Your credit score is a seemingly simple three-digit number, but it can have a major impact on your finances. Without a high score, you may not be able to pursue some of your major financial goals. Or even if you can, those goals can actually turn into major challenges if you’re stuck with high interest rates because you had a low score. If you are preparing to improve your credit, you need to know the general ranges for scores so that you can set a specific goal for yourself. There are various tiers of credit scores, and being in a higher tier will generally bring the reward of better terms.

First, What’s the Average?

We’re going to talk about credit score categories in a moment, such as “poor,” “fair,” and “good.” But first let’s take a look at the average credit score. One initial point of clarification—while there are two major credit scoring models—FICO and VantageScore—we will focus primarily on the FICO score in this article, though we will make brief mention of the VantageScore as well. There are actually multiple FICO scoring models, and lenders use a variety of them, but the information here specifically relates to FICO® Score 8.

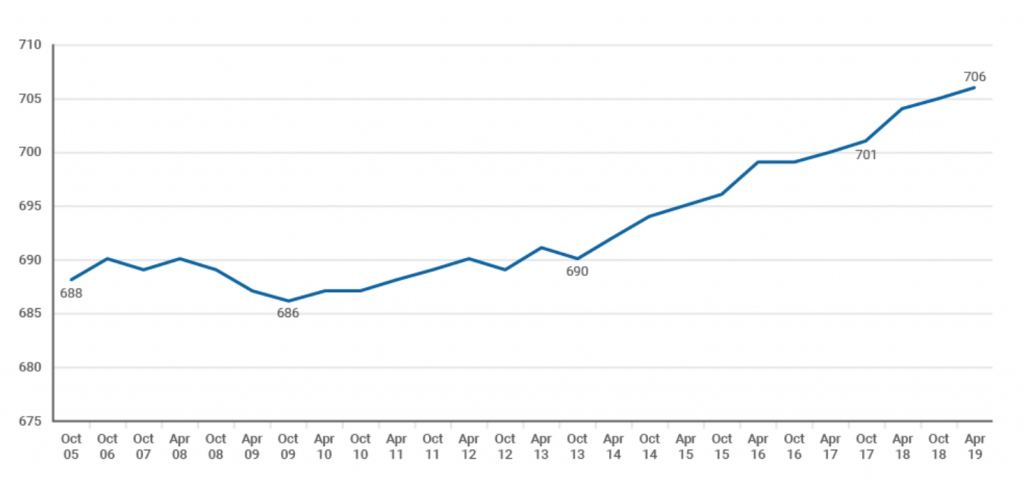

FICO most recently reported that the average credit score is 706. Credit scores nationwide can fluctuate significantly depending on the state of the economy. Back in 2009, the average was 686. COVID-19 and other economic factors may have a negative impact on the national average, but only time will tell. The average can be a useful baseline for comparing your own score. But, don’t let the average discourage you if your score is lower, because there are many ways to increase your score.

Source: FICO.com

The Breakdown

Using the FICO 8 scoring model, the credit bureaus agree (see Experian’s post here and Equifax’s here) to the following breakdown for score ranges. Again, remember that your lender may use a different model which could result in a slightly different breakdown. But, this should give you a good general idea of what to aim for.

Poor

A poor credit score is a score between 300 and 579.

Fair

A fair credit score is a score between 580 and 669.

Good

A good credit score is a score between 670 and 739.

Very Good

A very good credit score is a score between 740 and 799.

Excellent

An excellent credit score is a score between 800 and 850.

If you are curious about the breakdown for VantageScore 3.0, it looks like this:

Interestingly, the VantageScore ranges are narrower on the low end of the spectrum (including both a “very poor” and “poor” range, and broader on the high end (including only a “good” and “excellent,” without a “very good” range).

Why the Ranges Matter

Now that you know the ranges, here are three important reasons that they matter.

Access to Credit and Other Services

If your score is too low you may not have access to credit or, at the very least, you will likely have obstacles to credit. A score in the “very poor” range may mean that any applications for credit are denied. Your best bet may be a secured credit card, which requires you to make a deposit. While this is not ideal, a secured card can be an important tool in rebuilding your credit.

Also, remember that getting credit is not the only concern. Access to other products and services often depends, in part, on your credit history. Being in the “very poor” range can limit your ability to rent an apartment, enter certain contracts, or even get a job.

Favorable Credit Terms

Even if you can get credit, you will want the credit terms to be as favorable as possible. Bad credit terms, like high interest rates, will make your debt more expensive. They will also limit your purchasing power, which can prevent you from buying the home or car you want. Every time your score improves from one category to the next (say from “fair” to “good”), that should be paired with lenders offering you more favorable terms.

Here is a look at estimated mortgage rates by credit score and a look at auto loan rates by credit score. Note: these tools use different ranges and terminology for scores (for instance, the auto loan chart has ranges from “deep subprime” to “super prime”), but the general point still applies.

Goal Setting

Knowing the general credit score ranges can help you plan your goals for the future. Make a plan to check your credit score frequently, but especially as you make major changes (paying off a debt, opening a new card or loan, or changing your credit limit). You will also need to check your credit report often, as that report is the basis for your score. Keeping a close eye on these will help ensure that you move your credit in the right direction.

Want a free credit report review? An NFCC-certified counselor can review your credit report with you, and help you make a game plan for improving your financial standing. Learn more about the free credit report review, or get started here.

People who are serious about improving their credit often wonder what it takes to get the highest possible credit score. For the FICO 8 credit scoring model, the perfect credit score is 850.

As of April 2019, only about 1.6% of scorable consumers in the United States have the elusive 850 credit score, which is actually an increase from 0.98% in April 2014 and 0.85% in April 2009.

There are many other credit scoring models that are used for different purposes and may have different credit scoring ranges. However, since FICO 8 is the most commonly used credit score, we will use the number 850 as the benchmark for the ideal credit score.

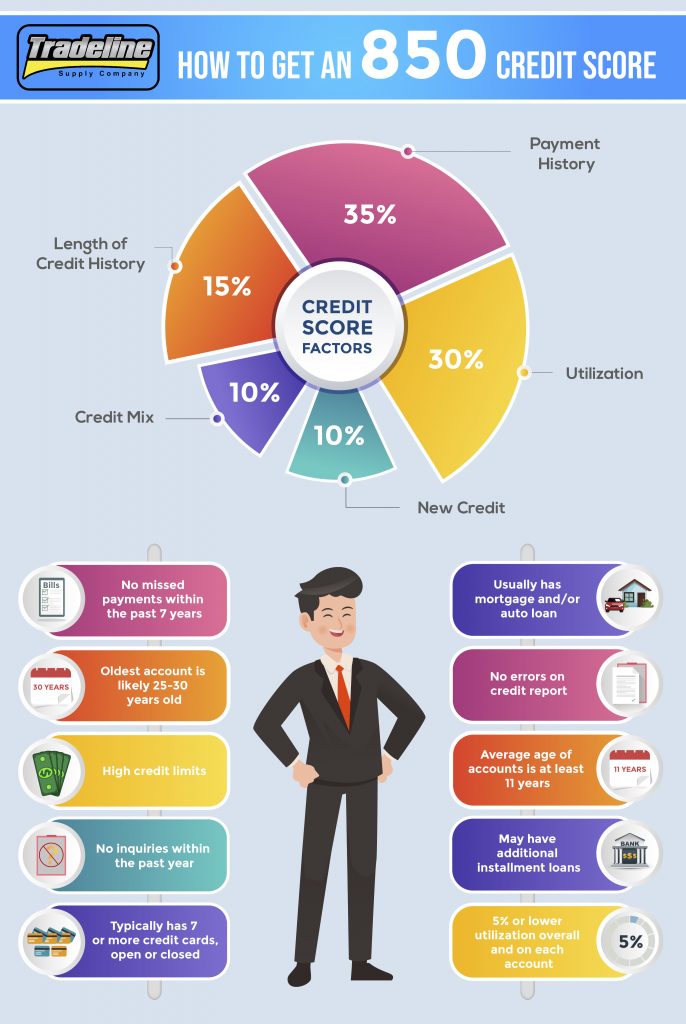

Check out the infographic below for some fast facts on how to get the highest credit score possible, then keep reading the article for even more tips on getting the coveted 850 credit score.

Payment History — 35%

Most people who have an 850 credit score have seven years of perfect payment history.

Your payment history is the biggest slice of the credit score pie, so even one late payment or missed payment can significantly affect your score. Negative items can stay on your credit report for up to seven years, so if you miss a payment, you may not be able to achieve a perfect 850 credit score until at least seven years have passed!

To safeguard against the possibility of forgetting to make a payment, consider setting up automatic bill pay for all of your accounts. Be sure to continue to check your accounts regularly in case of any system errors.

If you do miss a deadline once in a blue moon but have otherwise been an upstanding customer, try negotiating with your creditor to see if they will forgive the late payment and wipe it from your record.

FICO says that 96% of “high achievers,” or those with FICO scores above 785, have no missed payments on their credit report.

Essentially, to get an 850 credit score, you just need to follow one simple strategy: make all of your payments on time for a long time. We will further discuss the connection between payment history and time in the “Length of Credit History” section below.

Credit Utilization/How Much You Owe — 30%

The amount of debt you owe compared to your total credit limit is your credit utilization ratio. To get a perfect credit score, you’ll want to keep this ratio as low as possible, both overall and on each of your individual tradelines.

A study by VantageScore and MagnifyMoney found that people with the best credit scores and people with the worst credit scores actually had similar amounts of outstanding debt. However, those with the best scores had an average total credit limit of $46,700—16 times the credit limit of those with the worst scores!

Therefore, for the high scorers, that outstanding debt made up a much smaller percentage of their total available credit than those with low credit limits and poor scores, which highlights the importance of the overall utilization ratio.

This study reported that the average credit card user has an overall utilization ratio of 20%, which is generally considered to be a safe number for maintaining decent credit. To become someone who has an 850 credit score, however, you’ll need to keep it around 5% or lower. As of 2019, FICO says that the average revolving utilization for those with the “850 profile” is 4.1%.

While consumers with 850 credit scores do use credit cards, they tend to keep their utilization ratios around 5% or lower. Photo by Ellen Johnson.

In addition, keep in mind that even if you have a low overall utilization ratio, individual cards with high utilization could still bring down your score. You can read more about this in our article on individual vs. overall credit utilization ratios.

As a hypothetical example, let’s say you have two cards: one with a $10,000 limit and a $0 balance and the other with a $1,000 limit and a $900 balance. Your total available credit is $10,000 + $1,000 = $11,000 and your total debt is $900. Therefore, your overall utilization ratio is $900 / $11,000 = 8% utilization, which is a very good number.

However, your account with the $1,000 limit has a 90% individual utilization ratio! Since you only have two accounts, that means 50% of your accounts have high utilization, and that could negatively affect your credit. According to creditcards.com, maxing out just one credit card can reduce your score by as many as 45 points.

To get around this problem, if you have any individual cards with high utilization, consider transferring the balance to other accounts to keep the utilization ratio on each account as low as possible.

You could also request credit line increases from your creditors, which can lower your utilization ratios and benefit your score. Try using the tips we provide in “How to Increase Your Credit Limit.”

Another way to help with overall utilization is to add low-utilization tradelines to your credit file.

Optimizing this factor also means not closing old accounts even if you don’t use them very often, because their credit limits could be helping your score. To ensure old accounts don’t get automatically closed by the banks for inactivity, try to use them every 1-2 months, perhaps for small, recurring bills.

Length of Credit History (Age) — 15%

This category takes into account age-related factors such as the average age of your accounts, the age of your oldest account, and the ratio of seasoned to non-seasoned tradelines. (A seasoned tradeline is an account that is at least two years old, which is when the account is believed to have a more positive impact on your credit.)

Age goes hand-in-hand with payment history, because the more age an account has, the more time it has had to build up a positive or negative payment history. Together, age (15%) and payment history (35%) make up 50% of your credit score, which shows how important it is to open accounts early and make every single payment on time.

According to FICO, the age of the oldest account of people who have 650 credit scores is only 12 years, compared to 25 years for people who have credit scores above 800. In addition, individuals with fair credit have an average age of accounts of 7 years, compared to 11 years for those with excellent credit.

Cultivating an 850 credit score takes years of maintaining a positive credit history.

FICO reports that the average age of the oldest account of consumers who have 850 credit scores is 30 years old.

We have an in-depth discussion of which age tiers are most significant in our article, “Why Age Is the Most Valuable Factor of a Tradeline,” but the bottom line for getting the best credit score is simply to get as much age as possible. Seasoned tradelines can help by extending the age of the oldest account and the average age of accounts.

Also, keep in mind that it may be impossible to achieve an 850 credit score without a certain amount of age, even if you do everything else perfectly. So if you have stellar credit habits but haven’t yet been able to join the 850 credit club, you may just need to wait patiently for your accounts to age.

Credit Mix — 10%

While the mix of credit is one of the least important factors in a credit score, to get a perfect credit score of 850, you will still need to consider this factor.

In this category, credit scores reward having a balanced mix of several different accounts, including both revolving credit and installment loans. This is because creditors want to see that you can successfully manage a variety of different types of credit.

As an example, a credit file that includes an auto loan, a mortgage, and two credit cards has a better credit mix than a credit file that has four accounts that are all credit cards.

About the “credit mix” credit score factor, FICO says, “Having credit cards and installment loans with a good credit history will raise your FICO Scores. People with no credit cards tend to be viewed as a higher risk than people who have managed credit cards responsibly.”

The total number of accounts is also considered, with more accounts generally being better, up to a certain point.

FICO also states that high score achievers have an average of seven credit card accounts in their credit files, whether open or closed.

Auto loans are common among people who have 850 credit scores.

If you are looking to improve your credit mix statistics, adding authorized user tradelines can increase the total number of accounts and help diversify one’s credit file.

850 scorers also have installment loans in their credit files. According to Experian, the average mortgage debt for consumers with exceptional credit scores (800 or above) is $208,617. In addition, people who have FICO scores of 850 have an average auto-loan debt of $17,030.

Experian says, “In every other debt category except mortgage and personal loan, people with perfect scores had more open tradelines but less debt than their counterparts with average scores—underscoring the value of being able to manage debt while having numerous credit accounts.”

The “new credit” category of your credit score refers to how frequently you shop for new credit. This includes opening up new credit cards and applying for loans, for example. This “new credit” activity is reflected in the number of inquiries on your credit report.

Since seeking new credit makes you look like a higher risk to creditors, each hard inquiry has the potential to drop your score by a few points. Therefore, if you are going for a perfect 850, it’s best to avoid applying for new credit for a while.

However, it is possible to score an 850 with hard inquiries on your record. FICO recently stated that around 10% of 850 scorers had one or more inquiries within the past year, and about 25% had opened at least one new credit account within the past year.

If you need to shop for an auto loan or mortgage, be sure to complete all your applications within a two-week window in order for all of the credit pulls to count as one inquiry. For credit cards, however, each inquiry will be typically be counted individually.

Fortunately, inquiries only remain on your credit report for two years, and FICO scores only consider inquiries that occurred within the past year, so it shouldn’t take long for your credit to recover if you do have new inquiries on your credit report.

Inquiries aren’t the only thing that matters when it comes to the new credit factor of your credit score, however. It also includes data points such as the number of new accounts you have, the ratio of new accounts vs. seasoned accounts, and the amount of time that has passed since opening new accounts. The main idea if you want to maximize your credit score is to not open too many new accounts at once, which can make you look riskier to lenders and bring down your score.

More Tips on How to Get an 850 Credit Score

In addition to optimizing each of the above five categories that factor into your credit score, it is also important to regularly check for errors on your credit report and dispute any inaccurate information both with the credit bureaus as well as with the lenders who furnish the data to the bureaus.

In addition, those with very high credit scores rarely have serious delinquencies or public records on their credit reports, such as bankruptcies or liens. Obviously, this will be easy to avoid if you follow all of the suggestions above, but if you have a history of bad credit in your past, it could take up to 7-10 years to recover enough to get an 850 credit score.

850 Credit Score Benefits

What are the benefits of being in the 850 credit club? In reality, you’ll be able to take advantage of the benefits of having an excellent credit score whether you have a 760 credit score or an 850 credit score. You don’t need to score a perfect 850 to get the best credit cards or the best interest rates on loans.

Essentially, the main benefit of having the best possible credit score is bragging rights!

Final Thoughts on How to Get the Perfect Credit Score

While it’s probably not necessary to get an 850 credit score, it is smart to work toward the goal of having excellent credit by managing your credit wisely, which will eventually get you into the upper levels of high credit score achievers.

The most important factors of your credit score are payment history, utilization, and age. Therefore, to keep your credit in pristine condition, you’ll need to make all of your payments on time, keep your utilization as low as possible, and maximize your credit age. Beyond that, you’ll also want to maintain a balanced mix of accounts and minimize new credit inquiries.

Finally, take advantage of your three annual free credit reports to make sure your credit reports are free of damaging errors.

To summarize, here’s an example of what the credit profile of someone who has an 850 credit score might look like, as we illustrated in the infographic above:

No missed payments or delinquencies within the past seven years

A high total credit limit

The overall utilization ratio is 5% or lower

Individual credit cards each have low utilization, around 5% or lower

The oldest account is likely about 25-30 years old

The average age of accounts is at least 11 years

Typically has at least seven credit card accounts (whether open or closed)

Usually has an auto loan and/or a mortgage loan

May have additional installment loans

Minimal inquiries within the past year

No damaging errors on their credit report

Have you ever achieved the perfect 850 credit score? Is it a goal that you are currently working toward? Share your thoughts with us by leaving a comment below!

People who are serious about improving their credit often wonder what it takes to get the highest possible credit score. For the FICO 8 credit scoring model, the perfect credit score is an 850. Only 1.2% of consumers have the elusive 850 credit score.

There are many other credit scoring models that are used for different purposes and may have different credit scoring ranges. However, since FICO 8 is the most commonly used credit score, we will use 850 as the benchmark for the ideal credit score.

Keep reading for our tips and tricks for getting the highest credit score possible: the coveted 850 credit score.

Payment History — 35%

Most people who have an 850 credit score have seven years of perfect payment history.

Your payment history is the biggest slice of the credit score pie, so even one late payment or missed payment can significantly affect your score. Negative items can stay on your credit report for up to seven years, so if you miss a payment, you may not be able to achieve a perfect 850 credit score until at least seven years have passed!

To safeguard against the possibility of forgetting to make a payment, consider setting up automatic bill pay for all of your accounts. Be sure to continue to check your accounts regularly in case of any system errors.

If you do miss a deadline once in a blue moon but have otherwise been an upstanding customer, try negotiating with your creditor to see if they will forgive the late payment and wipe it from your record.

FICO says that 96% of “high achievers,” or those with FICO scores above 785, have no missed payments on their credit report.

Essentially, to get an 850 credit score, you just need to follow one simple strategy: make all of your payments on time for a long time. We will further discuss the connection between payment history and time in the “Length of Credit History” section below.

Credit Utilization/How Much You Owe — 30%

The amount of debt you owe compared to your total credit limit is your credit utilization ratio. To get a perfect credit score, you’ll want to keep this ratio as low as possible, both overall and on each of your individual tradelines.

According to Experian, “Among consumers with FICO credit scores of 850, the average utilization rate is 5.8%.”

A study by VantageScore and MagnifyMoney found that people with the best credit scores and people with the worst credit scores actually had similar amounts of outstanding debt. However, those with the best scores had an average total credit limit of $46,700—16 times the credit limit of those with the worst scores!

Therefore, for the high scorers, that outstanding debt made up a much smaller percentage of their total available credit than those with low credit limits and poor scores, which highlights the importance of the overall utilization ratio.

This study reported that the average credit card user has an overall utilization ratio of 20%, which is generally considered to be a safe number for maintaining decent credit. To become someone who has an 850 credit score, however, you’ll need to keep it around 5% or lower.

While consumers with 850 credit scores do use credit cards, they tend to keep their utilization ratios around 5% or lower. Photo by Ellen Johnson.

In addition, keep in mind that even if you have a low overall utilization ratio, individual cards with high utilization could still bring down your score.

As a hypothetical example, let’s say you have two cards: one with a $10,000 limit and a $0 balance and the other with a $1,000 limit and a $900 balance. Your total available credit is $10,000 + $1,000 = $11,000 and your total debt is $900. Therefore, your overall utilization ratio is $900 / $11,000 = 8% utilization, which is a very good number.

However, your account with the $1,000 limit has a 90% individual utilization ratio! Since you only have two accounts, that means 50% of your accounts have high utilization, and that could negatively affect your credit. According to creditcards.com, maxing out just one credit card can reduce your score by as many as 45 points.

To get around this problem, if you have any individual cards with high utilization, consider transferring the balance to other accounts to keep the utilization ratio on each account as low as possible.

You could also request credit line increases from your creditors, which could lower your utilization ratios and benefit your score.

Another way to help with overall utilization is to add low-utilization tradelines to your credit file.

Length of Credit History (Age) — 15%

This category takes into account age-related factors such as the average age of your accounts, the age of your oldest account, and the ratio of seasoned to non-seasoned tradelines. (A seasoned tradeline is at least two years old, which is when the account is believed to have a more positive impact on your credit score.)

Age goes hand-in-hand with payment history, because the more age an account has, the more time it has had to build up a positive or negative payment history. Together, age (15%) and payment history (35%) make up 50% of your credit score, which shows how important it is to open accounts early and make every single payment on time.

According to FICO, the age of the oldest account of people who have 650 credit scores is only 12 years, compared to 25 years for people who have credit scores above 800. In addition, individuals with fair credit have an average age of accounts of 7 years, compared to 11 years for those with excellent credit.

Cultivating an 850 credit score takes years of maintaining a positive credit history.

CreditKarma reports that a 2011 study found the average length of credit history for consumers with 850 credit scores to be 30 years.

We have an in-depth discussion of which age tiers are most significant in our article, “Why Age Is the Most Valuable Factor of a Tradeline,” but the bottom line for getting the best credit score is simply to get as much age as possible. Seasoned tradelines can help by extending the age of the oldest account and the average age of accounts.

Maximizing this factor also means not closing old accounts, because their age could be helping your score. To ensure old, dormant accounts don’t get automatically closed by the banks for inactivity, try to use them at least few times a year.

Also, keep in mind that it may be impossible to achieve an 850 credit score without a certain amount of age, even if you do everything else perfectly. So if you have stellar credit habits but haven’t yet been able to join the 850 credit club, you may just need to wait patiently.

Credit Mix — 10%

While the mix of credit is one of the least important factors in a credit score, to get a perfect credit score of 850, you may still need to optimize this factor.

In this category, credit scores reward having a balanced mix of several different accounts, including both revolving credit and installment loans. This is because creditors want to see that you can successfully manage a variety of different types of credit.

As an example, a credit file that includes an auto loan, a mortgage, and two credit cards has a better credit mix than a credit file that has four accounts that are all credit cards.

About the “credit mix” credit score factor, FICO says, “Having credit cards and installment loans with a good credit history will raise your FICO Scores. People with no credit cards tend to be viewed as a higher risk than people who have managed credit cards responsibly.”

The total number of accounts is also considered, with more accounts generally being better, up to a certain point.

FICO also states that high score achievers have an average of seven credit card accounts in their credit files, whether open or closed.

Auto loans are common among people who have 850 credit scores.

If you are looking to improve your credit mix statistics, adding authorized user tradelines can increase the total number of accounts and help diversify one’s credit file.

850 scorers also have installment loans in their credit files. According to Experian, the average mortgage debt for consumers with exceptional credit scores (800 or above) is $208,617. In addition, people who have FICO scores of 850 have an average auto-loan debt of $17,030.

Experian says, “In every other debt category except mortgage and personal loan, people with perfect scores had more open tradelines but less debt than their counterparts with average scores—underscoring the value of being able to manage debt while having numerous credit accounts.”

New Credit — 10%

The “new credit” category of your credit score refers to how frequently you shop for new credit. This includes opening up new credit cards and applying for loans, for example. This “new credit” activity is reflected in the number of inquiries on your credit report.

Since seeking new credit makes you look like a higher risk to creditors, each hard inquiry has the potential to drop your score by a few points. Therefore, if you are going for the enviable 850, it’s best to avoid applying for new credit for a while.

If you need to shop for an auto loan or mortgage, be sure to complete all your applications within a two-week window in order for all of the credit pulls to count as one inquiry. For credit cards, however, each inquiry will be typically be counted individually.

Fortunately, inquiries only remain on your credit report for two years, and FICO scores only consider inquiries that occurred within the past year, so it shouldn’t take long for your credit to recover if you do have new credit inquiries on your report.

More Tips on How to Get an 850 Credit Score

In addition to optimizing each of the above five categories that factor into your credit score, it is also important to regularly check your credit reports and dispute inaccurate information.

In addition, those with very high credit scores rarely have serious delinquencies or public records on their credit reports, such as bankruptcies or liens. Obviously, this will be easy to avoid if you follow all of the suggestions above, but if you already have a messy credit history in your past, it could take up to 7-10 years to recover enough to get an 850 credit score.

850 Credit Score Benefits

What are the benefits of being in the 850 credit club? In reality, you’ll be able to take advantage of the benefits of having an excellent credit score whether you have a 760 credit score or an 850 credit score. You don’t need to score a perfect 850 to get the best credit cards or the best interest rates on loans.

That said, the main benefit of having the best possible credit score is bragging rights.

Final Thoughts on How to Get the Perfect Credit Score

While it’s probably not necessary to get an 850 credit score, it is smart to work toward that goal by managing your credit wisely, which will eventually get you into the upper levels of high credit score achievers.

The most important factors of your credit score are payment history, utilization, and age. Therefore, to keep your credit in pristine condition, you’ll need to make all of your payments on time, keep your utilization as low as possible, and maximize your credit age. Beyond that, you’ll also want to maintain a balanced mix of accounts and minimize new credit inquiries.

Finally, take advantage of your three annual free credit reports to make sure your credit reports are free of damaging errors.

To summarize, here’s an example of what the credit profile of someone who has an 850 credit score might look like:

No missed payments or delinquencies within the past seven years

A high total credit limit

The overall utilization ratio is 5% or lower

Individual credit cards each have low utilization, around 5% or lower

The oldest account is likely about 25-30 years old

The average age of accounts is at least 11 years

Typically has at least seven credit card accounts (whether open or closed)

Usually has an auto loan and/or a mortgage loan

May have additional installment loans

No inquiries within the past year

No damaging errors on their credit report

How many times have you read a blog or heard some financial “guru” opining as to the mystical “right” number of credit cards to have in your wallet? Is the right number one, or two, or three? And what is the criteria for considering what is the right number versus the wrong number?

I’ll let you in on a little secret, there is no right or wrong number. It’s just an excuse to write a blog. If you are comfortable with one credit card, then one is the right number for you. If you need four to operate efficiently, then four is your right number. If you hate credit cards, then maybe zero is your right number.

When considering the right or wrong number of credit cards, nobody ever seems to focus on credit scores as part of their consideration. Well, that’s exactly what I’m going to do. And the reason I’m going to do so is because from a credit scoring perspective there actually is a right number of credit cards.

The Revolving Utilization Ratio

There is a metric in credit scoring systems called revolving utilization. Revolving utilization, often referred to as the balance-to-limit ratio, is the relationship between your credit card balances and your credit card limits, expressed as a percentage.

The ratio is calculated by dividing the aggregate of your balances by the aggregate of your credit limits, thus yielding a percentage. The higher that percentage, the fewer credit score points you’re going to earn from that metric. The lower that percentage, the more points you’re going to earn.

Reports about the optimal percentage are all over the place, with many of them being wrong. For FICO the optimal percentage is actually 1%, which is next to impossible to pull off. So, we have to go to the average percentage for the people with the highest average FICO scores, those with 750 and above. For those folks the average utilization ratio is 7%. For VantageScore the optimal percentage is anything less than 30%.

Now, that doesn’t mean you have to have 7% or 30% in order to have solid credit scores. You’ll just need to hit those targets if you want the highest possible scores, something that’s infinitely important right before you apply for a loan.

Let’s go back to the topic of this blog, which is the right number of credit cards. The right number for you is going to be the number of cards necessary for you to maintain 7% utilization relative to your normal credit card spending patterns. That way you don’t really have to worry about your credit scores, ever. If you can hit 7%, or close to it, on a monthly basis then you’ll do as well as possible under both credit scoring platforms.

What you need to do now is download your credit card statements from the last 12 months. Add up the balances from all of the statements, and divide that number by 12. That will give you your average monthly amount of credit card debt appearing on your credit reports. Let’s say, for illustration purposes, your average monthly balance from all of your cards is $5,000.

Now we just need to figure out what credit limits you need from all of your cards in order for $5,000 to represent 7% of the aggregate credit limit. I’ll do the math for you…you’re going to need about $70,000 of credit limits for $5,000 to represent 7% of the limit because $5,000 divided by $70,000 equals 7.1%.

$70,000 sounds like a really large number, but in the world of credit card credit limits, it’s actually not that big of a number. In fact, if you have two credit cards each with limits of $35,000, you’re already there. For many of you, however, you’re going to need more than two cards.

This becomes the answer to your question about the right number of cards. If it takes six credit cards for your average monthly credit card balances to equal about 7%, then six cards is the right number for you. If it takes ten cards, or 13 cards, or three cards…then those are the right numbers for you.

John Ulzheimer is a nationally recognized expert on credit reporting, credit scoring and identity theft. He is the President of The Ulzheimer Group and the author of four books about consumer credit. Formerly of FICO, Equifax and Credit.com, John is the only recognized credit expert who actually comes from the credit industry. He has 27+ years of experience in the consumer credit industry, has served as a credit expert witness in more than 370 lawsuits, and has been qualified to testify in both Federal and State courts on the topic of consumer credit. John serves as a guest lecturer at The University of Georgia and Emory University’s School of Law.

Disclaimer: The views and opinions expressed in this article are those of the author John Ulzheimer and do not necessarily reflect the official policy or position of Tradeline Supply Company, LLC.

While the credit system is definitely complicated, buying tradelines doesn’t have to be. Just keep a few basic principles in mind and follow these five steps to make buying tradelines easy!

Here are the five easy steps that we’ll break down in this article:

Understand your credit profile

Determine your goals

Choose tradelines that fit your credit profile and align with your goals

Order your tradelines

Wait for your tradelines to post!

1. Understand your credit profile

Understanding your credit file is the foundation of improving your credit. If you don’t know what’s in your file and blindly move ahead with tradelines and/or credit repair, you could easily make a mistake that could hurt your credit more than it helps.

Your credit report shows a list of all of your tradelines, and how you manage these tradelines is reflected in your credit score.

Payment history: 35%

Utilization (how much you owe): 30%

Length of credit history: 15%

Credit mix: 10%

New credit: 10%

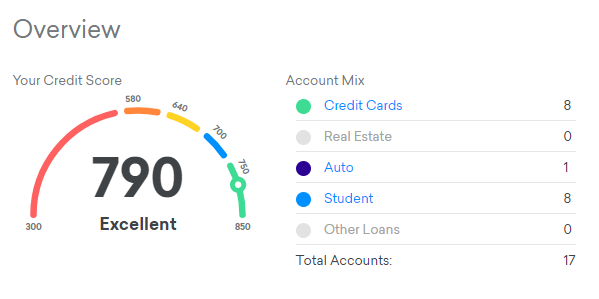

Before buying any tradelines, you’ll want to take a good look at your credit profile on CreditKarma.com (or order one of your three free credit reports allowed each year from annualcreditreport.com) and make sure everything is accurate and up to date.

You can get an overview of your credit profile for free on CreditKarma.com.

If there is inaccurate information in your credit profile, you may want to look into credit repair in addition to tradelines.

Examine each of your credit accounts and try to understand how it may be affecting your credit score, whether positively or negatively.

This foundational step will allow you to form a clear picture of your unique credit situation so you can choose the smartest path to move forward.

2. Determine your goals

Consider these five main factors that affect your credit score when setting your goals.

Now that you are aware of what is in your credit profile, ask yourself what variables could be improved and which strategies would be a good investment of your time, effort, and money.

For example, if you have a blemished payment history that is bringing down your score, you could balance that out by adding as much positive payment history as possible with a seasoned tradeline.

If your credit age is not old enough, you may want to increase the age of your oldest account and your average age of accounts by adding a tradeline with a lot of age.

Perhaps you have a thin file or your credit mix is unbalanced, and you just want to add more tradelines to your credit file.

These are just a few examples of common goals that people often have when they are looking to add tradelines to their credit report. Make sure your goals are personalized to your unique credit situation.

3. Choose tradelines that fit your credit profile and align with your goals

Choosing the correct tradeline tends to be the trickiest part of this process. However, there are really only two main variables that you need to consider when selecting tradelines: the age of the card and the credit limit.

The tricky part is that people often incorrectly assume that they should just get the highest credit limit. In reality, this approach could actually backfire and hurt your credit, because the age of the tradeline is much more important in the vast majority of cases.

However, the credit limit does still come into play if utilization is a factor you are concerned about.

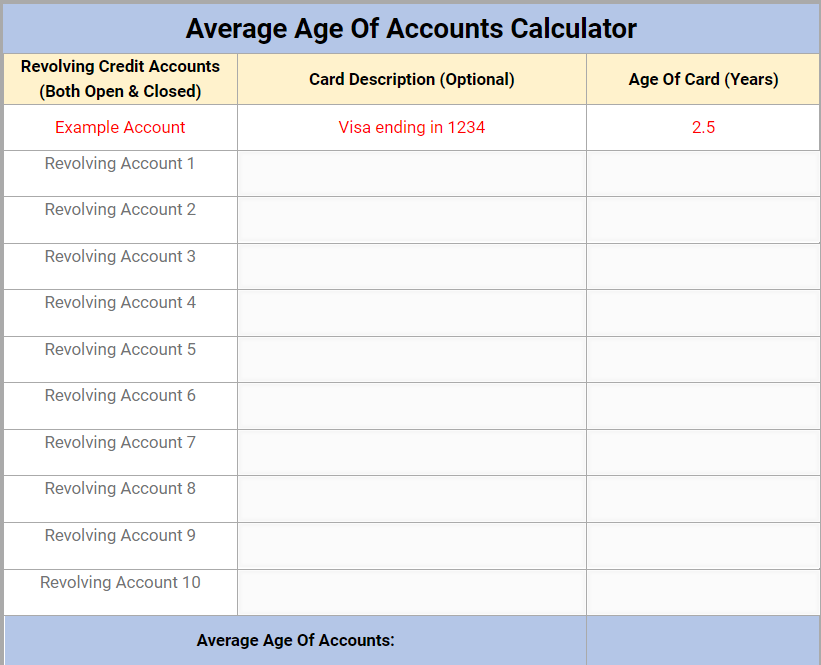

To account for both credit age and utilization, you’ll want to calculate your own average age of accounts and overall utilization ratio using our custom Tradeline Calculator. Simply input the numbers from your credit profile and the calculator will do the work for you.

Use our Tradeline Calculator to calculate your average age of accounts and utilization ratio.

Then, try plugging in information from some of the tradelines you are interested in purchasing and see how the numbers change. To get the maximum benefit from tradelines, you want to see the average age of accounts jump up at least to the next age level.

Based on our research, we estimate that the age levels to shoot for are 2 years, 5 years, 8 years, 10 years, and 20 years. So if your average age of accounts is 3 years, for example, it is probably a good idea to buy a tradeline that will boost that average to at least 5 years.

It’s important to fully think through your decision instead of just buying a tradeline that “seems” like a good choice.

Add tradelines to your cart and checkout on our secure site.

Once you have identified the best tradelines for you, simply add them to your cart and check out on our secure website!

To ensure that all goes smoothly with your purchase and that your tradelines post as guaranteed, you need to make sure you do not have any credit freezes or fraud alerts with any of the credit bureaus.

These actions block access to your credit report, so no new tradelines can be added. If you do have a credit freeze or fraud alert, contact each credit bureau to remove it before purchasing tradelines.

The last step is the easiest of all: sit back and wait for your tradelines to post! Once you receive your confirmation email, simply wait until the last day of each tradeline’s reporting period and then check to verify that the tradelines have posted.

Then, celebrate your new tradelines on social media! Don’t forget to tag us @tradelinesupply and use #tradelinesupply so we can find your post!

Share this image on social media and tag us when your tradelines post!

The banks and credit bureaus sometimes have errors in their reporting, so, unfortunately, there is a small chance that a non-posting could occur. However, if a tradeline does not post to at least any two out of the three credit bureaus, we will provide a refund or exchange for that tradeline. Simply follow the instructions detailed in “Report a Non-Posting” to submit your refund request.

6. Extra credit: Become a tradeline expert using the resources in our Knowledge Center!

The more you learn about tradelines, the more informed you will be when it’s time to buy. Those who are educated on the credit system and how tradelines work are in the best position to maximize their results from tradelines.

Check out our extensive library of tradeline resources in our Knowledge Center to become a tradeline expert and a highly informed buyer.

If you’re just starting out in the world of tradelines, we recommend taking a look at our Tradelines 101 infographic to get the basics down before moving on to deciding which tradelines to purchase. If you’re already familiar with the concept of tradelines and want to learn how to select the best tradelines for sale, then this buyer’s guide is for you.

When shopping to buy tradelines, there are basically only two main variables to consider:

(1) the age of the card, and

(2) the credit limit.

All the other variables should be about equal, which includes having a perfect payment history, low utilization (at or below 15%), the type of account (usually a revolving credit card), and the reporting date.

In most cases, if you buy from a reliable tradeline supplier, the name of the bank should not matter, except in instances where you may be blacklisted from that bank due to filing for bankruptcy or having unpaid collections with that bank.

So, with only two variables to consider, why is it so challenging to be able to choose the right tradelines? The answer is that most people’s credit files are fairly complex due to their depth of credit history. People have numerous data points in their credit file and all that data plays some sort of role in calculating their credit score.

Every person’s credit file is unique, making it very difficult to discuss how tradelines may affect anyone “on average.” Additionally, there are multiple different credit scores, each with their own closely guarded algorithm that takes into account a very large amount of data points within someone’s credit report.

When choosing the best tradelines for your situation, it’s not just about buying the top tradelines in terms of price. To get the results you want, you will need to understand what is already in your credit file and how adding tradelines could affect the important factors in your file.

Most people’s credit files contain a lot of complex information, which can make it difficult to predict how adding tradelines will affect one’s credit.

Credit Limits and Utilization Ratios

Let’s discuss each of these variables individually, starting with credit limits.

In most of the free credit score simulators out there, you can only change a very limited number of variables. So when it comes to trying to guess how a tradeline may affect your credit score, it usually only allows you to enter a new credit limit amount and then it generates a new credit score estimate.

The credit score simulator (sometimes referred to as a credit score calculator) assumes you are opening a new credit card with whatever limit you type in. Essentially, it is only looking at your overall utilization ratio, and not taking into account the age that you would gain from adding a seasoned tradeline.

As far as utilization, many professionals would suggest that you want to stay below 20% ideally. From our experience, we have seen that utilization ratios of 30% – 40% or higher start to pull credit scores down.

The higher the utilization ratio, the more your credit score will decrease, even if these accounts are always paid on time. Most credit specialists would recommend keeping your overall utilization ratio below 20% or even lower.

However, things get much more complicated in instances where someone has several credit cards with different utilization ratios.

Let’s say for example that someone has seven established credit cards, where two have zero balances, two are at 50% utilization, one is at 75%, and the last two are completely maxed out.

Sure, buying some tradelines with high limits might be able to get the overall utilization down to the targeted 20% level, but that does not eliminate the fact that that person still has five credit cards with high utilization, and each of these five cards is pulling down the credit score down due to high individual utilization.

Can a High-Limit Tradeline Help Lower Someone’s Overall Utilization Ratio?

In theory, a higher-limit tradeline can help lower someone’s overall utilization ratio, but this alone may not completely solve the problem of having credit cards with high utilization. Negative factors are always going to play a role in the credit score and having any high-utilization credit cards is a negative factor.

However, having a lower overall utilization ratio would be a positive change and may still yield some benefit despite the fact that the individual credit cards with high utilization will still remain in the equation.

We have even heard of metrics in the secret credit score algorithm that look at the percentage of high-utilization credit cards in someone’s credit file relative to the total number of credit cards they have.

For example, if someone has two credit cards, one with a $5,000 limit where they owe $5,000 on it and another credit card with a $25,000 limit where they owe zero on it, their overall utilization ratio is relatively low at 16.67% but they would be at 50% on the percentage of revolving accounts with high utilization. In this example, the 50% ratio of high utilization cards could possibly have a negative impact even though the overall utilization ratio is within the ideal range.

There may be other reasons why some people are interested in adding higher-limit tradelines to their credit file that have nothing to do with the typical goal of raising their credit score.

For example, some people believe that having higher-limit accounts in their credit file may increase their odds of getting approved for higher-limit credit cards or other types of loans. We do not have any knowledge about the validity of these beliefs, nor do we help people with funding in any way, but we are aware that such strategies exist in the marketplace.

This is an additional reason why some individuals might be interested in a high-limit tradeline even if there is not very much age on the account, which also makes the cost of a tradeline cheaper.

Examining the Age of a Tradeline

This leads us to the second variable to discuss, which is the age of the tradeline. We feel that age is the most important of the two factors of a tradeline. In general, a credit score is broken down into the following categories:

35% your payment history

30% how much you owe

15% length of credit history

10% credit mix

10% new credit

The utilization ratios fall under the “how much you owe” category, which accounts for about 30% of your score. Again, if you are only improving the overall utilization ratio but you are still being pulled down by individual card utilization ratios, then you may not be benefitting from the full 30% of the power of this category. Your benefit may be as little as 10-15% if you still have individual cards with high utilization ratios.

However, the tradelines we offer are going to have a perfect payment history, which is the category that can affect your score by as much as 35%. They also have the ability to affect the “length of credit history” category which accounts for another 15% of the score.

When added together, the payment history (35%) plus the length of credit history (15%) amounts to about 50% of a credit score. These two categories, which account for about 50% of a credit score, are both affected by the age of the tradelines.

“Seasoned” tradelines, or those that are at least two years old, are the most valuable type of tradeline.

In the age category, just like the utilization category, there are several different variables. To name a few, the credit score algorithm may look at your average age of accounts, the oldest account in your profile, the number or percentage of non-seasoned accounts (less than 2 years old) in your file as well as the number or percentage of seasoned accounts in your file.

Also, different scoring models may or may not include data on closed accounts and have varying degrees of how much weight they give to closed account information.

To illustrate an example, we have seen a credit report of a person who had over a 700 credit score with no open accounts at all. So 100% of that 700+ credit score was made up of data from closed accounts only.

We also know the opposite can be true, where someone has zero open accounts but several closed accounts with derogatory information and their credit score is very low, all from closed account data. So it is safe to say that closed accounts can still play a significant role in someone’s credit score since it is still part of their credit history.

One of the most important variables related to the length of credit history is the age of the oldest account in someone’s credit profile. This variable is very straightforward, except that it may be split into two categories: open accounts and closed accounts. It is assumed that open accounts usually weigh more than closed accounts and obviously, older accounts are better.

The most common age-related variable that most credit advisors will talk about is the average age of accounts. It is commonly believed that the average age of accounts may be the most powerful factor in the age category.

As we will see in the examples below, in working with tradelines, most people underestimate how difficult it is to significantly affect an average, especially when there are multiple accounts already in your credit history.

Calculating Your Average Age of Accounts

For illustration, here are a few hypothetical examples of how to calculate the average age of accounts and how new tradeline data gets factored in.

Example 1: Thin File for Simple Illustration

Card 1: 0.5 years old

Card 2: 0.5 years old

Card 3: 1.5 years old

The average age of accounts in this example is 0.83 years. The way you figure that out is to add up the total number of years and divide that by the total number of accounts. (0.5 + 0.5 + 1.5 = 2.5 years total, then divide by 3 = 0.83 years average.)

If your goal was to get the average age of accounts up to 2 years old by adding one tradeline, the new tradeline would have to be about 6 years old. (0.5 + 0.5 + 1.5 + 6 = 8.5 total years divided by 4 total accounts = 2.1 average age of accounts.)

Notice how much older the new tradeline had to be in order to simply get the average age of accounts to be 2 years old for a very thin file. Many people would not have guessed that they would need such an old card just to get the average to be 2 years old.

To illustrate this point, if someone were to only add a 4-year-old tradeline to this mix, the average age of accounts would then only be 1.6 years, and this is assuming a person only has 3 revolving accounts (opened or closed) in their credit file, which is very rare.

The more accounts a person has, the less impact a single tradeline will have due to the simple mathematics of calculating an average.

Example 2: Established Credit File With Multiple Open & Closed Accounts

The more accounts there are in your credit file, the more difficult it will be to affect the average age of accounts.

Card 1: 4 years old

Card 2: 8 years old

Card 3: 6 years old

Card 4: 4 years old

Card 5: 7 years old

Card 6: 7 years old (closed account)

Card 7: 15 years old (closed account)

Card 8: 13 years old (closed account)

Card 9: 9 years old (closed account)

Card 10: 12 years old (closed account)

The average age of accounts here is 8.5 years old. The way you calculate that is to add up the total number of years and divide that by the total number of accounts. (4 + 8 + 6 + 4 + 7 + 7 + 15 + 13 + 9 + 12 = 85 years, divided by 10 accounts = 8.5 years average age of accounts.)

Let’s say hypothetically that the person’s goal is to get their average age of accounts up to 10 years old by adding a single tradeline.

Please stop and take a moment to guess how many years old a new tradeline would need to be in order to make the average age of accounts 10 years in this example.

The Answer:

They would need to add a tradeline that is 25 years old in order to get the average age of accounts to be 10 years. (4 + 8 + 6 + 4 + 7 + 7 + 15 + 13 + 9 + 12 + 25 = 110 total years divided by 11 total accounts = 10 year average age of accounts.)

Notice how huge of a jump in years is needed in order to change someone’s average if they already have a lot of accounts in their credit file, even if some of them are closed accounts. Most people underestimate how difficult it is to really change an average and even most “professionals” (who are usually just commissioned salespeople) underestimate how these numbers actually work out.

Our tradeline calculator can help you figure out how buying tradelines could affect your credit.

Until you actually do the math yourself, do not just blindly trust what someone suggests for you. To easily calculate your own average age of accounts and utilization ratios and see how those variables change when you add seasoned tradelines, try our Tradeline Calculator.

A Common Mistake People Make When Buying Tradelines

It is easy to see how in the second example above, if this person did not do the math, they might purchase the wrong tradeline and be disappointed.

Let’s say they purchased a tradeline that is 18 years old with a $20,000 credit limit that cost $1,000. They might just assume that since it was an expensive tradeline with a lot of age and a high limit that it should “obviously” be super powerful and they should definitely see positive results.

However, in reality, the 18-year-old card would only increase the average age of accounts to 9.4 years, and it is very possible that increasing one’s average age of accounts from 8.5 years to 9.4 years may not have very much of an impact on their overall credit picture.

As you can imagine, this person could easily be very disappointed in their results for the reason that they simply did not do the math and were not aware of how to choose the best tradeline for their credit file.

As another example, what if this person were to choose to purchase a tradeline that is 7 years old with a $30,000 limit? On the surface, that might look like a decent tradeline to buy, but it would actually decrease their average age of accounts and consequently, it could even hurt their credit score, even though that tradeline might have a $750-$1,000 price tag.

We illustrate this to show that not knowing how tradelines work can actually hurt your credit and be a complete waste of money. For this reason, we believe education is the best service we can offer. Make sure to read our list of common mistakes made when buying tradelines to be aware of other pitfalls to avoid.

Although credit reports can be complex, it’s important to have a good understanding of your file before choosing which tradelines to buy. Image by Jack Moreh.

Conclusions on Choosing the Best Authorized User Tradelines

Authorized user tradelines can be very effective for many people, assuming that they added superior tradelines to what they already have in their credit file. On the other hand, since many people are not educated about how the system works, it can be easy for people to choose the wrong tradelines that do not help them very much.

Compounding the confusion, it is very difficult to find the best tradeline company to work with. We believe that educating our customers is the best thing that we can do for our community and offering affordable tradelines makes them more accessible to the people who need them most.

Use our Tradeline Calculator to help you understand the key factors relating to the tradelines in your credit file and to help point you in the right direction for your next tradeline. For even more educational resources on tradelines, visit our blog.

Tradelines are simple. There are only two main variables: Age and limit. Of course, price and posting dates are also important, but let’s set that aside for the moment.

If you want to see good results, you have to focus on age. Age makes up 50% of the credit score because 35% is payment history and 15% is the actual age. However, it is impossible to separate the age from the payment history or the payment history from the age, so in reality, these two categories are combined to form 50% of the credit score.

The other variable of a tradeline is the credit limit. The limit can affect the overall utilization ratio and possibly some other variables in the secret credit score algorithms, but mainly the overall utilization ratio. Since the amounts owed make up approximately 30% of the credit score, people tend to think that the limit of the tradeline is more important, but if you believe this, you are misinformed and you will not get the results you hope for.

Here’s the reason why the limit of a new tradeline does not help as much as people hope: if someone is trying to lower their overall utilization ratio, then that means they currently have high utilization on some of their credit cards.

If someone is carrying a lot of revolving debt, a high-limit tradeline may not provide the results they would hope for.

For example, if someone has several cards that are maxed out, it may seem to make more sense to lower their overall utilization ratio by buying a high limit tradeline as opposed to paying down their cards. However, if they do this, they still have the same amount of cards that are maxed out, and that alone is a very powerful negative factor.

Adding one or two high limit cards does not change the fact that the person still has several maxed out cards, which, as we all know, lowers a credit score. Changing the overall utilization ratio has been shown to be a relatively weak variable when individual high-utilization cards are present. Individual high-utilization cards tend to outweigh the overall utilization ratio.

To illustrate another example, let’s look at it from the opposite perspective of someone starting with a high credit score and a large amount of available credit who sees their score drop after maxing out their cards. (This is a hypothetical example with made-up numbers just to illustrate the point.)

Hypothetical scenario:

780 credit score

10 credit cards with perfect payment history, each with a $10,000 credit limit ($100,000 in available credit)

The number of individual cards with high utilization tends to outweigh the overall utilization ratio. Photo by Ellen Johnson.

If this person maxes out one card, they only have a 10% overall utilization ratio, but their score might drop to 710.

If this person maxes out a second card, they only have a 20% overall utilization ratio, but their score might drop to 660.

If this person maxes out a third card, they only have a 30% overall utilization ratio, but their score might drop to 640.

Now, if this person were to add a tradeline with a $50,000 limit, the overall utilization ratio may drop back down to 20%, but they may not see any improvement to their score at all, which has to do with the fact that they have three maxed-out credit cards.

The take-home message is this: if someone has high utilization on multiple credit cards, changing the overall utilization ratio alone is not going to solve that problem, and they may not see a significant benefit.

How a Seasoned Tradeline Can Help

The secret to using tradelines effectively is buying “seasoned” tradelines, which are tradelines that have significant age (generally at least two years). We estimate that as much as 90% of the power of a tradeline has to do with its age. However, just looking at the age of an individual tradeline alone is also not the correct way to shop for a tradeline.

The power of a tradeline will always be relative to what is already in someone’s credit report.

Therefore, the most effective way to choose a tradeline is to look at how the new tradeline will affect a person’s average age of accounts.

This is the secret key to unlocking the power of a tradeline. This factor alone is the most significant aspect of how tradelines work.

We have identified several possible age tiers of special significance, especially with respect to one’s average age of accounts. These special age tiers are:

2 Years

5 Years

8 Years

10 Years

20 Years

Therefore, if someone has an average age of accounts of 1.5 years, then the next target would be to pass the 2-year mark with their average age of accounts. Similarly, if someone has an average age of accounts of 3 years, the next target would be to get their average age of accounts past 5 years, and so on.

Often people make the mistake of only looking at the age of a tradeline by itself and not taking into account how the tradeline will affect their average age of accounts.

For example, if someone determines that their average age of accounts is 5 years, they might conclude that any tradeline over 5 years old is what they need, so they might choose a tradeline that is 7 years old.

However, by only adding a 7-year-old tradeline, they would have only increased their average age of accounts from 5 years to 5.2 years, which obviously is not a significant change and certainly does not get their average age of accounts up to the next age tier.

To make this easy, we have created a Tradeline Calculator, which helps you quickly calculate your average age of accounts, and demonstrates how a new tradeline may affect this powerful variable.

Using our Tradeline Calculator to determine your average age of accounts will help guide you in choosing the best tradelines for your particular situation.