In credit reporting, negative information can only stay on your credit report for a maximum of 10 years for a Chapter 7 bankruptcy and seven years for everything else—right?

The Fair Credit Reporting Act (FCRA) does mandate that the credit bureaus remove negative information from consumers’ credit reports within 7-10 years depending on the type of information.

While this is true most of the time, there are three exceptions to this rule, meaning that certain negative items could potentially stay on your credit report permanently.

1. If the consumer is applying for a job with a salary of $75,000 or greater.

If a consumer is going to apply for a job that pays $75,000 or more, and the employer uses a credit report as part of the employment screening process, the credit bureaus are allowed to include information on this report about derogatory events that occurred more than 7-10 years ago, such as an old bankruptcy or old collection accounts.

2. If the consumer is applying for a life insurance policy with a value of $150,000 or higher.

If a consumer applies for a life insurance policy with a value of $150,000 or higher, then the credit reporting agencies are technically allowed to include negative information that is more than 7-10 years old on the person’s credit reports.

3. If the consumer is applying for $150,000 or more in credit.

If the consumer applies for credit in the amount of $150,000 or more, this also qualifies as a case where the credit bureaus could include old negative information that normally would not be listed on the consumer’s credit report.

The interesting thing about this exception is that it includes most mortgages, meaning that if you apply for a mortgage today, there is a good chance that you could fall into this category of exceptions to the FCRA regulations regarding negative information.

Applying for $150,000 in credit qualifies as an exception to the 7-10 year rule, which means most mortgages could be included.

Should You Be Worried About Negative Items Staying on Your Credit Report Forever?

By now, you may be concerned that derogatory credit items that you thought were ancient history could haunt you in the future, in the event that you apply for a high-paying job, purchase life insurance, or apply for a mortgage.

However, there is no need to panic. While the credit bureaus are theoretically allowed to do this under the FCRA, that doesn’t mean that they choose to do so—and fortunately, they don’t.

Rather than maintaining old information to be used in specific situations, they simply default to applying the same 7-10 year policy across the board.

So if you do apply for a job that pays $75,000 or more, a $150,000 life insurance policy, or $150,000 in credit, you don’t have to worry about old negative items being revealed on your credit report.

Most of the time, when we talk about credit, we are talking primarily about the impact of open accounts. But are we underestimating the importance of closed accounts? Let’s shed some light on the less commonly addressed question of how closed accounts can affect your credit.

What Is a Closed Account on a Credit Report?

A closed account on your credit report is simply any credit tradeline that has been closed, whether it was terminated by the customer or the creditor.

There are several different reasons why an account may be closed.

If you don’t use your account for several months, it could get shut down for inactivity. Photo by Hloom on Flickr.

If you don’t use a credit card for several months, for example, you could get your credit card closed for inactivity. In this case, your credit report might say “account closed by credit grantor” for that account since the lender was the party who terminated the account.

Other reasons a credit card may be closed by the creditor include:

The credit card issuer is no longer offering that type of credit card or is replacing it with a different card

The credit card issuer determined that there was fraudulent activity on the account

The card was stolen or lost

Consumers may also want to close their own credit accounts from time to time, in which case the account might be notated as “account closed by consumer.” As an example, if one of your credit cards increases its annual fee or if you no longer feel that the fee is worth it, you might decide to close that account.

What Do Closed Accounts Mean on Your Credit Report?

Closed Accounts and Credit Utilization

Use our tradeline calculator to calculate your credit utilization ratios.

Now that you know what a closed account is and why an account may be closed, you may be wondering what a closed account on your credit report means for your credit.

The main impact of closing an account on your credit is the effect on your utilization ratio. By closing an account, you are reducing your total available credit limit, which could increase your overall utilization ratio if you have balances remaining on your other accounts.

Therefore, if you have balances on any of your other cards, you probably don’t want to close an account that is helping to keep your overall utilization down, as well as improving your ratio of low-utilization to high-utilization accounts.

On the other hand, if you pay down all your other credit cards to 0% utilization, you can safely close an account without impacting your credit utilization.

Many people believe that once an account is closed, it will no longer count toward your credit age. However, according to an article by credit expert John Ulzheimer in The Simple Dollar, this is a myth.

“Credit scoring models like FICO and VantageScore do indeed consider the age of your oldest account and the average age of your accounts when calculating your credit scores. However, closing an account does not remove its history — including its age — from your credit reports.

Not only will the history of a closed account remain on your credit reports, but credit scoring models will continue to consider the age of the account as well. And, even better, a closed account continues to age. So, if you closed a five-year-old credit card today… in 12 months it’s going to be a six-year-old credit card.”

Are Closed Accounts on Your Credit Report Bad?

Closed accounts on your credit report are not inherently a bad thing. In fact, they can often be a good thing, as we will elaborate on below.

Closed accounts on your credit report, unless they are derogatory, are not bad for your credit. In fact, they are probably giving your credit a boost.

However, derogatory closed accounts can definitely have a negative impact on one’s credit.

For example, if you had a credit card closed due to delinquency, meaning the creditor closed the account because you had stopped paying it, the account likely still has a balance owed.

Having a closed credit account with a balance on your credit report could really hurt your credit. According to some sources, closing a credit account removes its credit limit, so a credit card account closed with a balance would be considered maxed out or over-limit.

Credit utilization is a major influence on your credit score, so maxing out your utilization by having a credit card account closed with a balance could result in a big dip in your score.

However, other sources say that a closed account with a balance will be treated as an open account until the balance is paid off, at which point you can expect some damage to your score, especially if you have balances on your other credit cards.

The specific way that closed accounts are treated may depend on which credit score algorithm is used to calculate your score as well as other variables in your credit profile.

Should I Pay Off Closed Accounts on My Credit Report?

If your account was closed with a balance but remains in good standing, maintain its good standing by continuing to make payments until the account is paid off.

If your account was closed due to delinquency, the first thing to do is call your credit card issuer to check the status of the account. If the debt hasn’t been sold to a collections agency yet, you’ll want to start paying off the account immediately to prevent it from going to collections. You could end up with bad credit if you have a collection account on your file.

If the account is already in collections, however, whether or not you should pay it off is an entirely different question that depends on your individual situation.

See our article on collection accounts on your credit report for more information on how to handle collections.

Open vs. Closed Accounts on Credit Report

In the tradeline industry, we often get questions about whether closed accounts have an impact on one’s credit and, if so, what value they hold relative to open accounts.

It is possible to have a good credit score without having any open accounts. Photo by CafeCredit.com, CC 2.0.

This is an important question, because generally when you buy tradelines you are an active authorized user for two reporting cycles, and after you are removed from the account, it will begin to show as a closed account on your credit report.

Therefore, it is useful to know what impact the tradeline might have after it converts to a closed tradeline.

From what we have seen, closed accounts often can still be a very powerful influence on one’s credit score.

Remember, the age of a closed account still factors into your credit, and accounts continue to age even after they have been closed. Age and payment history go hand-in-hand and together make up 50% of a FICO score, and since closed accounts can still contribute to these factors, this implies that closed accounts can still have a strong effect on your credit.

However, closed accounts may have a diminishing impact over time, since credit scores tend to prioritize recent events.

Can You Have Good Credit With Only Closed Accounts?

It is possible to have a good credit score while only having closed accounts in one’s credit report. We have seen examples of people with credit scores in the 700’s who only had closed accounts in their credit file.

Can I Have Closed Accounts Removed From My Credit Report?

If you have closed accounts on your credit report that are not delinquent or hurting your credit, then there is no need to remove them. They may actually be helping your credit, even though they are closed.

Accounts that were closed in good standing should automatically fall off your credit report after 10 years, while delinquent closed accounts will fall off your credit report after 7 years.

How to Get Rid of Closed Accounts on Your Credit Report

If your credit card has been closed, you can try calling your credit card issuer to ask if the account can be reopened, but don’t wait too long.

If a closed account on your credit report is reporting inaccurately, then you can dispute it and have the credit bureaus update the account with the correct information or remove it.

Contact each credit bureau or check their websites for instructions on how to dispute accounts on your credit report.

If a Credit Card Is Closed, Can It Be Reopened?

In some cases, consumers may be able to reopen closed credit cards.

If your account was closed due to fraud or delinquency, banks typically do not allow these accounts to be reopened.

If it was closed voluntarily on your part or closed due to inactivity, however, you might have a chance to reopen the account if you don’t wait too long.

Only some banks will allow this, and those that do have varying time limits as to when you can reopen an account, so check with your credit card issuer.

If you’re within the time window and your account is eligible to reopen, here’s how to reopen a closed credit card account:

Call the phone number provided on the back of your credit card (or if you don’t have the physical card anymore, look up the phone number for the customer service department for that card).

Be ready to provide your personal information and answer security questions.

Explain why you closed the account and why you are requesting to reopen it.

Some issuers may require a hard inquiry before they can approve your request, which could cause a small, temporary drop in your credit score.

If your bank doesn’t allow you to reopen the card, the next best solution might be to re-apply for the same card or apply for a new credit card altogether.

Take-Home Points About Closed Accounts

Accounts may be closed voluntarily by the consumer or closed by the creditor due to inactivity, fraudulent activity, or delinquency.

Closed accounts are not necessarily bad and can even help your credit.

Closing an account could affect your credit utilization.

Closed accounts still contribute to your credit age and they continue to age even after they are closed.

Closed accounts can still have a powerful impact on credit scores.

Continue paying off accounts that were closed with balances to prevent them from going to collections.

You can dispute closed accounts that are not reporting correctly.

You may be able to reopen a closed credit card account depending on the circumstances.

What is credit piggybacking? If you’re not sure what this strange term could possibly mean, you’re definitely not alone.

Credit piggybacking, also referred to as “credit card piggybacking” or “piggybacking credit,” is a commonly used credit-building strategy. However, many people are still unaware of how to access this strategy and use it to their advantage.

In this article, we’ll define what piggybacking for credit means and how it can help your credit.

Credit Piggybacking Definition

The general definition of credit piggybacking is building credit by sharing a credit account with someone else. For example, spouses, business partners, and parents and children are all common examples of people who often share credit.

There are three main ways in which credit piggybacking can take place, which we discuss in more detail in “The Fastest Ways to Build Credit”:

Opening an account with a cosigner or guarantor is one way to piggyback on someone’s good credit.

Opening an account with a cosigner or guarantor, which is someone who promises to be responsible for the debt if the primary borrower cannot repay it. If the cosigner or guarantor has good credit, the borrower may be able to qualify for credit that they could not qualify for on their own or qualify for better terms.

Opening a joint account with another person, which means both parties have full access to the account and are both held fully responsible for the account. By opening a joint account with a partner who has good credit, a person with less-than-ideal credit may be able to open an account that they wouldn’t have qualified for on their own or get more favorable terms.

Becoming an authorized user for the purpose of credit card piggybacking, meaning you are not responsible for the debt, but the entire history of that account may be reflected in your credit file, regardless of when you were added to the account.

When people talk about piggybacking credit, they are usually referring to the method of piggybacking using authorized user tradelines.

How Does Authorized User Piggybacking Work?

Here’s how piggybacking works as an authorized user:

When you are added as an authorized user to someone’s credit card, often (depending on the bank), the full history of that account will then be shown in your credit report, regardless of when you were added to the card.

Therefore, piggybacking can almost instantly add years of perfect payment history to the authorized user’s credit file.

Authorized user tradelines can affect many important credit variables, such as your average age of accounts, age of oldest account, overall utilization ratio, number of accounts, mix of accounts, and more.

Historically, only the wealthy and privileged were able to use piggybacking as a credit-building strategy. Now, there is a marketplace where tradelines can be bought and sold, which is helping to democratize the credit system and provide equal credit opportunity.

The issue of piggybacking went all the way to Congress, which upheld consumers’ rights to use authorized user tradelines.

Is Piggybacking Credit Legal?

While Tradeline Supply Company, LLC does not provide legal advice, we can provide evidence that supports the idea that piggybacking credit is legal.

Firstly, piggybacking for credit is an extremely common practice that has been in use since the advent of credit cards. Studies estimate that 20-30% of Americans who have credit records have authorized user accounts in their credit file.

In addition, about 25% of people who have credit reports initially established their credit files by piggybacking in one way or another.

Many banks actually encourage consumers to add authorized users for the express purpose of boosting their credit scores.

You may have heard about FICO trying to take away authorized user privileges in 2008. But what you probably didn’t hear about was FICO backing down after a congressional hearing that involved the Federal Trade Commission and Federal Reserve Board.

During the hearing, FICO admitted that they could not legally discriminate between spousal AUs and other users, because this would unlawfully violate the Equal Credit Opportunity Act.

Since the U.S. Congress has upheld consumers’ rights to use authorized user tradelines, it seems reasonable to conclude that authorized user tradelines are legal.

However, it is important to get your tradelines from a reputable source. Some tradeline companies use illegal credit profile numbers (also known as CPNs) to mislead creditors as well as consumers. That’s why consumers should only work with tradeline companies that don’t use or sell CPNs—learn more about CPNs and why Tradeline Supply Company, LLC does not accept them.

Does Piggybacking Credit Still Work?

As we discussed in “Do Tradelines Still Work in 2020?”, credit piggybacking still works, and we think it will be around for a long time.

Piggybacking credit is a well-established credit-building strategy that has been defended in Congress and promoted by banks. It is a significant part of our credit system.

Thanks to the Equal Opportunity Credit Act, authorized user tradelines are still a very important factor in credit scoring models.

Not only that, but even if FICO were to devise an algorithm intended to exclude piggybackers, it would be quite some time before lenders could implement it on a large scale. The slow-moving financial industry is still using FICO scores that were developed decades ago.

Piggybacking companies bring together buyers and sellers of authorized user tradelines.

What Do Piggybacking Companies Do?

Friends and family will often allow each other to piggyback, but for many people, it’s difficult to find someone with good credit to piggyback on. A third party can play a role in helping to connect people who are looking to purchase seasoned tradelines with people who have high-quality tradelines to offer.

Piggybacking companies, more commonly referred to as tradeline companies, simply facilitate the buying and selling of authorized user tradelines.

The tradeline company acts as an intermediary by marketing the tradelines to consumers, protecting the identities of the clients, and preventing fraud.

At Tradeline Supply Company, LLC, we provide an innovative platform through which users can buy and sell tradelines entirely online. We also provide educational resources so consumers can familiarize themselves with the credit system and how piggybacking works.

How Long Does Piggybacking Credit Take Before I See the Tradelines on My Credit Report?

The account you are piggybacking on can show up on your credit report in as little as 11 days, depending on several factors relating to the particular tradeline.

Each piggybacking tradeline has its own reporting cycle, and Tradeline Supply Company, LLC provides a “purchase by date” before which you must purchase your tradeline in order for us to guarantee that it will post in the coming reporting cycle. If you miss the purchase by date, it will simply show up in the following cycle.

If you have purchased a seasoned tradeline that you believe has not posted, first, check to make sure that the entire reporting period has passed, then check your credit reporting service again to verify that it still has not posted. If you take these steps and determine your tradeline has not posted, please reach out to us for support and we will rectify the situation.

Can Piggybacking Hurt Credit?

If credit piggybacking is done incorrectly, it can actually backfire and hurt your credit.

Because the full history of the credit account is reflected in the credit file of the piggybacker, that means any derogatory factors will show up, too.

For example, if the account has any late or missed payments, that could hurt the authorized user rather than help. Similarly, a high utilization ratio on the account could also damage the authorized user’s credit.

That’s why we recommend going with a reputable piggybacking company who guarantees a perfect payment history and a low utilization ratio (15% or lower) on all tradelines. This will virtually eliminate the risk of your credit being hurt by these factors.

The only other way piggybacking could hurt your credit is if you choose the wrong piggybacking credit card. It’s essential to choose the right tradelines for your credit file. To do this, you’ll need to figure out your average age of accounts and how adding a tradeline could affect this statistic.

For example, if your average age of accounts is five years and you decide to piggyback on a tradeline that is two years old, this would bring down your average age of accounts, which is the opposite of what you want to achieve with tradelines.

Credit mix, also called mix of credit, is one of the factors that your credit score takes into account. It is one of the least important factors, weighing in at 10% of a FICO score.

Credit mix is the diversity of types of credit accounts in your credit report. Having different types of credit accounts in good standing in your credit file demonstrates that you can use credit responsibly. Lenders ideally want to see that you have successfully managed a diverse mix of multiple types of accounts.

Types of Credit Accounts

Depending on how you define the types, there are 3-4 general categories when it comes to types of credit.

Revolving credit is a form of credit with which you can “revolve” or carry a balance each month. You are assigned a credit limit that you can charge up to and you make a payment each month. Interests will typically be charged if you carry a balance from month to month. Credit cards and lines of credit are the most common types of revolving credit accounts.

Charge cards are similar to credit cards, except the balance must be paid in full every month.

Service credit includes accounts with your service providers, such as utilities, cell phone service, etc. These are considered credit accounts because the service is provided before you pay the bill.

Installment credit is a loan of a specific amount of money that you pay back in regular payments of the same amount over a certain period of time. Types of installment loans include car loans, mortgages, student loans, etc.

Credit Karma simplifies the categories to 3 types of credit:

Revolving credit

Open credit (includes charge cards)

Installment credit

Examples of Revolving Credit

As we touched on above, the two most common types of revolving credit are credit cards and lines of credit.

Credit cards include those issued by banks such as Capital One, Bank of America, and Chase, as well as store cards, which can typically only be used at a particular retailer.

Lines of credit are similar to credit cards in that you have access to a set amount of money—your credit limit—that you can draw from. After you borrow money from your line of credit, the balance starts accruing interest, and when you pay it back, that credit is then available again for you to use. This is why it’s considered revolving credit: you can use it again and again as long as you keep paying it back.

Types of Lines of Credit

A home equity line of credit (HELOC) is secured by your home.

Lines of credit can be either secured, which means the borrower has provided collateral to back the line of credit in case of default, or unsecured, meaning no collateral is required.

Beyond those general categories, there are three main types of lines of credit.

A home equity line of credit (HELOC) is a line of credit secured by your equity in your home, which is the difference between the value of your home and the amount you still owe on your mortgage. Since your home equity serves as collateral, if you default on a HELOC, you could risk losing your home to foreclosure.

A personal line of credit is usually unsecured, although sometimes you may be able to provide collateral in the form of savings or investments.

A business line of credit may be secured or unsecured. They are offered by financial institutions as well as many commercial vendors.

Examples of Installment Loans

An auto loan is one type of installment account.

Types of installment credit include:

Auto loans

Mortgages

Student loans

Personal loans Credit-builder loans

Home equity loans (not to be confused with a HELOC, which falls under revolving credit)

The breakdown of account types outlined above is a simplified version of how credit scoring systems actually categorize different types of accounts. In reality, credit scoring models may consider as many as 75+ account types.

In addition, each type of account could have a different effect on your credit.

How Does Credit Mix Affect Your FICO Score?

As we mentioned at the top of this article, credit mix makes up about 10% of your FICO score. With VantageScore, type of credit and credit age are combined into the same category, which makes up approximately 21% of your VantageScore.

With both types of scores, credit mix is a relatively small portion of what determines a credit score, so having the perfect credit mix is not necessarily essential in order to have good credit. However, it’s still a good thing to aim for, especially if you want to get a perfect 850 credit score or somewhere close to it.

What Is a Good Credit Mix?

When it comes to your credit score, the most important thing is to demonstrate that you have managed both revolving and installment accounts. Therefore, it’s best to have at least one type of account of each type.

FICO high score achievers have an average of seven credit cards on their credit reports. Photo by Hloom on Flickr.

For example, you might have a credit card (revolving) and an auto loan (installment). Or, you could have a mortgage (installment) and a HELOC (revolving). Any combination of one revolving account and one installment account is a good start for your credit mix.

FICO supports this idea, saying, “Having credit cards and installment loans with a good credit history will raise your FICO Scores.”

FICO also says that people who have managed credit cards responsibly are better off than consumers that don’t have any credit cards, who can be seen as risky because they have not demonstrated experience in using revolving credit.

Statistics show that high FICO score achievers have an average of seven credit cards on their credit reports, which includes both open and closed accounts.

People with credit scores in the 800s also typically have installment loans such as mortgages and auto loans, according to Experian.

The total number of accounts in your file may also play a role. FICO has indicated that those with high credit scores can have 20+ credit accounts in their credit reports.

How Many Credit Cards Is Too Many?

Having too many credit card accounts could hurt your credit score.

Keep in mind that it is possible to have too many accounts on your credit file. According to the FTC, having too many credit cards could have a negative effect on your credit score, as could having loans from some types of companies.

There is no hard-and-fast rule when it comes to how many credit cards is too many because the impact of any given factor on your credit score depends on what is already in your credit profile, says FICO.

However, in figure 1 in the article “How Credit Actions Impact FICO Scores,” the hypothetical consumer “Rachel,” who has 33 credit accounts, has a lower credit score than “Maria,” who has 21 accounts. This would seem to imply that at some number between 21 and 33 accounts, one’s credit score might begin to suffer. However, these two consumers have other differences in their credit profiles, so the difference in their credit scores cannot be solely attributed to the number of accounts in their files.

Can Some Account Types Hurt Your Credit?

Certain types of loans on your credit report could make you seem like a more risky consumer and therefore could end up hurting your score instead of helping.

Why? It’s all based on statistics and who the credit score algorithms have deemed to be risky borrowers.

For example, taking out a furniture loan could actually drop your credit score. That’s because furniture loans are often reported as “consumer finance loans,” which are typically reserved for borrowers with bad credit who are statistically more likely to default on loans. Therefore, having this type of account on your credit report could be viewed as risky by lenders and credit scoring algorithms.

Alternatively, the financing arrangement may be reported as revolving debt, which will appear nearly maxed out until you make enough payments to get the balance to a lower level.

Payday and title loans, however, are typically not reported to the credit bureaus, so these types of loans won’t count toward your credit mix or credit score—unless, of course, you default on a loan and it gets sold to a collection agency, who will then report it as a collection account.

Conclusions on Credit Mix

Since credit mix makes up about 10% of your credit score, it is helpful to try to achieve a balanced mix of credit by keeping a few revolving and installment accounts in good standing. The best credit mix should ideally include a few credit cards and at least one or two installment loans, such as mortgages or auto loans.

However, it’s also important to note that credit mix is much less important than other credit score factors, such as payment history, credit utilization, and credit age. It’s probably not worth obsessing over because you won’t automatically get an excellent credit score just by having the perfect mix of accounts.

In addition, most people naturally accumulate different types of accounts over time, so it’s not necessarily the best idea to start opening new accounts left and right just to build up your credit mix. This strategy could result in lots of inquiries and new accounts bringing your score down in the short term, and having access to credit you don’t need could also encourage extra spending.

As with all credit-related decisions, it’s up to you to take your overall financial goals and priorities into account before taking action. You might decide that you don’t need to worry too much about improving your credit mix, and that’s fine. On the other hand, improving your credit mix can only help your credit score, and it is something that you should pay attention to if you want to get a perfect 850 credit score.

While the credit system is definitely complicated, buying tradelines doesn’t have to be. Just keep a few basic principles in mind and follow these five steps to make buying tradelines easy!

Here are the five easy steps that we’ll break down in this article:

Understand your credit profile

Determine your goals

Choose tradelines that fit your credit profile and align with your goals

Order your tradelines

Wait for your tradelines to post!

1. Understand your credit profile

Understanding your credit file is the foundation of improving your credit. If you don’t know what’s in your file and blindly move ahead with tradelines and/or credit repair, you could easily make a mistake that could hurt your credit more than it helps.

Your credit report shows a list of all of your tradelines, and how you manage these tradelines is reflected in your credit score.

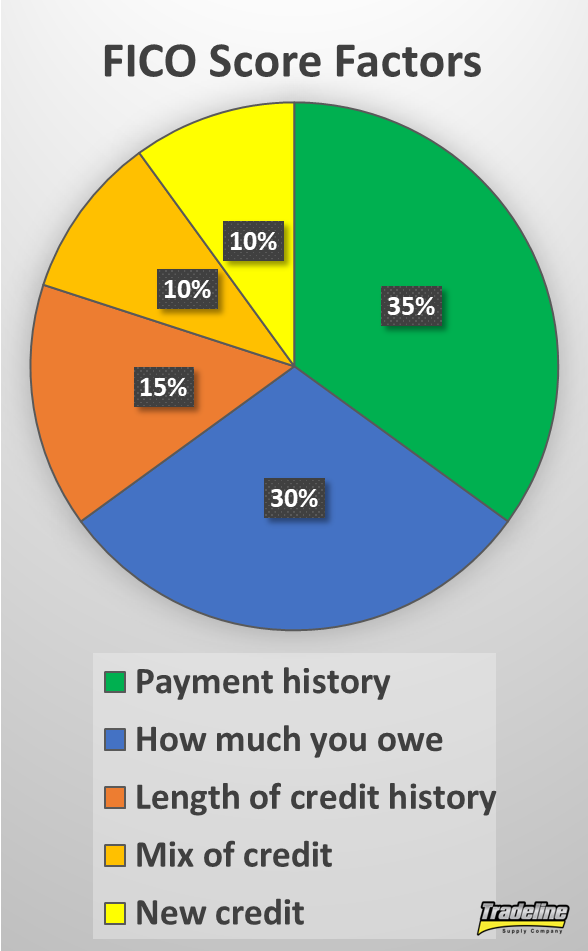

Payment history: 35%

Utilization (how much you owe): 30%

Length of credit history: 15%

Credit mix: 10%

New credit: 10%

Before buying any tradelines, you’ll want to take a good look at your credit profile on CreditKarma.com (or order one of your three free credit reports allowed each year from annualcreditreport.com) and make sure everything is accurate and up to date.

You can get an overview of your credit profile for free on CreditKarma.com.

If there is inaccurate information in your credit profile, you may want to look into credit repair in addition to tradelines.

Examine each of your credit accounts and try to understand how it may be affecting your credit score, whether positively or negatively.

This foundational step will allow you to form a clear picture of your unique credit situation so you can choose the smartest path to move forward.

2. Determine your goals

Consider these five main factors that affect your credit score when setting your goals.

Now that you are aware of what is in your credit profile, ask yourself what variables could be improved and which strategies would be a good investment of your time, effort, and money.

For example, if you have a blemished payment history that is bringing down your score, you could balance that out by adding as much positive payment history as possible with a seasoned tradeline.

If your credit age is not old enough, you may want to increase the age of your oldest account and your average age of accounts by adding a tradeline with a lot of age.

Perhaps you have a thin file or your credit mix is unbalanced, and you just want to add more tradelines to your credit file.

These are just a few examples of common goals that people often have when they are looking to add tradelines to their credit report. Make sure your goals are personalized to your unique credit situation.

3. Choose tradelines that fit your credit profile and align with your goals

Choosing the correct tradeline tends to be the trickiest part of this process. However, there are really only two main variables that you need to consider when selecting tradelines: the age of the card and the credit limit.

The tricky part is that people often incorrectly assume that they should just get the highest credit limit. In reality, this approach could actually backfire and hurt your credit, because the age of the tradeline is much more important in the vast majority of cases.

However, the credit limit does still come into play if utilization is a factor you are concerned about.

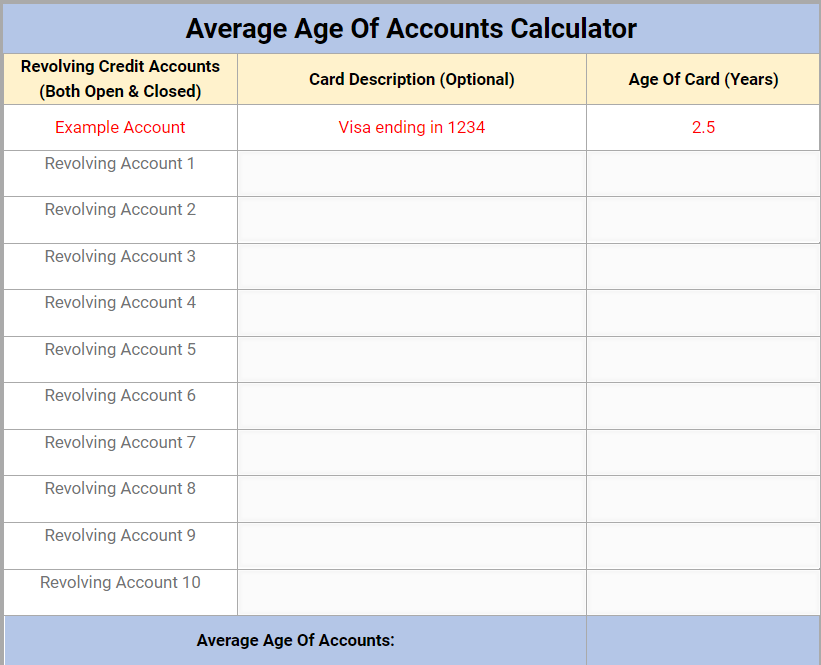

To account for both credit age and utilization, you’ll want to calculate your own average age of accounts and overall utilization ratio using our custom Tradeline Calculator. Simply input the numbers from your credit profile and the calculator will do the work for you.

Use our Tradeline Calculator to calculate your average age of accounts and utilization ratio.

Then, try plugging in information from some of the tradelines you are interested in purchasing and see how the numbers change. To get the maximum benefit from tradelines, you want to see the average age of accounts jump up at least to the next age level.

Based on our research, we estimate that the age levels to shoot for are 2 years, 5 years, 8 years, 10 years, and 20 years. So if your average age of accounts is 3 years, for example, it is probably a good idea to buy a tradeline that will boost that average to at least 5 years.

It’s important to fully think through your decision instead of just buying a tradeline that “seems” like a good choice.

Add tradelines to your cart and checkout on our secure site.

Once you have identified the best tradelines for you, simply add them to your cart and check out on our secure website!

To ensure that all goes smoothly with your purchase and that your tradelines post as guaranteed, you need to make sure you do not have any credit freezes or fraud alerts with any of the credit bureaus.

These actions block access to your credit report, so no new tradelines can be added. If you do have a credit freeze or fraud alert, contact each credit bureau to remove it before purchasing tradelines.

The last step is the easiest of all: sit back and wait for your tradelines to post! Once you receive your confirmation email, simply wait until the last day of each tradeline’s reporting period and then check to verify that the tradelines have posted.

Then, celebrate your new tradelines on social media! Don’t forget to tag us @tradelinesupply and use #tradelinesupply so we can find your post!

Share this image on social media and tag us when your tradelines post!

The banks and credit bureaus sometimes have errors in their reporting, so, unfortunately, there is a small chance that a non-posting could occur. However, if a tradeline does not post to at least any two out of the three credit bureaus, we will provide a refund or exchange for that tradeline. Simply follow the instructions detailed in “Report a Non-Posting” to submit your refund request.

6. Extra credit: Become a tradeline expert using the resources in our Knowledge Center!

The more you learn about tradelines, the more informed you will be when it’s time to buy. Those who are educated on the credit system and how tradelines work are in the best position to maximize their results from tradelines.

Check out our extensive library of tradeline resources in our Knowledge Center to become a tradeline expert and a highly informed buyer.

What is credit piggybacking? If you’re not sure what this strange term could possibly mean, you’re definitely not alone.

Credit piggybacking, also referred to as credit card piggybacking or piggybacking credit, is a commonly used credit-building strategy. However, many people are still unaware of how to access this strategy and use it to their advantage.

In this article, we’ll define what piggybacking for credit means and how it can help your credit.

Credit Piggybacking Definition

The general definition of credit piggybacking is building credit by becoming associated with a credit account owned by someone else. There are three main ways in which credit piggybacking can take place, which we discuss in more detail in “The Fastest Ways to Build Credit”:

Opening an account with a cosigner or guarantor is one way to piggyback on someone’s good credit.

Opening an account with a cosigner or guarantor, which is someone who promises to be responsible for the debt if the primary borrower cannot repay it. If the cosigner or guarantor has good credit, the borrower may be able to qualify for credit that they could not qualify for on their own or qualify for better terms.

Opening a joint account with another person, which means both parties have full access to the account and are both held fully responsible for the account. By opening a joint account with a partner who has good credit, a person with less-than-ideal credit may be able to open an account that they wouldn’t have qualified for on their own or get more favorable terms.

Becoming an authorized user for the purpose of credit card piggybacking, meaning you are not responsible for the debt, but the entire history of that account may be reflected in your credit file, regardless of when you were added.

When people talk about piggybacking credit, they are usually referring to authorized user piggybacking.

How Does Authorized User Piggybacking Work?

Here’s how piggybacking works as an authorized user:

When you are added as an authorized user to someone’s credit card, often (depending on the bank), the full history of that account will then be shown in your credit report, regardless of when you were added to the card.

Therefore, piggybacking can almost instantly add years of perfect payment history to the authorized user’s credit file.

Authorized user tradelines can affect many important credit variables, such as your average age of accounts, age of oldest account, overall utilization ratio, number of accounts, mix of accounts, and more.

Historically, only the wealthy and privileged were able to use piggybacking as a credit-building strategy. Now, there is a marketplace where tradelines can be bought and sold, which is helping to democratize the credit system and provide equal credit opportunity.

The issue of piggybacking went all the way to Congress, which upheld consumers’ rights to use authorized user tradelines.

Is Piggybacking Credit Legal?

While Tradeline Supply Company, LLC does not provide legal advice, we can provide evidence that supports the idea that piggybacking credit is legal.

Firstly, piggybacking for credit is an extremely common practice that has been in use since the advent of credit cards. Studies estimate that 20-30% of Americans that have credit records have authorized user accounts in their credit file.

In addition, about 25% of people who have credit reports initially established their credit files by piggybacking in one way or another.

Many banks actually encourage consumers to add authorized users for the express purpose of boosting their credit scores.

You may have heard about FICO trying to take away authorized user privileges in 2008. But what you probably didn’t hear about was FICO backing down after a congressional hearing that involved the Federal Trade Commission and Federal Reserve Board.

During the hearing, FICO admitted that they could not legally discriminate between spousal AUs and other users, because this would unlawfully violate the Equal Credit Opportunity Act.

Since the U.S. Congress has upheld consumers’ rights to use authorized user tradelines, it seems reasonable to conclude that authorized user tradelines are legal.

As we discussed in “Do Tradelines Still Work in 2019?”, credit piggybacking still works, and we think it will be around for a long time.

Piggybacking credit is a well-established credit-building strategy that has been defended in Congress and promoted by banks. It is a significant part of our credit system.

Thanks to the Equal Opportunity Credit Act, authorized user tradelines are still a very important factor in credit scoring models.

Not only that, but even if FICO were to devise an algorithm intended to exclude piggybackers, it would be quite some time before lenders could implement it on a large scale. The slow-moving financial industry is still using FICO scores that were developed decades ago.

Piggybacking companies bring together buyers and sellers of authorized user tradelines.

What Do Piggybacking Companies Do?

Piggybacking companies, more commonly referred to as tradeline companies, simply facilitate the buying and selling of authorized user tradelines.

The tradeline companies act as an intermediary by marketing the tradelines, protecting the identities of the clients, and preventing fraud.

At Tradeline Supply Company, LLC, we provide an innovative platform through which users can buy and sell tradelines entirely online. We also provide educational resources so consumers can familiarize themselves with the credit system and how piggybacking works.

Can Piggybacking Hurt Credit?

If credit piggybacking is done incorrectly, it can backfire and hurt your credit.

Because the full history of the credit account is reflected in the credit file of the piggybacker, that means any negative factors will show up, too.

For example, if the account has any late or missed payments, that could hurt the authorized user rather than help. Similarly, high utilization on the account could also damage the authorized user’s credit.

That’s why we recommend going with a reputable piggybacking company who guarantees perfect payment history and low utilization (15% or lower) on all tradelines. This will virtually eliminate the risk of your credit being hurt by these factors.

The only other way piggybacking could hurt your credit is if you choose the wrong piggybacking credit card. It’s essential to choose the right tradelines for your credit file. To do this, you’ll need to figure out your average age of accounts and how adding a tradeline could affect this statistic.

For example, if your average age of accounts is 5 years and you decide to piggyback on a 2-year-old tradeline, this would bring down your average age of accounts, which isn’t a good thing.

In credit reporting, negative information can only stay on your credit report for a maximum of 10 years for a Chapter 7 bankruptcy and seven years for everything else—right?

In credit reporting, negative information can only stay on your credit report for a maximum of 10 years for a Chapter 7 bankruptcy and seven years for everything else—right?