by piggybacking on the good credit of others, but don’t assume that everyone has a credit score just by virtue of existing.

Myth: Checking your credit report will hurt your credit score.

Fact: Checking your own credit will not hurt your score.

Checking your own credit report results in what is known as a “soft pull,” which means the inquiry does not affect your credit score.

Myth: Your income affects your credit score.

Fact: Your credit score does not look at your income.

However, your income can affect your credit indirectly in that it influences the “five C’s” that have been shown to predict credit performance: capacity to pay off debts, the collateral backing a loan, capital available to repay a loan, conditions that affect income and expenses, and the character of the borrower.

Your capacity to pay off debts as well as the collateral and capital they have available to repay loans may all have a relationship with your income.

That’s a big part of the reason why low-income consumers are 8 times more likely than high-income consumers to have no credit score at all. In consumers that do have credit scores, those who reside in low-income areas have lower credit scores. In addition, low-income consumers are 240 percent more likely to have their credit file originated due to derogatory items such as collections.

So while your income is not technically incorporated into your credit score, it can definitely influence your ability to repay debts, which is the basis of a credit score.

Myth: You only have one credit score.

Each consumer can have dozens of different credit scores.

FICO 8 is the credit score most commonly by lenders today, but in some industries, older models or industry-specific models are used instead. For example, there are FICO scores tailored specifically toward auto loans and credit cards, and mortgage lenders are known to use the older FICO score versions 2, 4, and 5. Plus, FICO scores are different for each credit bureau.

VantageScore, which is increasingly used by some lenders as well as for consumer credit education, also has a few versions. The latest version is VantageScore 4.0, but VantageScore 3.0 is still the most commonly used version today.

Altogether, between the many versions of FICO scores and VantageScores, consumers can have dozens of different credit scores.

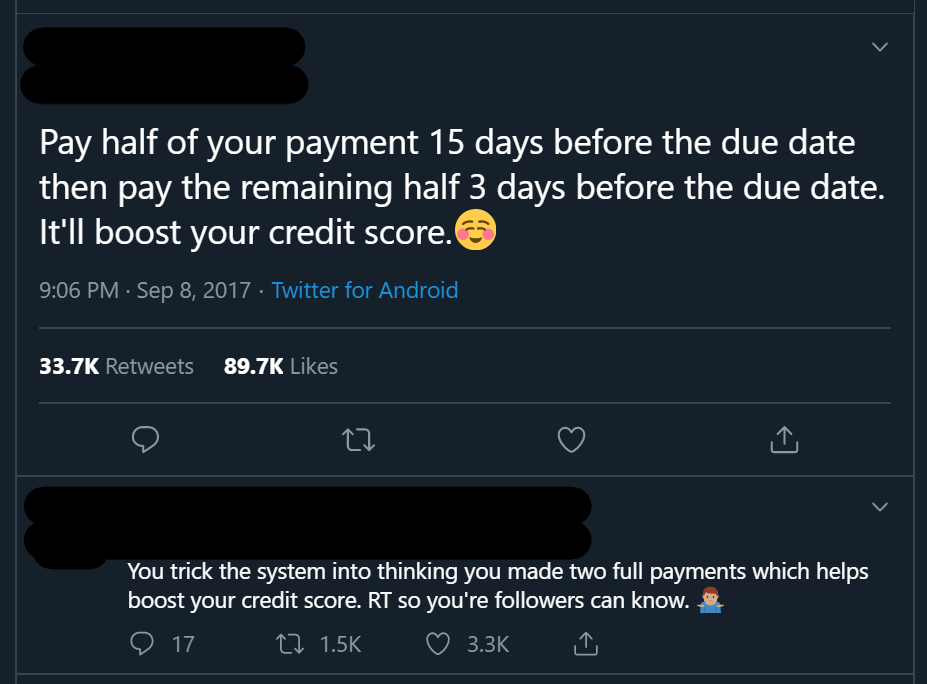

Myth: Paying half of your minimum payment twice a month counts as two full payments and tricks the system into giving you twice the credit score boost.

Fact: Dividing your bill in half and making two payments is the same as paying the full amount once.

This credit myth is unfounded yet often repeated.

If this “credit hack” sounds a little too good to be true, that’s because it is. It is simply not true that you can “trick the system” into thinking you have made two full payments by making two half payments.

Making a payment on a credit account affects two main factors of your credit score: payment history and credit utilization. Let’s discuss each factor individually.

When it comes to your payment history, making a partial payment that is less than the minimum amount due does not satisfy the requirement and will not count as an on-time payment. Only once you have made the second payment for the other half of the amount due will you have satisfied the requirement to be considered paid on time. Therefore, you do not gain any extra benefit to your payment history from dividing your payment into two parts instead of paying the full amount at one time.

As an example, let’s say you have a bill due on the 30th and the minimum amount you must pay is $50. We have laid out the two payment scenarios in the table below.

Scenario 1: Pay the full amount in one payment

Scenario 2: Make half of the payment twice

Date

Amount Paid

Payment Status

Date

Amount Paid

Payment Status

15th

15th

$25

Insufficient payment—$25 still due

30th

$50

Paid on time

30th

$25

Paid on time

As you can see from the table, in both scenarios, you only get the benefit of paying your bill on time once per billing cycle, not twice.

Now let’s discuss the utilization factor. Continuing with the same example, the total amount you are paying toward the account is $50 in both scenarios. Therefore, the overall improvement in your utilization ratio is going to be the same either way.

Now, if the reporting date for that account is in between the first and second payments, since you have already sent a partial payment, you may temporarily get a small boost from having a slightly lower utilization ratio when the account reports to the credit bureaus. But at the end of the billing cycle, the result will be the same.

If you don’t have any credit history, you can being building credit by piggybacking on someone else’s good credit.

If you decide to make extra payments in addition to your minimum payment, which is ideally what all responsible borrowers should be doing, that can certainly help your credit score by speeding up your debt repayment. But simply splitting the minimum payment into two payments won’t do anything to boost your score.

Myth: If you don’t have credit history, you’ll never be able to get credit.

Fact: You can start building credit by piggybacking.

While it can definitely be more difficult to get credit when you don’t have any credit history to begin with, it’s not impossible. There are credit products out there designed for people with no credit or bad credit, such as secured credit cards and credit-builder loans.

Another way to start building credit fast is by piggybacking off of the good credit of someone else. You could have someone you trust cosign on a loan or open a joint account with you, or you could become an authorized user on someone else’s seasoned tradeline.

If you are not lucky enough to know someone who has a seasoned account with perfect payment history that they could add you to, consider purchasing tradelines from a reputable tradeline company.

Myth: Paying off a collection will “re-age” the debt because the account falls off your credit report based on the date of last activity.

Fact: Collections fall off your credit seven years after the initial delinquency and cannot legally be re-aged.

It is illegal to “restart the clock” on collections.

If you’ve read our article about collections on your credit report, then you know that it is the date of first delinquency (DOFD) that determines when the collection will be removed from your credit report, not the “date of last activity” (DLA).

The reason why some people may believe this myth is because shady debt collectors sometimes illegally change the date of first delinquency to the date of last activity in an attempt to re-age the debt.

As we said, this practice is illegal. If you notice that a debt collector has improperly changed any information about a collection account on your credit report, you have the right to dispute the inaccurate information.

Myth: Paying off a collection will boost your credit score.

Fact: Paying off a collection may or may not raise your score depending on which credit score is used.

While it makes sense to assume that paying off a collection should increase your credit score, that is not always the case. In fact, more often than not, this is not the case, although it depends on which credit score is being used.

With FICO 8 and all previous FICO scores, both paid and unpaid collections are categorized as major derogatory items on your credit report. Therefore, paying off the account will not change how it is considered by the credit scoring algorithm, which means your score may not go up at all.

On the other hand, FICO 9, VantageScore 3.0, and VantageScore 4.0 ignore paid collection accounts, so your score should recover after paying off a collection if one of these credit scoring models is being used.

Myth: You should close accounts you’re not using.

Fact: You should keep accounts open and use them periodically.

While you might think that closing accounts you don’t need will help your credit score, the opposite is actually true, especially when it comes to revolving accounts such as credit cards.

The main reason for this is that credit utilization is an important part of your credit score, and closing credit card accounts will hurt your utilization ratio by decreasing your credit limit.

It could also hurt your mix of credit, although that’s a less important factor.

In addition, payment history is the number one factor that helps your score. It’s better for your credit to keep the account open, use it for small purchases here and there or a monthly subscription, and pay it off every month to keep building more positive payment history.

The exception to this is if an account comes with an annual fee that’s no longer worth the price or if you can’t resist the temptation to overspend.

Myth: Closed accounts don’t affect your credit.

Fact: Closed accounts can have a significant impact on your credit.

Although we just discussed why you shouldn’t necessarily close old accounts, that’s not to say that closed accounts don’t impact your credit. They certainly can, particularly when it comes to your credit age.

Closing an account does not remove its payment history or age from your credit report, so closed accounts still contribute to your credit age. In addition, accounts can continue to age even after they have been closed.

So although it’s best to keep accounts open if you can, having closed accounts on your credit report is not a bad thing. If the account was closed in good standing, it will likely continue to help your credit.

Carrying a balance on your credit cards is expensive and does not help you build credit. Photo by Hloom on Flickr.

Myth: Carrying a balance on your credit cards will help your credit.

Fact: Carrying a balance will not help you build credit and it will cost you interest fees.

While it is important to use credit regularly when building credit, it’s not necessary to carry a balance on your credit cards from month to month. If you do this in an attempt to build credit, you will be wasting money by paying unnecessary interest.

The best way to build credit using your credit cards is to use them responsibly and then pay the full balance due each month, or even make multiple payments each month to keep your utilization ratio as low as possible.

Myth: Shopping around for the best rates on a loan will hurt your credit score.

Fact: Getting loan estimates from multiple lenders will not hurt your score if you complete the process within a specific time window.

Credit scoring algorithms understand that it’s smart to shop around for the best rates on a loan, not risky. Therefore, credit scores typically have ways of preventing the series of multiple inquiries that result from this process from hurting your score excessively.

If you are applying for student loans, mortgages, or auto loans, FICO scores allow a certain time frame for you to shop around, only counting one hard inquiry to your credit report for this time period. For older FICO scores, the time window is 14 days; for newer FICO scores, the time window is 45 days.

In addition, FICO scores have a 30-day hard inquiry “buffer,” meaning that the algorithm ignores any inquiries that occurred within the past 30 days when calculating your score.

VantageScore uses a simpler method: it groups all inquiries made within a 14-day window of each other together and counts those all as one inquiry, regardless of what types of accounts the inquiries were for.

Myth: You can fix your credit by disputing everything on your credit report.

Fact: Disputing everything on your credit report could get you in legal trouble and may not even help your credit.

If there is information on your credit report that is inaccurate, outdated, incomplete, or unverifiable, of course you would want to dispute those items with the credit bureaus. But it’s not necessarily a good idea to dispute negative items on your credit report that are accurate.

First of all, the derogatory items won’t necessarily get deleted from your credit report, especially if you don’t provide proof that they are inaccurate. They might just get updated with the correct information, or they may get deleted temporarily until an investigation determines the items are valid and they go right back on your credit report.

Furthermore, the credit bureaus don’t have to investigate disputes that are deemed “frivolous,” and they could decide that some of your disputes are frivolous if you are disputing every item in your credit file, regardless of accuracy.

Plus, lying on a credit dispute could be considered fraudulent. According to the FTC, “No one can legally remove accurate and timely negative information from a credit report.”

Even if you were to get away with disputing everything on your report, this might not necessarily help your credit as much as you hoped. If you’ve gone through an aggressive credit sweep and have nothing left on your report, then you essentially have no credit history and likely no credit score, which could be just as problematic as having bad credit.

Myth: CPN numbers can be used in place of social security numbers to create a new, clean credit file.

Using a CPN to apply for credit is a federal crime. Photo via seniorliving.org.

Fact: CPNs are illegal and using one to apply for credit is a federal crime.

Although you might have heard some people claim that “credit profile numbers” or credit privacy numbers” are a legitimate way to protect your privacy or wipe your credit slate clean, in reality, there is no legitimate or legal source for CPN numbers.

Most of the time, these numbers are either fake social security numbers that have not been created yet or real SSNs that have been stolen from children, the elderly, deceased people, people who are incarcerated, and people who are homeless. Either way, using a CPN means getting involved in identity fraud, which is a federal crime.

Myth: The credit score you check online is the same one lenders see when they pull your credit.

Fact: Lenders often do not use the same credit scores that are provided for free online.

When you check your credit score for free online, the credit score you see is most likely going to be a VantageScore. This is the score most commonly used by free online services such as Credit Karma.

The majority of lenders, however, primarily use FICO scores, although some lenders are now starting to use VantageScore. Just keep in mind that the score you see online may not be the same as the score lenders see, as there can often be a significant difference between your VantageScore and your FICO score.

If you want to check your FICO score for free, check with your credit card issuer, since many now offer this service.

Myth: If you don’t have any debt, you will have a good credit score.

Fact: You need to use credit to build your credit score.

Having good credit doesn’t just come down to the amount of debt you have—that’s just one part of your credit score. Payment history is the most important part of a credit score, so if you’ve never had debt and you don’t have any payment history, you might not even have a credit score at all.

To get a good credit score, you have to use some form of credit and demonstrate that you can use credit responsibly by building up a positive payment history over time.

Myth: There’s no need to check your credit report until it’s time to apply for a big loan.

Fact: It’s important to monitor your credit regularly.

Waiting to check your credit score until you need to apply for credit is a mistake because there could be errors on your credit report bringing your score down. Studies estimate that about one-fifth of consumers have at least one error on their credit report, some of which could be serious enough to result in higher interest rates, less favorable loan terms, or being denied credit.

It’s important to keep an eye on your credit so that you can correct errors and fight fraud as soon as possible instead of waiting until it’s too late.

Myth: A late payment will make your score go down by 50 points.

Fact: There is no set amount of points that is associated with any particular item on your credit report.

While it is certainly possible that a 30-day late payment could cause a 50-point drop (or more) in someone’s credit score, this is not always going to be the case. There is no fixed number of points that your score will go up or down by for each item on your credit report. Rather, the way in which a late payment affects your score is always going to depend on your individual credit profile.

There is no set amount of points associated with missing a payment.

Credit scoring algorithms are very complex and they incorporate hundreds of variables, such as how recent the late payment is, whether you have other late payments in your credit history, and how severe the delinquency is, not to mention the myriad other variables associated with the other categories within a credit score.

Because delinquencies on your credit report are always going to be relative to whatever else is in your file, there is a “diminishing returns” effect where the first late payment hurts your score the most and each subsequent late payment tends to have a smaller impact. Someone who has a high credit score and has never missed a payment before is going to experience a severe drop from their first missed payment, whereas someone who already has lates on their record and a lower credit score is going to be hurt less by a subsequent late payment.

According to credit expert John Ulzheimer in a blog article, “Delinquencies, like inquiries, do not have independent value… It is entirely inappropriate and incorrect to say that ‘X’ lowered my score by ‘Y’ points.”

He continues, “The late payment didn’t lower your score but because adding a late payment to a credit report moves other things around it caused your score to be different than it was before the late payment was added. If your score is 50 points lower it’s not as if the new late payment lowered your score 50 points…but because the addition of that item caused a different evaluation of EVERYTHING on your credit reports…the new reality for you is 50 points lower.”

The same principle goes for other items on your credit report as well, not just late payments.

Myth: You don’t have to worry about your kid’s credit.

Fact: You should keep an eye on your kid’s credit report, too.

The proliferation of scammers and hackers stealing people’s private information means even your kid’s credit profile could be at risk of identity theft. When people use “credit profile numbers” (CPNs), for example, these numbers are often real social security numbers stolen from children.

Make sure you monitor your kid’s credit in addition to your own.

You don’t want to wait until your child is grown up and ready to apply for credit to realize they have bad credit as a result of identity theft. Consider freezing your kid’s credit to prevent fraudsters from opening accounts in their name.

Myth: Everyone’s credit score is calculated in the same way.

Fact: Credit scores have “scorecards” that categorize consumers and score them differently.

You already know that credit scoring algorithms are extremely complex, but what many people don’t know about is the “scorecards” or “buckets” within each credit scoring model. These “buckets” consist of different categories of consumers.

For example, according to John Ulzheimer, “There are scorecards for thin files or those with few accounts, bankruptcy, derogatories, and those with clean credit files… Comparing like populations gives this population an opportunity to be considered based on [the] behavior of that group rather than a comparison to another, better group.”

The credit scoring formula is different for each bucket. In other words, items on your credit report can be treated differently based on which scorecard you fall into.

Sometimes your credit score changes in a way that you don’t expect. For example, perhaps an inaccurate collection account got deleted off of your credit report and your score went down, instead of up. This could be because you changed scorecards as a result of the deletion, causing your credit score to be calculated in a different way. Essentially, you might now be at the bottom of a different bucket instead of at the top of your previous bucket.

It’s always good to keep the concept of scorecards in mind, especially when trying to predict any kind of change to your credit score. You can never guess exactly how your score will change because of all the complexities and trade secrets that go into credit scores.

Conclusions

Unfortunately, there are tons of credit myths out there, and believing them may lead you to mismanage your credit and eventually end up with poor credit. We hope that this article helped to dispel many of the misconceptions about credit and helped you get started on the path to better credit.

What credit myths have you heard of? Did you use to believe any of these? We’d love to hear from you, so share your experience with us in the comments!

Credit mix, also called mix of credit, is one of the factors that your credit score takes into account. It is one of the least important factors, weighing in at 10% of a FICO score.

Credit mix is the diversity of types of credit accounts in your credit report. Having different types of credit accounts in good standing in your credit file demonstrates that you can use credit responsibly. Lenders ideally want to see that you have successfully managed a diverse mix of multiple types of accounts.

Types of Credit Accounts

Depending on how you define the types, there are 3-4 general categories when it comes to types of credit.

Revolving credit is a form of credit with which you can “revolve” or carry a balance each month. You are assigned a credit limit that you can charge up to and you make a payment each month. Interests will typically be charged if you carry a balance from month to month. Credit cards and lines of credit are the most common types of revolving credit accounts.

Charge cards are similar to credit cards, except the balance must be paid in full every month.

Service credit includes accounts with your service providers, such as utilities, cell phone service, etc. These are considered credit accounts because the service is provided before you pay the bill.

Installment credit is a loan of a specific amount of money that you pay back in regular payments of the same amount over a certain period of time. Types of installment loans include car loans, mortgages, student loans, etc.

Credit Karma simplifies the categories to 3 types of credit:

Revolving credit

Open credit (includes charge cards)

Installment credit

Examples of Revolving Credit

As we touched on above, the two most common types of revolving credit are credit cards and lines of credit.

Credit cards include those issued by banks such as Capital One, Bank of America, and Chase, as well as store cards, which can typically only be used at a particular retailer.

Lines of credit are similar to credit cards in that you have access to a set amount of money—your credit limit—that you can draw from. After you borrow money from your line of credit, the balance starts accruing interest, and when you pay it back, that credit is then available again for you to use. This is why it’s considered revolving credit: you can use it again and again as long as you keep paying it back.

Types of Lines of Credit

A home equity line of credit (HELOC) is secured by your home.

Lines of credit can be either secured, which means the borrower has provided collateral to back the line of credit in case of default, or unsecured, meaning no collateral is required.

Beyond those general categories, there are three main types of lines of credit.

A home equity line of credit (HELOC) is a line of credit secured by your equity in your home, which is the difference between the value of your home and the amount you still owe on your mortgage. Since your home equity serves as collateral, if you default on a HELOC, you could risk losing your home to foreclosure.

A personal line of credit is usually unsecured, although sometimes you may be able to provide collateral in the form of savings or investments.

A business line of credit may be secured or unsecured. They are offered by financial institutions as well as many commercial vendors.

Examples of Installment Loans

An auto loan is one type of installment account.

Types of installment credit include:

Auto loans

Mortgages

Student loans

Personal loans Credit-builder loans

Home equity loans (not to be confused with a HELOC, which falls under revolving credit)

The breakdown of account types outlined above is a simplified version of how credit scoring systems actually categorize different types of accounts. In reality, credit scoring models may consider as many as 75+ account types.

In addition, each type of account could have a different effect on your credit.

How Does Credit Mix Affect Your FICO Score?

As we mentioned at the top of this article, credit mix makes up about 10% of your FICO score. With VantageScore, type of credit and credit age are combined into the same category, which makes up approximately 21% of your VantageScore.

With both types of scores, credit mix is a relatively small portion of what determines a credit score, so having the perfect credit mix is not necessarily essential in order to have good credit. However, it’s still a good thing to aim for, especially if you want to get a perfect 850 credit score or somewhere close to it.

What Is a Good Credit Mix?

When it comes to your credit score, the most important thing is to demonstrate that you have managed both revolving and installment accounts. Therefore, it’s best to have at least one type of account of each type.

FICO high score achievers have an average of seven credit cards on their credit reports. Photo by Hloom on Flickr.

For example, you might have a credit card (revolving) and an auto loan (installment). Or, you could have a mortgage (installment) and a HELOC (revolving). Any combination of one revolving account and one installment account is a good start for your credit mix.

FICO supports this idea, saying, “Having credit cards and installment loans with a good credit history will raise your FICO Scores.”

FICO also says that people who have managed credit cards responsibly are better off than consumers that don’t have any credit cards, who can be seen as risky because they have not demonstrated experience in using revolving credit.

Statistics show that high FICO score achievers have an average of seven credit cards on their credit reports, which includes both open and closed accounts.

People with credit scores in the 800s also typically have installment loans such as mortgages and auto loans, according to Experian.

The total number of accounts in your file may also play a role. FICO has indicated that those with high credit scores can have 20+ credit accounts in their credit reports.

How Many Credit Cards Is Too Many?

Having too many credit card accounts could hurt your credit score.

Keep in mind that it is possible to have too many accounts on your credit file. According to the FTC, having too many credit cards could have a negative effect on your credit score, as could having loans from some types of companies.

There is no hard-and-fast rule when it comes to how many credit cards is too many because the impact of any given factor on your credit score depends on what is already in your credit profile, says FICO.

However, in figure 1 in the article “How Credit Actions Impact FICO Scores,” the hypothetical consumer “Rachel,” who has 33 credit accounts, has a lower credit score than “Maria,” who has 21 accounts. This would seem to imply that at some number between 21 and 33 accounts, one’s credit score might begin to suffer. However, these two consumers have other differences in their credit profiles, so the difference in their credit scores cannot be solely attributed to the number of accounts in their files.

Can Some Account Types Hurt Your Credit?

Certain types of loans on your credit report could make you seem like a more risky consumer and therefore could end up hurting your score instead of helping.

Why? It’s all based on statistics and who the credit score algorithms have deemed to be risky borrowers.

For example, taking out a furniture loan could actually drop your credit score. That’s because furniture loans are often reported as “consumer finance loans,” which are typically reserved for borrowers with bad credit who are statistically more likely to default on loans. Therefore, having this type of account on your credit report could be viewed as risky by lenders and credit scoring algorithms.

Alternatively, the financing arrangement may be reported as revolving debt, which will appear nearly maxed out until you make enough payments to get the balance to a lower level.

Payday and title loans, however, are typically not reported to the credit bureaus, so these types of loans won’t count toward your credit mix or credit score—unless, of course, you default on a loan and it gets sold to a collection agency, who will then report it as a collection account.

Conclusions on Credit Mix

Since credit mix makes up about 10% of your credit score, it is helpful to try to achieve a balanced mix of credit by keeping a few revolving and installment accounts in good standing. The best credit mix should ideally include a few credit cards and at least one or two installment loans, such as mortgages or auto loans.

However, it’s also important to note that credit mix is much less important than other credit score factors, such as payment history, credit utilization, and credit age. It’s probably not worth obsessing over because you won’t automatically get an excellent credit score just by having the perfect mix of accounts.

In addition, most people naturally accumulate different types of accounts over time, so it’s not necessarily the best idea to start opening new accounts left and right just to build up your credit mix. This strategy could result in lots of inquiries and new accounts bringing your score down in the short term, and having access to credit you don’t need could also encourage extra spending.

As with all credit-related decisions, it’s up to you to take your overall financial goals and priorities into account before taking action. You might decide that you don’t need to worry too much about improving your credit mix, and that’s fine. On the other hand, improving your credit mix can only help your credit score, and it is something that you should pay attention to if you want to get a perfect 850 credit score.

One of the more common questions I receive from consumers is how they can best establish credit or improve their credit scores. It’s a hard question to answer without seeing their credit reports. There are many paths to poor credit scores so the advice isn’t as simple as one universal answer. The answer is going to vary based on each consumer’s individual credit situation.

As to the “how can I establish credit” question, that one is certainly easier to answer because there is a finite number of options to choose from when building or rebuilding a credit report and a credit score. My favorite option is the same one my parents used some 33 years ago when I was 18 years old and headed off to college. My father added me as an authorized user on one of his credit cards.

If you’re not familiar with authorized users, you can read more about them here. Or, I can save you some time; an authorized user is someone who is added to the credit card account of another person. The authorized user has the same spending permissions as the primary cardholder, but without any of the payment or debt liability. Almost all large credit card issuers will allow their primary credit card holders to add authorized users to their accounts.

The upside to being an authorized user is most credit card issuers will report the history of the credit card account to your three credit reports as maintained by Equifax, Experian and TransUnion. This means not only will lenders see the account on your credit reports but, also, credit scoring systems will consider it when calculating your credit scores.

Authorized Users and Credit Scoring

All commonly used credit scoring systems will consider an authorized user account or “tradeline” as a scored attribute. In English that means if you’re an authorized user on someone else’s credit card account and that account is reported or “furnished” to the three consumer credit reporting agencies, and it ends up on your credit reports, then it will be considered in the calculation of your credit score.

In most scenarios an authorized user credit card account is treated no differently than if you were the primary cardholder. The balance, the credit limit, the age of the account, and the account’s payment history would be treated no differently. If all of those credit card attributes say good things about you, the card will likely help your credit scores. And conversely, if the card is mismanaged then you too will likely suffer a credit score impact, just like the primary cardholder.

There was a time many years ago when authorized users were being abused as a credit repair strategy to temporarily boost consumer credit scores. The response…in June of 2007 the primarily used credit scoring company announced that they would no longer count authorized user accounts in their upcoming credit scoring system. The reason they gave was that by no longer counting authorized user accounts in the calculation of a credit score they would be protecting lenders from the practice of piggybacking on someone else’s credit card account.

Thankfully the company reconsidered their position after consulting with the Federal Reserve Board and the Federal Trade Commission. Instead of simply ignoring authorized user tradelines, the company instead implemented logic into their future credit scoring models that reduced the potential impact from piggybacking. [1] The specifics as to the exact treatment of authorized user tradelines by these newer credit scoring systems have never been publicly disclosed.

How Authorized User Tradelines are Helpful

Assuming an authorized user tradeline makes its way to your credit reports, it can be helpful in a variety of ways, which I alluded to above. First and foremost, lenders like to see positive information on credit reports, and that has nothing to do with your credit scores.

If the authorized user account is old, it will help to increase your average age of accounts, which is an important factor in your credit scores. If the authorized user account has a clean payment history, that is helpful to your credit scores. And, maybe most importantly, if the authorized user account has a low balance relative to the credit limit, that is very helpful to your credit scores.

Really the only way an authorized user account can hurt your credit scores is if you choose to associate yourself with a poorly managed account. For example, you’d never want to have your name added to an account that had a history of late payments. And, you’d never want to associate your name with an account that has a large balance relative to the credit limit. These are score damaging qualities of a tradeline, which would certainly point your credit scores in the wrong direction.

[1] From the Written Statement of Fair Isaac Corporation before the U.S. House of Representatives Committee on Financial Services Subcommittee on Oversight and Investigations.

John Ulzheimer is a nationally recognized expert on credit reporting, credit scoring and identity theft. He is the President of The Ulzheimer Group and the author of four books about consumer credit. Formerly of FICO, Equifax and Credit.com, John is the only recognized credit expert who actually comes from the credit industry. He has 27+ years of experience in the consumer credit industry, has served as a credit expert witness in more than 370 lawsuits, and has been qualified to testify in both Federal and State courts on the topic of consumer credit. John serves as a guest lecturer at The University of Georgia and Emory University’s School of Law.

Disclaimer: The views and opinions expressed in this article are those of the author John Ulzheimer and do not necessarily reflect the official policy or position of Tradeline Supply Company, LLC.

Collections are one of the worst things to have on your credit report. They can damage your credit score significantly for a long time—up to seven years. This helpful guide explains what collections are, how they affect your credit, how collection agencies try to re-age debt, how to get collections removed from your credit report, and more.

What Is a Collection Account?

A collection account is a debt account that has been sold by the original creditor to a third-party debt collection agency. This happens you (the borrower) are delinquent on payments long enough (generally 180 days) for the lender to charge off the loan, which means they consider the account to be a loss—but that doesn’t mean you’re off the hook.

Once the account has been charged off, the original creditor closes your account and often transfers or sells it to a debt collection agency or a debt buyer. (Debt buyers typically focus on purchasing debt accounts and they hire debt collection companies to attempt to collect the debt.)

When Does the 7 Year Credit Rule Start on Your Credit Report?

Regardless of who the debt was transferred to or when it was transferred, the Fair Credit Reporting Act (FCRA) allows collections to legally be reported by the credit bureaus for up to seven years after the date of the first delinquency (also known as “DOFD” for “date of first delinquency”).

The seven-year rule for collections begins on the date of first delinquency.

What does this mean exactly? How do you figure out the date of the original delinquency of an account?

According to Experian, the date of the original delinquency is the first reported late payment. As an example, if you have a 30-day late reported and never catch up on payments, then the delinquency would later get reported as a 60-day late and eventually as a 90-day late.

The seven-year period after which the delinquency falls off begins with the first missed payment, the 30-day late. If the debt is sold to a collection agency, the original account and the collection account will both be removed from your credit report seven years after the initial delinquency, says Experian.

Medical collections are slightly different in that a 180-day grace period must be provided to allow insurance benefits to be applied. Therefore, the seven-year timeline starts after 180 days, not after a 30-day late.

The date that a collection account is charged off or transferred to another company does not change the DOFD and therefore should not change the date that the delinquency falls off of your credit report.

How Often Do Collection Agencies Report to Credit Bureaus?

Collections agencies can begin reporting to the credit bureaus as soon as they acquire your account. After that, they will typically report to the credit bureaus every month, like most other types of tradelines on your credit report. Therefore, if you have a collection account, you will most likely see the collection agency reporting every month.

Should You Pay the Debt Collector or the Original Creditor?

If you already have an account in collections, meaning the original creditor has already closed your account and transferred it to another owner, you should not pay the lender that the loan was originally from. The debt now belongs to someone else, so it would be pointless to pay the original creditor.

How Do Collections Affect Your Credit Score?

Having one or more collection accounts on your credit report can quickly lead to bad credit. A collection account on your credit report means you failed to make sufficient payments on a debt, which is a big red flag to lenders that you might default on a loan again. Therefore, your credit score will likely suffer a significant drop if you have an account go to collections.

Collections are major derogatories, so they can lead to bad credit. afeCredit.com, CC 2.0.

However, collections with low balances may not impact your score at all, depending on which credit scoring model is being used to calculate your score, such as VantageScore or a FICO credit score.

FICO scores 8 and 9 ignore both paid and unpaid collections that had an original balance of less than $100.

FICO 9, VantageScore 3.0, and VantageScore 4.0 don’t count paid collection accounts against you and treat medical collections as less important than other types of collection accounts.

Unfortunately, with FICO 8 and previous versions of FICO, which most lenders today still use, all collections are highly damaging to your credit score, regardless of what type of account they are or whether the collections have been paid or not.

Does Paying Off Collections Improve Your Credit Score?

Unfortunately, paying off a collection won’t necessarily improve your credit score right away. Why?

As we said, with all FICO scores except FICO 9 (which is not widely used yet), both paid and unpaid collections are considered to be major derogatories on your credit report. Since a paid collection is still a major derogatory mark, paying off your collection likely won’t help your credit score if the scoring model used is FICO 8 or earlier.

On the other hand, since FICO 9, VantageScore 3.0, and VantageScore 4.0 ignore paid collection accounts, your score should rebound after paying off a collection with these credit scoring models.

Can a Collection Agency Change the Open Date of a Collection?

The open date of a collection is the date that the collection account was acquired by a debt collector. Every time the debt changes hands, the new collection account will thus have a new open date.

The open date does not affect how long the collection remains on your credit report because it’s the date of first delinquency (DOFD) that determines when the collection will be removed from your credit. While each debt collector will have a different open date, the DOFD cannot be changed unless it was reported incorrectly.

Can a Collection Agency Report an Old Debt as New?

You may have heard of another date pertaining to collection accounts: the “date of last activity” (DLA).

You might have heard it said that you should never make payments on a collection because that action would change the DLA on the account. If the DLA changes, so the advice goes, this “resets the clock” on the seven-year period after which the collection will fall off your credit.

In reality, debt collectors cannot change the DLA—only the credit bureaus can do that. Furthermore, the DLA does not affect the timeline of your collection account.

As we know, the seven-year period begins at the DOFD, not the DLA, and not the open date of the collection. The collection agencies are not legally allowed to change the DOFD, so there should be no legitimate way for them to “restart” the seven-year timeline. Yet there are many cases in which consumers report that their collection accounts are suddenly being updated as new accounts, even if they are several years old. What is going on in these situations?

This shady practice is the collection agency re-aging the debt.

It’s illegal to re-age a collection account by incorrectly changing the DOFD.

When a debt collector acquires an account, they sometimes improperly update the DOFD to be the same as the date opened. If you make a payment on the collection, they may replace the DOFD with the DLA, which is the date that you made the payment. This explains why the seven-year clock seems to restart in these situations.

But guess what? Re-aging a collection is illegal. Collection agencies cannot legally report an old debt as a new collection.

If a collection agency keeps updating your credit report with incorrect information and the date of first activity or the date opened on your credit report is wrong, you have the right to dispute that account and have it updated or removed from your credit report.

Double Jeopardy Credit Report

A “double jeopardy” credit report is when you have multiple collections for the same account on your credit report. This can happen when the debt is being reported by both the original creditor and the collection agency on your credit report or when the debt is sold to another collection agency.

Experian explains why there may legitimately be duplicate accounts on your credit report:

“When an account is charged off, or written off as a loss, it remains on your credit report for seven years from the original delinquency date leading up to the charge off.

Often, the original creditor will transfer or sell the account to a collection agency. In that case, the original account will be updated to show transferred/closed, and will no longer show a balance owed because the debt is now owed to the collection agency. However, your report will still show the history of the account, including the amount that was written off.

Since you now owe the collection agency, it will report the current balance owed.”

In this case, having multiple accounts for the same collection on your credit report is normal and should not change the impact the collection has on your credit score.

A true case of double jeopardy on your credit report involves duplicate collection accounts on your credit report being reported as open collections, which would be even more of a disaster for your credit than having a single open collection account.

Multiple Collection Agencies Same Debt

If your credit report looks as Experian describes, with the old collection accounts accurately reporting as closed, there may not be much you can do besides wait seven years for the collections to fall off your credit report.

However, if the original creditor and/or multiple collection agencies report the same debt as if they are all separate open collection accounts, that may be an error that you need to dispute with the credit bureaus.

How to Remove Collections From Credit Report

It may be possible to remove collections from your credit report depending on the situation.

How to Dispute a Collection on Your Credit Report

If a collection on your credit report is inaccurate or a duplicate collection account, you can dispute the collection account on your credit report. This doesn’t necessarily guarantee that the collection will be removed from your credit report, though, because the account could be updated with the correct information rather than removed.

How to Remove Paid Collection Accounts From Credit Report: Pay for Delete Collections

Even once you have paid a collection, you may find that it is difficult or impossible to remove it from your credit file. However, if you do want to try to remove zero balance collections from your credit report, one method that consumers use to do this is the “pay for delete” strategy.

You may be able to negotiate a “pay for delete” agreement with the debt collector.

With the pay for delete method, you negotiate with the debt collector to have them stop reporting the collection to the credit bureaus in exchange for your payment, whether you negotiate to pay the full amount owed or settle the debt for a lesser amount.

It may not be necessary to hire a pay for delete service, since you can look for a sample pay for delete letter online, although a credit repair service might be helpful in this situation as well.

Keep in mind that debt collectors are not obligated to accept the offer outlined in your deletion letter, so this strategy is not a guaranteed success.

If the collection agency does agree to delete the collection once you pay it off, it’s best to get verification of this agreement in writing before you make any payments.

Does Pay for Delete Increase Credit Score?

Remember that FICO 9, VantageScore 3.0, and VantageScore 4.0 don’t penalize paid collections, so it may not be a problem to have a paid collection on your credit report if your lender uses one of these credit scores. In this case, the deleted collection won’t increase your credit score.

However, with FICO 8 and earlier FICO scores, paid collections do hurt your credit, so a successful “pay for delete” arrangement could lead to a credit score increase after collection removal.

On the other hand, you may be shocked to learn that it is possible that deleting a collection could actually make your credit score go down. This is because there are certain scorecards or “buckets” within each credit scoring model that categorize consumers based on what is in their credit file and calculate their score differently depending on what bucket they are in.

As a hypothetical example, let’s say you have one collection on your file and you get that collection deleted. Perhaps you used to be in a scorecard of consumers with one or more major derogatories on file and after the deletion, you get reassigned to a different scorecard in which the consumers have no major derogatories. Since you are now in a higher bucket, your credit score would be calculated differently, and your score could actually decrease compared to what it was when you were in the lower bucket.

How to Remove Collections Without Paying

The only legitimate way to get an unpaid collection removed from your credit report is if the collection is more than seven years old or if it is being reported incorrectly.

If the collection is older than seven years, it should have been removed from your credit report already, so you can dispute that account with the credit bureaus to have it removed.

If the account is being reported inaccurately, such as if the date of first delinquency or the date opened on your credit report is wrong, you can also dispute the account and have it updated or removed as described above.

Conclusions on Collections

If you have a collection account on your credit file, you might end up with bad credit for a while, but it’s not the end of the world. Collections must be removed from your credit file after seven years whether they were paid or not, and the damage to your credit score will lessen as the collection ages.

Some credit scoring models don’t count paid collections against you, so you might see a credit score increase after paying off a collection. Alternatively, you could try to negotiate a pay for delete agreement with the debt collector.

If you have an old or inaccurate collection on your credit report, you can dispute this with the credit bureaus and have it corrected or removed.

Finally, the best thing to do to help your credit recover after a collection is to focus on building credit and maintaining a positive credit history going forward.

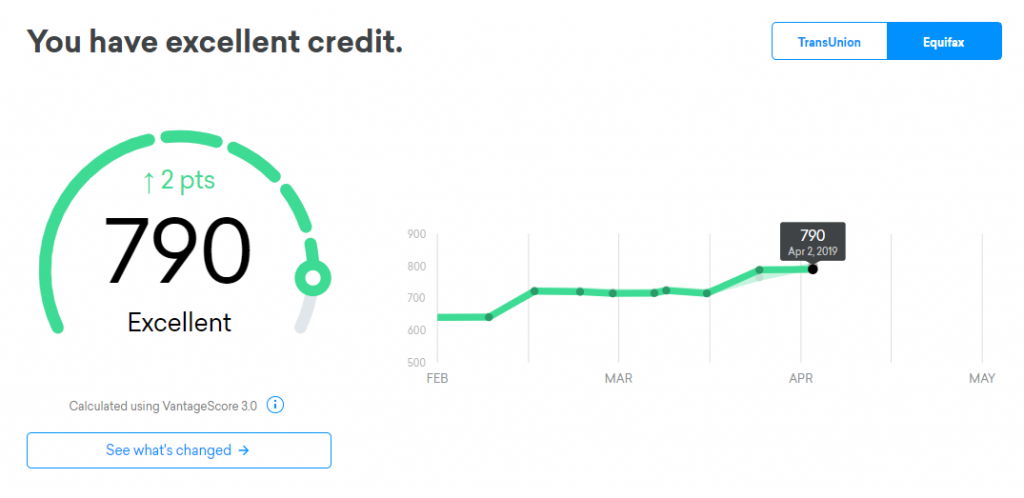

If you monitor your credit using a free website, chances are, you’ve seen your VantageScore. However, you may not realize that this credit score is not your FICO score.

So what is a VantageScore credit score and how is it different from a FICO credit score? Is one better than the other? We’ll compare and contrast the two types of credit scores and discuss the merits of each in this article.

What Is a Vantage Credit Score?

The VantageScore credit score, sometimes referred to as a “Vantage credit score,” is a credit scoring model created in 2006 by the three major credit bureaus (Experian, TransUnion , and Equifax) to compete with FICO’s credit scoring models.

VantageScore is a tri-bureau credit score, meaning the exact same model is used at each credit bureau.

The most commonly used version of the VantageScore used by lenders today is the third iteration of the credit scoring model, VantageScore 3.0.

VantageScore Solutions, LLC has released VantageScore 4.0, which is supposed to be more accurate than previous versions, but since it takes lenders a long time to adopt new credit scoring models, most are still using VantageScore 3.0.

Who Uses VantageScore?

According to Experian, VantageScore is used by lenders for all types of loans except mortgages, where FICO is still the dominant player. The largest group of financial institutions that uses VantageScore is credit card issuers.

Non-financial institutions have also increasingly been adopting VantageScore, such as landlords and utility providers.

VantageScore is also widely used by consumer websites that provide educational credit scores and market credit products.

What Is My Vantage Score?

It’s easy to find out what your VantageScore is for free. Credit Karma provides free VantageScore 3.0 credit scores from TransUnion and Equifax, so all you have to do is create an account on creditkarma.com and log in to your Credit Karma account to see your free Vantage credit score.

Credit Sesame and NerdWallet are other sites that provide consumers with free VantageScore 3.0 credit scores from TransUnion.

You can view your free VantageScore with TransUnion and Equifax on Credit Karma.

VantageScore vs. FICO Score

The primary difference between VantageScore and FICO scores is what they are used for.

FICO scores have been in use for a longer period of time and, consequently, are most widely used by lenders to make lending decisions. According to U.S. News, FICO scores are used by 90 percent of “top lenders.”

While VantageScore credit scores are also used by some lenders, they are more well-known for their use as an educational tool.

Both FICO and VantageScore consider the same general categories of information from your credit report (although they use slightly different terms to describe them), which include:

Payment history

Utilization

Length of credit history/age

Mix of accounts/types of credit

New credit activity/recent credit

Since the scores share the same general categories, it is safe to assume that they will both be bolstered by the same common sense behaviors that lead to good credit, such as not using too much of your available credit and not missing payments.

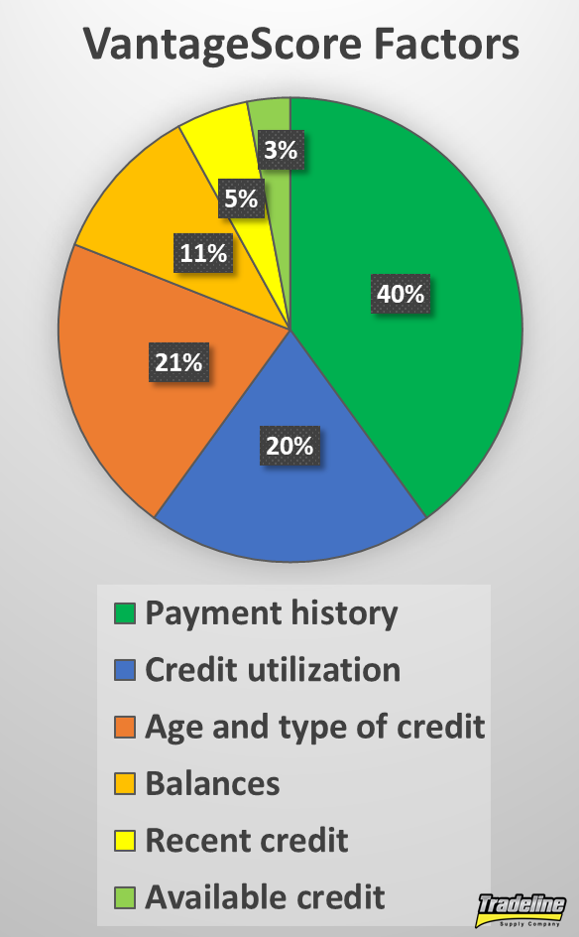

However, FICO and VantageScore assign slightly different weights to each category, as shown in the following table (percentage values are approximate).

FICO Score Factors

VantageScore Factors

Payment history, 35%

Payment history, 40%

Utilization, 30%

Credit utilization, 20%

Length of credit history, 15%

Age and type of credit, 21%

Mix of accounts, 10%

Balances, 11%

New credit activity, 10%

Recent credit, 5%

Available credit, 3%

FICO Score Factors

VantageScore Factors

In addition, within these broader categories listed above, the scoring models have different ways of assigning value to certain variables. Here are a few examples.

Inquiries

Hard inquiries can generally hurt your score by a few points because seeking new credit is considered risky behavior. When people are applying for some types of loans, such as mortgages, auto loans, and student loans, they tend to apply for multiple loans so they can shop for the best rates. Credit scoring models now have different ways of accounting for this behavior so as not to punish consumers for shopping around.

Newer FICO scores group inquiries of the same type together within a 45-day window. That means consumers could apply for 5 auto loans within 45 days and it would only count as one inquiry. Older FICO scores do this within a 14-day window.

FICO scores only apply this rule to student loans, mortgages, and auto loans—not credit cards. According to creditcards.com, the FICO scoring model also includes a 30-day “buffer” against hard inquiries, which means it ignores any inquiries that occurred within the last 30 days.

In contrast, VantageScore groups all inquiries within a 14-day window, regardless of the type of account. You could apply for some credit cards, a student loan, a mortgage, and an auto loan within 14 days, and it would only count as one inquiry.

Collections

Unpaid collections are always going to make a significant dent in one’s credit score, but paid collections and collections with small balances are treated differently between FICO and VantageScore.

With FICO 8, the credit score most widely used by lenders today, all unpaid and paid collections are damaging, regardless of the type of account. FICO 9, the newest FICO score, leaves out paid collection accounts and reduces the impact of unpaid medical collections specifically. Both FICO 8 and FICO 9 disregard collections when the original balance was less than $100.

VantageScore 3.0 and 4.0 are similar to FICO 9 in that they don’t count paid collection accounts and assign less importance to medical collections, but they do not make exceptions for collections with low balances.

Utilization

While utilization is treated fairly similarly with both scoring models, the specific thresholds that affect credit scores vary. VantageScore recommends keeping your credit utilization below 30%, while many experts believe that FICO scores suffer at lower utilization ratios.

Interestingly, the newer VantageScore 4.0 looks at the trends in your utilization over time, such as whether your balances have increased or decreased. FICO scores and previous VantageScore versions only look at the data that is in your credit report at the moment when your score is calculated and do not look “back in time.”

Other Differences Between VantageScore vs. FICO

Tri-bureau vs. single-bureau