Revolving accounts and installment accounts are both important account types when building credit, but they are not equally powerful when it comes to your credit score. Which type of account has a greater impact on your credit score? Keep reading to find out.

Revolving Debt vs. Installment Debt: Definitions

Revolving Credit Account Definition

A revolving credit account is an account that allows you to “revolve” a balance, which means you do not have to pay the full outstanding balance on the account every month.

Revolving accounts typically have a credit limit up to which you can charge up to. You can choose how much to borrow from the account; you do not have to use the full credit limit. Once you make payments against the balance, that amount of credit is then available for you to use again.

Revolving accounts include lines of credit and credit cards.

Installment Credit Definition

Installment credit, in contrast, is credit where the full loan amount is disbursed at one time. You then make regular payments of a fixed amount toward the debt over a certain period of time.

Installment debt includes mortgages, auto loans, student loans, personal loans, credit-builder loans, and any other type of loan that has a regular payment schedule of fixed payments.

How Installment and Revolving Debts Affect Your Credit Score

Revolving Accounts and Your Credit Score

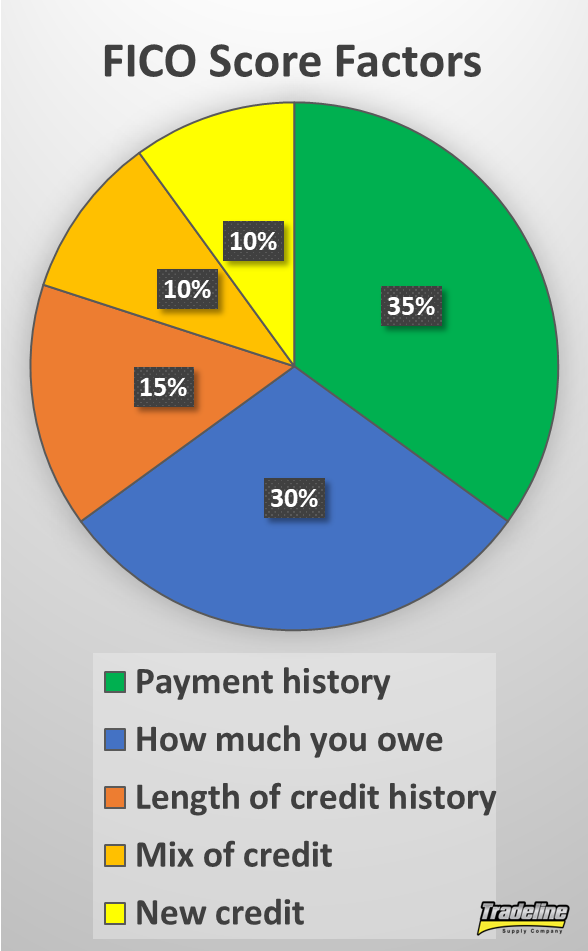

Five main factors are considered by FICO scores.

As you know from our article on credit scores, there are five main factors that influence your FICO score:

Revolving accounts can have a significant effect on each of these five factors.

As far as payment history, it’s important to pay your bills on time every single month just like any other account. However, with revolving accounts, you do not have to pay off the full balance every month. Instead, there is likely a minimum payment amount that you will be required to make. If you make a payment that is less than the minimum payment, your account will still be considered delinquent.

A lot of the power of revolving accounts comes from their influence on your utilization. This is because the credit utilization factor of your credit score places much more importance on the utilization of your revolving accounts.

Having high revolving utilization means that you are using a large portion of your available credit, which indicates to lenders that you might be at an increased risk of default. That’s why high credit utilization is bad news for your credit score.

If you run up a balance on a credit card and then only pay the minimum payment each month, you will be increasing your credit utilization. Since utilization makes up 30% of your FICO score, carrying a balance on your revolving accounts can seriously reduce your score.

Credit age is also important since it goes hand-in-hand with payment history. The longer you keep your revolving accounts open, the better. Even after they are closed, they can still continue to age and impact your average age of accounts.

Having a few different revolving accounts is also beneficial to your credit mix. Consumers with FICO scores of 785 and up have an average of seven credit cards in their credit files, including both open and closed accounts. In fact, if you don’t have enough revolving accounts, you can get dinged for a “lack of revolving accounts,” because without them there is not enough information to judge your creditworthiness, according to Discover.

Having too many inquiries for revolving accounts or too many new revolving accounts can hurt your credit score. Typically, each application for a revolving account is counted as a separate inquiry.

Installment Loans and Your Credit Score

When it comes to your credit score, installment loans primarily impact your payment history. Since installment loans are typically paid back over the course of a few years or more, this provides plenty of opportunities to establish a history of on-time payments.

Since installment loans typically don’t count toward your utilization ratio, you can have a high amount of mortgage debt and still have good credit.

Having at least one installment account is also beneficial to your credit mix, and installment debt can also impact your new credit and length of credit history categories.

What installment loans do not affect, however, is your credit utilization ratio, which primarily considers revolving accounts. That’s why you can owe $500,000 on a mortgage and still have a good credit score. This is also why paying down installment debt does not help your credit score nearly as much as paying down revolving debt.

This is the key to understanding why revolving accounts are so much more powerful than installment accounts when it comes to your credit score. Credit utilization makes up 30% of a credit score, and that 30% is primarily influenced by revolving accounts, not installment accounts.

In addition, with a FICO score, multiple inquiries for certain types of revolving accounts (mortgages, student loans, and auto loans) will count as just one inquiry as long as they occur within a certain time frame. As an example, applying for five credit cards will be shown as five inquiries on your credit report, whereas applying for five mortgage loans within a two-week period will only count as one inquiry.

Why Are Revolving and Installment Accounts Treated Differently By Credit Scores?

Now that you know why revolving accounts have a more powerful role in your credit score than installment accounts, you might be wondering why these two types of accounts are considered differently by credit scoring algorithms in the first place.

According to credit expert John Ulzheimer in The Simple Dollar, it’s because revolving debt is a better predictor of higher credit risk. Since credit scores are essentially an indicator of someone’s credit risk, more revolving debt means a lower credit score.

Since revolving accounts like credit cards are usually unsecured, they are a better indicator of how well you can manage credit.

Why is it that revolving debt better predicts credit risk than installment debt?

The first reason is that installment loans are often secured by an asset such as your house or car, whereas revolving accounts are often unsecured. As a result, you are going to be less likely to default on an installment loan, because you don’t want to lose the asset securing the loan (e.g. have your car repossessed or your home foreclosed on). Since revolving accounts such as credit cards are typically unsecured, you are more likely to default because there is nothing the lender can take from you if you stop paying.

In addition, while installment debts have a schedule of fixed payments that must be paid every month, revolving debts allow you to choose how much you pay back each month (beyond the required minimum payment). Since you can decide whether to pay off your balance in full or carry a balance, revolving accounts are a better reflection of whether you choose to manage credit responsibly.

How to Use Revolving Accounts to Help Your Credit

Since revolving accounts are the dominant force influencing one’s credit, it is wise to use them to your advantage rather than letting them cause you to have bad credit.

Here’s what you need to do to ensure your revolving accounts work for you instead of against you:

Make at least the minimum payment on time, every time.

Don’t apply for too many revolving accounts and spread out your applications over time.

Aim to eventually have a few different revolving accounts in your credit file.

Keep the utilization ratios down by paying off the balance in full and/or making payments more than once per month. Use our revolving credit calculator to track your utilization ratios.

Avoid closing revolving accounts so that they can continue to help your credit utilization.

Revolving Accounts vs. Installment Accounts: Summary

Revolving accounts are given more weight in credit scoring algorithms because they are a better indicator of your credit risk.

Revolving accounts play the primary role in determining your credit utilization, while installment loans have a much smaller impact. High utilization on your revolving accounts, therefore, can damage your score.

With a FICO score, inquiries for installment loans are grouped together within a certain time frame, while inquiries for revolving accounts are generally all counted as separate inquiries. Therefore, inquiries for revolving accounts can sometimes hurt the “new credit” portion of your credit score more than inquiries for installment accounts.

Use revolving accounts to help your credit by keeping the utilization low and keeping the accounts in good standing.

What is credit piggybacking? If you’re not sure what this strange term could possibly mean, you’re definitely not alone.

Credit piggybacking, also referred to as “credit card piggybacking” or “piggybacking credit,” is a commonly used credit-building strategy. However, many people are still unaware of how to access this strategy and use it to their advantage.

In this article, we’ll define what piggybacking for credit means and how it can help your credit.

Credit Piggybacking Definition

The general definition of credit piggybacking is building credit by sharing a credit account with someone else. For example, spouses, business partners, and parents and children are all common examples of people who often share credit.

There are three main ways in which credit piggybacking can take place, which we discuss in more detail in “The Fastest Ways to Build Credit”:

Opening an account with a cosigner or guarantor is one way to piggyback on someone’s good credit.

Opening an account with a cosigner or guarantor, which is someone who promises to be responsible for the debt if the primary borrower cannot repay it. If the cosigner or guarantor has good credit, the borrower may be able to qualify for credit that they could not qualify for on their own or qualify for better terms.

Opening a joint account with another person, which means both parties have full access to the account and are both held fully responsible for the account. By opening a joint account with a partner who has good credit, a person with less-than-ideal credit may be able to open an account that they wouldn’t have qualified for on their own or get more favorable terms.

Becoming an authorized user for the purpose of credit card piggybacking, meaning you are not responsible for the debt, but the entire history of that account may be reflected in your credit file, regardless of when you were added to the account.

When people talk about piggybacking credit, they are usually referring to the method of piggybacking using authorized user tradelines.

How Does Authorized User Piggybacking Work?

Here’s how piggybacking works as an authorized user:

When you are added as an authorized user to someone’s credit card, often (depending on the bank), the full history of that account will then be shown in your credit report, regardless of when you were added to the card.

Therefore, piggybacking can almost instantly add years of perfect payment history to the authorized user’s credit file.

Authorized user tradelines can affect many important credit variables, such as your average age of accounts, age of oldest account, overall utilization ratio, number of accounts, mix of accounts, and more.

Historically, only the wealthy and privileged were able to use piggybacking as a credit-building strategy. Now, there is a marketplace where tradelines can be bought and sold, which is helping to democratize the credit system and provide equal credit opportunity.

The issue of piggybacking went all the way to Congress, which upheld consumers’ rights to use authorized user tradelines.

Is Piggybacking Credit Legal?

While Tradeline Supply Company, LLC does not provide legal advice, we can provide evidence that supports the idea that piggybacking credit is legal.

Firstly, piggybacking for credit is an extremely common practice that has been in use since the advent of credit cards. Studies estimate that 20-30% of Americans who have credit records have authorized user accounts in their credit file.

In addition, about 25% of people who have credit reports initially established their credit files by piggybacking in one way or another.

Many banks actually encourage consumers to add authorized users for the express purpose of boosting their credit scores.

You may have heard about FICO trying to take away authorized user privileges in 2008. But what you probably didn’t hear about was FICO backing down after a congressional hearing that involved the Federal Trade Commission and Federal Reserve Board.

During the hearing, FICO admitted that they could not legally discriminate between spousal AUs and other users, because this would unlawfully violate the Equal Credit Opportunity Act.

Since the U.S. Congress has upheld consumers’ rights to use authorized user tradelines, it seems reasonable to conclude that authorized user tradelines are legal.

However, it is important to get your tradelines from a reputable source. Some tradeline companies use illegal credit profile numbers (also known as CPNs) to mislead creditors as well as consumers. That’s why consumers should only work with tradeline companies that don’t use or sell CPNs—learn more about CPNs and why Tradeline Supply Company, LLC does not accept them.

Does Piggybacking Credit Still Work?

As we discussed in “Do Tradelines Still Work in 2020?”, credit piggybacking still works, and we think it will be around for a long time.

Piggybacking credit is a well-established credit-building strategy that has been defended in Congress and promoted by banks. It is a significant part of our credit system.

Thanks to the Equal Opportunity Credit Act, authorized user tradelines are still a very important factor in credit scoring models.

Not only that, but even if FICO were to devise an algorithm intended to exclude piggybackers, it would be quite some time before lenders could implement it on a large scale. The slow-moving financial industry is still using FICO scores that were developed decades ago.

Piggybacking companies bring together buyers and sellers of authorized user tradelines.

What Do Piggybacking Companies Do?

Friends and family will often allow each other to piggyback, but for many people, it’s difficult to find someone with good credit to piggyback on. A third party can play a role in helping to connect people who are looking to purchase seasoned tradelines with people who have high-quality tradelines to offer.

Piggybacking companies, more commonly referred to as tradeline companies, simply facilitate the buying and selling of authorized user tradelines.

The tradeline company acts as an intermediary by marketing the tradelines to consumers, protecting the identities of the clients, and preventing fraud.

At Tradeline Supply Company, LLC, we provide an innovative platform through which users can buy and sell tradelines entirely online. We also provide educational resources so consumers can familiarize themselves with the credit system and how piggybacking works.

How Long Does Piggybacking Credit Take Before I See the Tradelines on My Credit Report?

The account you are piggybacking on can show up on your credit report in as little as 11 days, depending on several factors relating to the particular tradeline.

Each piggybacking tradeline has its own reporting cycle, and Tradeline Supply Company, LLC provides a “purchase by date” before which you must purchase your tradeline in order for us to guarantee that it will post in the coming reporting cycle. If you miss the purchase by date, it will simply show up in the following cycle.

If you have purchased a seasoned tradeline that you believe has not posted, first, check to make sure that the entire reporting period has passed, then check your credit reporting service again to verify that it still has not posted. If you take these steps and determine your tradeline has not posted, please reach out to us for support and we will rectify the situation.

Can Piggybacking Hurt Credit?

If credit piggybacking is done incorrectly, it can actually backfire and hurt your credit.

Because the full history of the credit account is reflected in the credit file of the piggybacker, that means any derogatory factors will show up, too.

For example, if the account has any late or missed payments, that could hurt the authorized user rather than help. Similarly, a high utilization ratio on the account could also damage the authorized user’s credit.

That’s why we recommend going with a reputable piggybacking company who guarantees a perfect payment history and a low utilization ratio (15% or lower) on all tradelines. This will virtually eliminate the risk of your credit being hurt by these factors.

The only other way piggybacking could hurt your credit is if you choose the wrong piggybacking credit card. It’s essential to choose the right tradelines for your credit file. To do this, you’ll need to figure out your average age of accounts and how adding a tradeline could affect this statistic.

For example, if your average age of accounts is five years and you decide to piggyback on a tradeline that is two years old, this would bring down your average age of accounts, which is the opposite of what you want to achieve with tradelines.

There are plenty of articles out there about the fastest ways to raise a credit score, but the focus of this article and infographic is a bit different. Rather than giving you shortcuts on how to boost your credit score, we’re talking about the fastest ways to build credit for long-term success.

While raising a credit score can be accomplished in various ways, not all of them involve actually building your credit profile by adding more accounts. Credit repair companies may offer tactics on how to raise credit scores by removing negative, inaccurate information from your credit file, but this strategy doesn’t do anything to build your credit history by establishing new accounts. They may remove harmful inaccurate information, but they often lack in assisting with credit re-establishment.

Opening a mix of several different accounts and keeping them in good standing is crucial for building a good credit record, but this process takes time. It is well-known that a credit account needs at least two years of history to be considered “seasoned,” which is when it has enough age to show that you can properly handle the account and therefore begins to improve your credit score.

Before this point, when an account is still young, it represents a risk to the lender because they don’t know if you will use the credit responsibly. They don’t know if you are going to max out your cards, miss payments, etc. That’s why new accounts often hurt your credit temporarily.

So what can you do if you don’t have 2+ years to open new accounts and wait for them to age? What if you can’t get approved for credit on your own to begin with? How do you build good credit fast?

Piggybacking: The Fastest Way to Build Credit

The answer to how to build credit fast is piggybacking. This term refers to the practice of building credit by becoming associated with someone else’s credit accounts.

This might sound surprising, but studies have shown it is a very common practice. A study of over 1 million consumers by the Consumer Financial Protection Bureau showed that nearly a quarter of consumers transitioned out of credit invisibility by piggybacking on the creditworthiness of others. According to a survey by creditcards.com, 86 million Americans have shared a credit card account with someone else!

Additionally, a study by the Federal Reserve Board found that about 30% of consumers with a scorable credit record have at least one authorized user account on their credit record.

There are three main ways that piggybacking occurs: getting credit with a co-signer, being a joint credit account holder, or becoming an authorized user.

Build Credit Fast With a Cosigner or Guarantor

One very common strategy for someone who needs help building credit fast is to apply for credit with a cosigner or guarantor, which is a person who can be responsible for the debt in the event that the primary borrower cannot repay it. The cosigner or guarantor does not typically receive access to the funds or make payments on the debt unless the primary borrower is no longer able to.

A cosigner or guarantor can help a borrower get credit by pledging to be responsible for the debt if the primary borrower cannot repay it.

Pros:

Since the cosigner or guarantor’s credit record and income are considered when applying for credit, the primary borrower may be able to piggyback off the cosigner’s good credit to qualify for credit or get better terms.

Cons:

Getting credit with a cosigner or guarantor means opening a new account, which dings credit temporarily. It is still going to take a few years for the account to age enough to help build your credit score.

It may be difficult to find someone willing to cosign on a loan or credit card since it is a risky proposition without much benefit for the cosigner.

Some lenders, particularly credit card issuers, may not even allow cosigners.

It may be difficult or impossible to remove the cosigner in the future, so the cosigner must be willing to potentially be permanently associated with the account.

Building Credit as a Joint Account Holder

As joint account holders, two parties apply for one account that they can both use. Both parties have full access to the account and both are held fully responsible for the account. Joint accounts are most commonly used by spouses with shared finances.

Joint accounts can help build credit, but they are most commonly used by spouses with shared finances.

Pros:

Both applicants are considered by the lender when issuing credit. By pairing with someone with good credit, a person with less-than-perfect credit may be able to open an account that they wouldn’t have qualified for on their own, or get more favorable terms.

If the joint account is kept in good standing over time, it can continue to help build the credit of the user who needs to improve their credit profile.

A joint account can make it easier for two people to manage their finances together.

Both account holders have access to the privileges associated with the account, such as rewards.

A joint account is also considered a primary account since each borrower has full access to the account and full liability for the debt.

Cons:

Opening a joint account means adding a new account to your credit report, which decreases the average age of accounts and can temporarily hurt your credit. The account will still need at least two years to age enough to help improve your credit score.

Both users are fully responsible for the debt. If one person maxes out the account, the other can legally be held responsible.

It’s always possible that an event such as a breakup could change the relationship between account holders, which could make it difficult to manage the account.

Disagreements over the account could damage the relationship between account holders.

It might be difficult to find someone to open a joint account with you if you do not have a spouse or if your spouse does not want to combine finances.

Not all lenders provide joint credit accounts, so options for opening a joint account are limited.

Many joint accounts do not provide the option of removing a joint account holder, so both users are often attached to the account permanently unless they decide to close it altogether.

Authorized user credit piggybacking is one of the fastest ways to build credit. Photo via seniorliving.org.

How to Build Credit Fast as an Authorized User

You’re probably already familiar with the concept of piggybacking credit as an authorized user. The classic example is parents who add their children as authorized users of their credit cards for the purpose of helping them build a credit history. Often, the young adult does not even get a credit card, so they can’t make charges to the account—the goal is solely to have the account show up on their credit report.

Pros:

The account can show up on the authorized user’s credit report as soon as the next reporting date for that credit card, which means it can build your credit fast.

Only the primary account holder is responsible for the debt incurred, not the authorized user.

Only the primary cardholder’s credit file is considered when the credit card company issues the card. Therefore, many times, an authorized user may be added to the account even if their credit is not as pristine as the primary cardholder.

The authorized user’s credit score does not affect the credit of the primary cardholder (as long as the authorized user does not increase the utilization of the account by making charges). Being an authorized user can be a great way to build credit fast, since the full history of the account is often shown in the credit reports of both the primary cardholder and the authorized user, regardless of when the authorized user was added (with some exceptions depending on the bank).

The authorized user can remove themselves from the account if they no longer want the account to appear on their credit report, such as if the account becomes delinquent.

Cons:

Authorized users don’t have the ability to make changes to the account like the primary cardholder. The primary cardholder does not even have to give the authorized user a credit card.

If the account shows any negative behaviors such as a late payment or high utilization, this will be reflected on the authorized user’s credit report, which may be counterproductive to the goal of building credit. If you buy an authorized user tradeline from a reputable company, however, the tradeline should have a perfect payment history and low utilization.

What Is the Best Way to Build Credit Fast?

While there are many ways to increase your credit score quickly, not all of them are conducive to building credit, which means strengthening your credit profile with additional accounts.

Credit repair techniques may promise to boost credit scores fast, but removing information from your credit report doesn’t help you build credit. To truly build or rebuild credit, you need to add positive credit history to your credit report.

Building credit for long-term success involves establishing a mix of different credit accounts, including credit cards and loans. These foundational accounts, with time, will aid in boosting your credit score to its highest potential.

However, if you need to build credit fast, you’ll have to take a different approach. Primary accounts need time to age and accumulate positive payment history before they can start to increase your credit score. And if you are starting with bad credit or no credit at all, it can be hard to get approved for credit accounts on your own.

The only shortcut we have seen to building credit fast is piggybacking credit. Through credit piggybacking, you can benefit from someone else’s good credit, whether that is by getting a cosigner to sign on with you, opening a joint account with someone, or becoming an authorized user on an existing account.

While the first two options are still restricted by the limiting factor of time, being added as an authorized user to a seasoned account can add years of positive credit history to your credit report almost instantly.

Therefore, if you need to build credit fast, consider adding one or more authorized user accounts to the mix, whether by asking a trusted family member or friend or purchasing them online from a reputable business.

Have you tried any of these ways to build credit fast? Share your experience with us in the comments!

Did you know that a large proportion of consumers have errors on their credit reports? Unfortunately, it’s true. In 2017, the most common complaint received by the Consumer Financial Protection Bureau (CFPB) had to do with incorrect information being reported on consumers’ credit reports.

A study conducted by the FTC in 2012 found that about 25% of consumers had at least one error on one of their credit reports. Some of those consumers were paying higher interest rates on loans as a result of those errors bringing down their credit scores.

From this information, you can see that it’s all too likely that you may have an error in your credit report. Let’s go over some of the most common types of credit report errors and how to fix errors on your credit report.

How to Get Your Credit Report

The first thing you will need to do in order to identify errors on your credit report is, of course, obtain a copy of your credit report.

You can get your credit report for free from annualcreditreport.com, which is the only website authorized by the government to provide your annual free credit report.

Under the Fair Credit Reporting Act (FCRA), you are legally entitled to receive one free credit report from each of the three major credit bureaus once every 12 months. You can choose to order all three credit reports at the same time or order each individual report at different times throughout the year.

Watch out for other websites claiming to offer free credit reports or free trials, especially if they ask you for payment information.

However, there are some reputable websites where you can view a simplified version of your credit report for free, such as CreditKarma, CreditSesame, WalletHub, and Bankrate. They are able to offer this service by advertising credit products to users.

Inspect your credit report regularly to catch errors early.

You can also request a free credit report if you are denied credit because of information found in your credit report. The credit report must be from the credit bureau that provided the original report to the lender.

In addition, you can qualify for an additional free report if you are unemployed and planning to apply for jobs, if you receive government assistance, or if you are a victim of identity theft.

Credit experts recommend checking your credit reports at least once a year, so make sure to take advantage of any opportunities to get a free copy of your credit report.

You can also pay to get your credit reports directly from the credit bureaus.

Types of Credit Report Errors

Identity Errors

Your personal information is not accurate. For example, your name is misspelled or your address is incorrect. This is an indication that the credit bureau may be confusing you with another person. This can sometimes happen with family members who have similar names or live at the same address.

Your file has been mixed with someone else’s. If you see accounts on your credit report that belong to someone else who has a similar name or the same address, this could mean that your credit report has been merged with another person’s report due to having similar personal information.

There are accounts that you didn’t open. Accounts that you know you didn’t open but are listed in your name indicate that someone has stolen your identity and used it to fraudulently open accounts.

If there are accounts in your name that you didn’t open, your identity may have been stolen.

Account Information Errors

Accounts are reported more than once (duplicate accounts). Sometimes, the same account may be shown twice on your credit report. This can definitely hurt your credit if it’s a derogatory account that’s been duplicated.

An account reports that you are the primary owner of the account when you are actually an authorized user (or vice versa). It’s possible that the credit bureaus have mixed up who is the primary owner of the account.

Closed accounts are reporting as open (or vice versa). Sometimes, accounts that you have closed in the past will still be reporting as open. This can be problematic especially if it’s a negative account, such as a collection. On the other hand, if an open account is reporting as closed, that’s also a problem because it can hurt your utilization ratio.

There are late payments on your report, but you were on time. Late payments are highly damaging to your credit score, so if you’ve never been late paying your bills but your credit report indicates otherwise, that’s an error you’ll want to correct as soon as possible.

An account has an inaccurate open date or date of first delinquency (DOFD). If an account has an incorrect open date, this could change the age of the account, which could, in turn, impact your credit score. An incorrect DOFD on a derogatory account, such as a collection account, will affect when the negative mark falls off your credit report.

Accounts show incorrect balance or credit limit information. Some credit cards do not report a credit limit at all, which could hurt your credit utilization ratio. Alternatively, your credit report may not be showing the correct balance or credit limit, which could also potentially hurt your utilization.

Clerical Errors

Inaccurate data was added back into your credit report after being corrected. If you’ve corrected an error on your credit report but then see the same error pop back up again, it could be a clerical error on the part of the credit bureaus or the data furnisher.

Duplicate collection accounts with different debt collectors are all being reported as open accounts. As we explained in our article on collections, this situation is called “double jeopardy” on your credit report. If an account has been sold to a debt collector, there may legitimately be multiple accounts for the same collection on your credit report, but the original account should be updated to show that it has been transferred and should no longer show a balance owed. The collection agency that currently owns the debt should be the only entity reporting the collection as open with a balance owed.

There is negative information on your credit report that is more than seven years old. Negative information must be removed from your credit report seven years after the date of first delinquency, so if any derogatory information on your credit report is older than seven years, you can have it deleted.

How to Fix Errors on Your Credit Report

To get the best results, write a letter for each dispute and send your letters by certified mail.

If there are any errors on your credit report, you can contact the credit bureau that is reporting the inaccurate information to resolve the issue. Your credit report should contain information on how to file a dispute.

1. Gather All Necessary Information and Supporting Evidence

When you submit your dispute, it’s important to provide all the information the credit bureau will need to process your claim.

This may include the following:

An annotated copy of your credit report (circle or highlight the incorrect item) Documentation to verify your identity (copies, not original documents)

A letter containing additional information about the item, an explanation of why it is incorrect, and a request to update or remove the incorrect item

Copies of supporting documents that provide proof of the item’s inaccuracy

2. Submit Your Credit Dispute Letter Via Certified Mail

Although it is possible to dispute credit report errors online, many credit experts recommend instead writing a letter and sending it in the mail along with documentation to verify your identity and supporting evidence.

If you try to dispute an error online or over the phone, you may not have the chance to provide enough supporting evidence, and the credit bureau may dismiss your dispute as frivolous.

It’s also recommended that you send your letters by certified mail so that you have proof that the letters have been received. In addition, it’s a good idea to keep copies of your correspondence in case you need to get outside help.

3. Send a Separate Dispute Letter for Each Error

If there is more than one error on your credit report to deal with, it is best to send a separate letter for each dispute, since the credit bureaus may reject long lists of disputes as frivolous.

4. Consider Working With a Reputable Credit Repair Company

Annotate each error in your credit report and provide documentation supporting your dispute.

If you have a lot of errors to dispute or if you have been the victim of identity fraud, you may consider hiring a credit repair service to assist with the process. [Disclosure: This article contains affiliate links.]

5. Contact the Furnisher of the Incorrect Data

You should also contact the lender that furnishes the data to the credit bureaus to ensure the inaccuracy gets corrected at the source. The FTC also provides a sample dispute letter to send to data furnishers.

If you neglect this step, the error could show up on your credit report again the next time the lender reports to the credit bureaus.

6. If Your Identity Was Compromised, Consider Placing a Credit Freeze or Fraud Alert on Your Profile

If the error on your credit report was the result of identity theft, it might also be a good idea to contact the credit bureaus to place a fraud alert or credit freeze on your account.

A fraud alert requires lenders to take extra steps to verify your identity if someone is trying to open an account in your name, whereas a credit freeze blocks anyone from viewing your credit file except for businesses that you have existing relationships with.

Keep in mind that if you are planning to buy tradelines, you must have all fraud alerts and credit freezes removed first, or the tradelines will not post.

What Happens Next?

Once the credit bureau has received your dispute, they have 30 days to investigate your claim. If their investigation cannot verify the information on your credit report, they must update it with accurate information or delete the item.

In addition, the credit reporting agency is required to provide you with written documentation of the results of the investigation.

You are also entitled to get a free copy of your credit report from the company if your credit report has been changed as a result of the dispute. This free copy is not counted as one of your annual free credit reports from annualcreditreport.com.

Upon your request, the credit bureau must notify any entity who pulled your report in the past six months about the corrections made to your report. If anyone has pulled your report for employment purposes in the past two years, you can ask to have an updated copy of your report forwarded to them as well.

What To Do If You Disagree With the Dispute Results

Option 1: Add a Consumer Statement to Your Credit File

If your dispute is rejected and you don’t agree with the credit bureau’s decision, you have the option of adding a consumer statement to your credit report to explain the situation. However, this is not necessarily the best solution.

Firstly, the statement doesn’t get factored into your credit score, so it won’t help your chances when a lender uses an automated system to approve or reject applicants. If it’s a case where an underwriter is looking at your credit report, adding a consumer statement may just draw their attention to a negative item unnecessarily, especially if the item is older.

Option 2: File Another Dispute With Additional Information

Another option is to submit a second dispute with additional supporting documentation to try to get the credit bureau to investigate the dispute a second time.

Option 3: Submit a Complaint to the CFPB

If the credit bureau still fails to correct the information in your credit report, you can submit a complaint to the CFPB.

The CFPB may not be able to force the credit bureaus, as private companies, to do anything, but getting a government agency involved might encourage the credit bureau to rethink their position.

Option 4: Take Legal Action

Continuing to report inaccurate information after you have disputed it is a violation of the FCRA. If you feel that a credit bureau is violating your rights under the FCRA, you have the option of talking to a lawyer about potentially taking legal action.

Conclusions on Credit Report Errors

Unfortunately, errors on credit reports are very common, so we all need to be vigilant about monitoring our credit for fraud and inaccuracies.

Make sure to check your credit reports regularly by claiming your annual free credit reports as well as using a reputable free or paid service throughout the year. As soon as you spot any errors, try to get to the bottom of them and get them corrected both with the credit bureaus and with the data furnishers as soon as possible.

By making sure that your credit report only contains accurate and timely information, you are helping to protect your financial health and ensuring that credit report errors don’t stand in the way of future opportunities.

Credit repair can be a long and arduous process, especially if you have very bad credit. Getting results from credit repair can take months, and it takes years to build or rebuild a solid credit history.

However, there are some “credit hacks” that you can use to improve your credit on a much shorter time scale.

In this article, we’re going to tell you the best credit hacks to improve your credit score as well as credit card hacks that work to help you save you money on interest. In addition, we’ll also provide some credit-building hacks for those with thin credit files and credit repair hacks to help you fix bad credit.

Here are the credit hacks we’ll be covering in this article. You can click on the bulleted list items below to jump directly to each hack.

Now let’s delve deeper into each credit of these credit hacks.

Credit Score Increase Hacks

Pay down high-balance cards first to improve your credit utilization

If your focus is primarily on boosting your credit score fast, you may want to consider paying down your high-balance cards first. The reason for this can be explained by the importance of individual credit utilization ratios, which refers to the utilization ratios of each of your revolving accounts.

From what we have seen, individual utilization ratios may be even more important than your overall utilization ratio. Having one or more maxed-out accounts, for example, can drag down your score even if your overall utilization ratio is low.

Therefore, by paying down your high balances first, you can get those accounts out of the high-utilization danger zone and into a utilization range that is less damaging to your credit score.

Pay off low-balance accounts to reduce the number of accounts with balances

One of the factors that are considered within the overall “credit utilization” category is the number of accounts that have balances. Having fewer accounts with balances is better for your score. In fact, the ideal credit utilization scenario is having a zero balance on all but one of your accounts and having one account with a utilization ratio in the 1-3% range.

Therefore, if you can pay some of your accounts down to zero, you should see a boost to your score. Accounts with small balances are low-hanging fruit because you don’t have to spend as much money to get them to a zero balance.

Time your payments so that you have a $0 balance on your statement date

To ensure that your credit report shows low credit utilization, time your payments so that you have a low balance (or no balance) when your accounts report to the credit bureaus.

When it comes to credit utilization, you might think that as long as you pay your credit card balance in full by the due date every month, then you should show a 0% utilization for that account. However, this assumption is not necessarily correct. The reason for this is that the date when your credit card issuer reports to the credit bureaus is often not the same as your due date.

That means that your account is reporting at some other time during the month when your card does have a balance on it. If you use a significant portion of your credit limit, that utilization could be hurting your score.

To correct this, if you want to have your accounts show a 0% utilization ratio, try using this credit hack: Instead of waiting for your statement to arrive and then paying your balance on the due date a few weeks later, you need to pay your balance to $0 before the statement closing date. Then, your statement will close with a $0 balance and that’s what will report to the credit bureaus.

Alternatively, you can pay your bill on your normal schedule and then refrain from using your card for the next entire billing cycle. Since you have paid off the balance and not made any new charges, your account will show a $0 balance at the end of the reporting cycle.

Either way, if you can shift the timing of your payments so that your account reports a 0% utilization, that could provide a significant benefit to the credit utilization portion of your credit score.

Credit-Building Hacks

Build credit fast by piggybacking on someone else’s good credit

One of the easiest and fastest ways to build credit is called credit piggybacking, which refers to the practice of becoming associated with someone else’s good credit for the purpose of helping you build your own credit history.

Piggybacking credit can help you build credit quickly, whether you open a joint account, get a cosigner, or become an authorized user.

There are three main ways to piggyback credit.

Get a co-signer or guarantor

Having a co-signer or guarantor with good credit can go a long way toward helping you qualify for credit because the co-signer or guarantor is essentially promising to assume responsibility for the debt if you default.

The downside of this strategy is that since the position of the co-signer or guarantor comes with a lot of risks, it can be difficult to find someone to take on this role for you.

Open a joint account

Since both applicants are considered when opening a joint account, you can benefit from your partner’s good credit as well as the fact that the income of both applicants can be counted. If you maintain the joint account for a while, this can allow you to build up a credit history with a primary account.

However, many banks no longer offer joint credit cards, so your options for opening a joint account may be limited. Plus, if your relationship with the other account holder ever takes a turn for the worse, it can make managing the account difficult, and you may end up needing to close the account altogether.

Become an authorized user

Becoming an authorized user on a seasoned tradeline (i.e. a credit account that already has at least two years of positive payment history associated with it) is the fastest way to build credit. Instead of opening your own primary account and waiting for it to age, you can add years of credit history to your credit profile within a few weeks or even days.

Consider applying for a credit-builder loan

If you have bad credit or if you have never used credit before, you might be feeling discouraged about the prospect of getting credit anytime soon. It can feel impossible to get credit if you have a thin credit file or a history of derogatory marks on your credit report.

A credit-builder loan can be a useful tool for those struggling to build credit. Here’s a summary of how they work:

Credit-builder loans are typically for small amounts (e.g. a few hundred to a thousand dollars).

A credit-builder loan functions like a backward version of a traditional loan: instead of receiving the funds upfront and paying the money back later, you first make all of the monthly payments and then receive the loan disbursement once you have already paid off the loan. For this reason, these types of loans are low-risk for lenders, which is why even those with bad credit or thin credit can still qualify (provided your income is sufficient for you to make the monthly payments).

The lender reports your payment history to one or more of the major credit bureaus, which allows you to build a credit history.

For more information on how these loans work and whether a credit-builder loan might be a good strategy for you to consider, check out our article, “Credit-Builder Loans: Can They Help You?”

Credit Card Hacks

Increase your credit limit

Increasing your credit limit is one of the best credit hacks. Check out our article for more tips on how to request a credit line increase.

Increasing your credit limit can be one of the easiest and fastest ways to boost your credit score. However, you’ll want to strategize a little before requesting credit line increases from your lenders.

If your financial situation has improved since opening your credit cards, it might be a good time to request a credit line increase. For example, if you have received a raise at work or your credit score has increased, that could indicate to lenders that you can handle a higher credit limit responsibly.

Wait until you have been a responsible cardholder for at least six months and you don’t have too many inquiries on your credit report to make your request. Also, don’t request an increase if you have already requested one within the past six months.

Check with your credit issuer to see whether they will need to do a hard inquiry or soft inquiry. If you don’t want to get a hard inquiry on your credit report, ask if there is an amount they may be able to approve without doing a hard pull on your credit.

You can make your request for a credit limit increase online or over the phone. Be prepared to provide some financial information and to explain why you are asking for additional credit. Calling your bank and talking to a representative may give you more opportunities to negotiate than if you make the request online.

So, how does this hack improve your credit score?

Your credit utilization ratio, also called your debt-to-credit ratio, makes up about 35% of your FICO score and about 20% of your VantageScore. It’s defined as the ratio of how much debt you owe to the amount of credit you have available. This can be calculated for your revolving credit accounts in aggregate by adding up all of your balances and dividing by the sum of all your credit limits for those accounts.

Ask your credit card issuers for lower interest rates

This is another credit card hack that is easier and quicker than you might think. All you need to do is call up each of your credit card issuers and ask them to lower your interest rate.

Try calling your credit card issuers and asking for lower interest rates—odds are good that they will grant your request.

Again, you’ll want to do a little homework before asking for a lower interest rate. Research interest rates on cards from other issuers and see if your bank can match a lower number. Explain why you’ve been a good customer and why you feel your rate should be lowered. Also, describe how your financial situation may have improved since you opened the card.

You can find a detailed script to help you negotiate on creditcards.com.

Although this tip doesn’t directly affect your credit score, it can still be hugely beneficial, especially if you are one of the 37% of American households that carry balances on their credit cards from month to month.

Lowering your interest rate decreases the debt burden that comes from interest charges each month, allowing you to pay off your debt faster. Paying off your debt faster means improving your utilization ratio, which leads to a better credit score!

Although this hack isn’t guaranteed to work, the worst that could happen is that your lenders deny your request and your interest rates stay the same. On the other hand, it could save you hundreds or even thousands of dollars in interest. Plus, you can be optimistic about your chances: polls show that over three-quarters of consumers who ask for a lower interest rate are successful in their request.

Set up automatic bill payments

Setting up automatic payments is one of the best things you can do for your credit, especially if you struggle to remember due dates or if you have accidentally missed payments in the past. Payment history is the number one factor that influences your credit score, so even one late payment can have a serious impact on your credit.

Setting up automatic payments for all of your accounts can help prevent you from accidentally missing a payment.

Take human error out of the equation by setting up automatic payments for all of your loans and credit cards. That way, you’ll never accidentally miss a payment, so you can continue to build up a positive payment history each month without even thinking about it.

Pay down high-interest balances first to save money on interest and pay off debt faster

When it comes to paying off debt, the way to save the most money on interest is to pay off your high-interest balances first. This method is called the “debt avalanche” because you’re starting with the highest interest rates and working your way down from there. (In contrast, the “debt snowball” method involves paying your debt in order of smallest to largest balances).

Transfer your balances to a card with a lower interest rate

Another popular way to get some relief from paying those astronomical interest charges every month is to transfer your credit card balances to another credit card that has a lower interest rate.

This hack works best if you have good enough credit to qualify for a balance transfer credit card. These credit cards are marketed specifically for this purpose and they typically come with special introductory offers, such as 0% APR on balance transfers for a certain number of months.

A balance transfer can help you save money on interest charges and may improve your credit utilization ratio.

Here’s how the balance transfer process works:

When you apply for the balance transfer credit card, you tell the credit card issuer the amount you want to transfer and which bank(s) you want to transfer a balance from.

Once you have been approved for the balance transfer card, the credit card issuer essentially pays off your balances at the other banks with the credit on your new card.

Your debts (plus a balance transfer fee, usually around 3-5%) have thus been transferred to your new card.

Since your balance transfer card likely has a low promotional interest rate or perhaps even zero interest for a while, you have some extra time to pay off your debt without being crushed by interest, which means you can pay off your debt faster.

As a bonus, this credit card hack can also help your credit utilization, because you are adding some available credit to your credit profile by opening a new account.

The pitfall to watch out for with this method is that it opens up the possibility of you running up your credit cards again and potentially ending up even deeper in debt than you were before. If you think having access to additional credit is going to tempt you to spend more, then it’s probably best for you to avoid this credit hack.

Credit Repair Hacks and Bad Credit Hacks

Dispute inaccurate information on your credit report (such as inquiries or derogatory items)

Check your credit report for errors that could be damaging your score and dispute them with the credit bureaus.

If you have any errors on your credit report that are bringing your score down, such as credit inquiries or derogatory items that don’t belong to you or are otherwise being reported incorrectly, then this hack could definitely give your credit a boost.

First, you need to obtain a copy of your credit report to check for errors. You can order one from each of the three credit bureaus for free once a year at annualcreditreport.com and you can order your Innovis credit report for free directly from their website.

Then, thoroughly check your credit report for any inaccuracies, such as late payments that you actually made on time, duplicate accounts, or negative information that is more than seven years old (which means it should have been deleted by the credit bureaus already).

To fix the errors on your credit report, you can dispute the items with the credit bureaus by following the instructions found on each of your credit reports. However, there are a couple of other things you should keep in mind in order to ensure your dispute process goes smoothly.

Look up a sample credit dispute letter, such as the sample letter offered by the Federal Trade Commission, that you can use as a model for writing your own letters.

Write one dispute letter for each credit report error and send in your letters one at a time. If you try to dispute several items at once, you run the risk of the claim being dismissed as “frivolous.”

Be sure to include as much evidence as possible that supports your claim when submitting your dispute. Without documentation proving that the item is being reported incorrectly, the credit bureaus could dismiss your dispute.

Send your letters along with the necessary documentation via certified mail so that you can get proof that the bureaus received them. In addition, you should also talk to the creditor that is reporting the inaccurate date to the credit bureaus in order to fix the problem at the source and prevent the error from showing up on your credit report again in the future.

Once the credit bureaus receive your dispute letters, they have 30 days to investigate the issue. If they cannot verify the information to be accurate, then they have to either update the item with the correct information or remove the item from your credit report.

For this credit hack, dispute collection accounts on your credit report that are inaccurate or outdated to have the credit bureaus update them or delete the collections altogether.

As we discussed above, if a collection account on your credit report is being reported incorrectly or doesn’t belong to you, then you can certainly dispute the inaccurate information and have the credit bureaus update or remove the item.

If, on the other hand, the collection accounts on your credit report are legitimate, then your options for removing them are limited.

Some consumers try to negotiate a “pay for delete” arrangement with the debt collector, in which the debt collector agrees to stop reporting the collection to the credit bureaus in exchange for you paying some or all of the debt. However, this strategy is risky and it does not always work in the consumers’ favor. If you do try this approach, be sure to get the agreement in writing from the collection agency.

In addition, deleting a paid account might not even increase your credit score depending on which credit scoring algorithm is being used. Simply paying the collection may be enough to boost your credit score, since some scoring models (FICO 9, VantageScore 3.0, and VantageScore 4.0) don’t penalize you for having paid collections on your credit report.

If you want to delete a collection account without paying it, unfortunately, your only legitimate option is to wait for the collection to be removed from your credit report automatically, which happens seven years after the date that you were first delinquent on the account.

Time your credit inquiries carefully when shopping for credit

If you’re planning to shop for credit in the future, you’ll probably be getting some hard inquiries from lenders on your credit report.

Lenders typically need to check your credit history before they can decide whether or not to extend you credit, so when you apply for a loan or credit card, the lender will often request a “hard pull” of your credit report from one or more of the credit bureaus.

While it’s unlikely that inquiries alone will ruin your credit score, since each inquiry can potentially subtract a few points from your credit score, it is still important to be mindful of the frequency and the timing of your credit applications in order to minimize the impact of inquiries on your credit report.

Thankfully, though, you can still shop around for the best loan without being punished by the credit scoring algorithms. FICO and VantageScore know that it’s financially smart to shop for the best rates, not risky. Therefore, they each have ways of accounting for this behavior so that your loan applications don’t have an outsize impact on your credit score.

When applying for credit, try to minimize the impact of credit inquiries by grouping your applications within a specific time frame.

FICO scores group together inquiries that occur within a certain time frame for student loans, auto loans, and mortgages. Older FICO scores allow a 14-day window for consumers to apply for multiple loans of the same type (such as mortgages), while newer FICO scores allow a 45-day window.

Each inquiry for the same type of loan within the given time period gets grouped together and only counted as a single inquiry. However, note that this rule does not apply to credit cards, for which each inquiry will be counted separately.

With VantageScore, all inquiries that are made with a 14-day period are grouped together, regardless of the types of accounts—even credit cards.

To simplify this information into a general rule, if you can complete all of your hard credit inquiries for a given type of loan within 14 days of each other, then the inquiries will be grouped together and you can avoid ending up with way too many inquiries on your credit report.

Get a rapid rescore from your mortgage lender

Once you’ve tried some of these credit hacks and optimized your credit report, the fastest way to see your results reflected in your credit score is to get a rapid rescore. For those who are about to apply for a mortgage but need to quickly update their credit report first, a rapid rescore can be an extremely valuable tool.

To trigger a manual update of your credit report, obtain verification of your tradeline’s new status from your creditor and then forward the letter to the credit bureaus.

Since rapid rescores can only be provided by mortgage lenders, if you’re not in the market for a mortgage but you need to update your credit report in a hurry, you’ll need to update your tradelines manually.

To do so, once you have made the desired changes to your tradelines (e.g. paying down your balances or correcting errors), contact your creditors and ask them to send you a letter verifying the new account information. Then, forward this letter to the credit bureaus so they can update the information in your credit report.

By initiating the update manually, you can bypass the period of time that you would otherwise have to wait until your next reporting period.

Conclusions on Hacks to Improve Your Credit

While there is no substitute for the time and effort required to establish and maintain a respectable credit history, that doesn’t mean that you can’t try some of these credit-boosting hacks to help you improve your credit right away and perhaps even save some money on credit card interest and fees.

Just make sure not to lose sight of the most important goal, which is to build good credit over time and keep your credit report in good condition long-term.

Let us know what you think of these credit hacks! Which are the best credit hacks in your opinion? Do you have any creative credit hacks that you would add to this list?

Many people are uncertain about what may happen to their credit when they get married and what can happen to their credit if they get divorced.

For example, it is commonly believed that your credit report merges with your spouse’s credit report when you get married.

Is that really true? And what happens to your credit when you get divorced?

Keep reading for an in-depth explanation of what happens to your credit score when you get married or divorced.

What Happens to Your Credit When You Get Engaged

Technically, nothing directly happens to your credit score as a result of getting engaged. However, becoming betrothed to your future spouse can come with pressure to go into debt, and can thereby indirectly affect your credit.

Financing the Engagement Ring

The first major purchase for a couple planning to marry is often the engagement ring or rings. Many people still hold onto “traditional” ideas about how much one “should” spend on an engagement ring and want to be able to purchase an expensive ring for their partner. The average cost of an engagement ring in 2019 is nearly $6,000!

Those who don’t have the cash on hand to pay for a lavish ring may feel that they need to finance one in order to please their partner or keep up with the Joneses, but be mindful of the impact this could have on your credit.

If you want to take advantage of an in-house financing plan at the store where you are purchasing the ring, you’ll likely have to open a retail credit card with the store. The inquiry on your credit report might ding your credit score by a few points, and the new retail card account will lower your average age of accounts, which is also likely to affect your score.

In addition, if the credit limit of the store card is close to or the same price as the ring, then your individual utilization ratio will be very high or maxed out on that account, and it will also contribute to an increase in your overall utilization ratio. This makes you look riskier to lenders and thus has a negative impact on your credit score.

Before financing an engagement ring, make sure you know how it could affect your credit.

Another way to finance an engagement ring is to take out a personal loan. Taking out an installment loan is generally less damaging to your credit score than opening a new revolving account such as a credit card and maxing it out immediately. However, the downside of taking out a loan to pay for the ring is that you will have to pay interest on top of the price of the ring, whereas with in-store financing you may be able to take advantage of an interest-free promotional offer.

Regardless of how you may choose to finance the jewelry, unfortunately, going thousands of dollars into debt for a ring can bring down your credit score, especially if you become overextended and can’t keep up with the payments.

Paying for the Wedding and Honeymoon

While the cost of an engagement ring can certainly get quite expensive, it typically pales in comparison to the cost of the wedding ceremony and reception.

Planning a wedding involves paying for a venue, catering, photography, flowers, invitations, and much more, and all those expenses can add up quickly. In 2018, the average amount spent on weddings in the United States, not including the cost of the honeymoon, was almost $34,000.

While it used to be commonly expected for parents to foot the bill for weddings, now, spouses-to-be are increasingly paying their own way, even if that means going into debt. Business Insider recently reported that 28% of American couples go into debt to pay for their weddings.

The expenses don’t stop there if you want a traditional honeymoon, which can add several thousand dollars to the total—over $5,000, on average.

The average cost of a wedding in the U.S. is over $30,000, and many couples resort to taking out loans to pay for their nuptials.

Needless to say, on top of the staggering amounts of student loan debt that many couples are already saddled with, spending money you don’t have to shoulder the astronomical cost of a wedding can lead to even more credit struggles.

How Does Marriage Affect Credit?

Although many people seem to believe that your credit report combines with your spouse’s credit report after you tie the knot, this is a misconception. After you get married, both parties still retain their individual credit histories and credit scores. Your partner’s accounts will not be added to your credit report and vice versa.

There is no such thing as a shared credit score for married couples. In fact, your credit report will not even indicate your marital status or your spouse’s name.

Does Marriage Affect Your Credit Score?

No, getting married does not directly affect your credit score. Since your credit report does not change when you get married, neither does your credit score.

However, just like when you get engaged and plan your wedding, your credit may be indirectly affected by your marriage due to financial actions that you may take as a married couple.

Applying for a Mortgage

One of the most important financial decisions a couple can make is whether to apply for a mortgage to buy a home and, if so, whether both parties will apply jointly or whether the spouse with the best credit score will apply individually.

If you get a joint mortgage with your spouse, make sure you are on the same page about who will be responsible for making payments.

If both you and your partner have already established a credit history before entering the marriage, then it is likely that you will have different credit scores. In some cases, your scores may be in the same credit score range, while in others, the gap may be substantial. Ideally, all couples would do well to discuss finances before committing to marriage so that no one is surprised by a bad credit score after you have already taken the plunge.

If one spouse has bad credit while the other does not, the lower credit score could damage your chances of getting approved for a mortgage or getting the best rate on your loan. In this case, it might be a better idea for the spouse with good credit to apply in their name only, or else you could end up owing tens of thousands of dollars more on your mortgage thanks to a higher interest rate.

On the other hand, if your credit scores are similar, then it would probably make sense to apply for the home loan jointly. Assuming both partners have decent credit, then applying for a joint mortgage may offer certain advantages. Namely, both your income and your partner’s income will be considered, which could allow you to apply for a larger loan than if you were just relying on one person’s income.

While getting a mortgage is certainly a huge milestone and financial commitment, since it is a type of installment loan, having a lot of mortgage debt won’t affect your credit as much as revolving accounts do.

However, it’s how you and your spouse manage the mortgage together that can have a significant impact on your credit. With a joint mortgage, both parties are responsible for paying the bill on time. If your partner is in charge of paying the mortgage bill and one month they miss the due date and get a 30-day late, since you are equally responsible for the joint account, that late payment will also show up on your credit report and can bring down your score.

Opening Joint Credit Accounts

Besides applying for a joint mortgage, there are other types of joint credit accounts that married couples may open together, such as joint credit cards or joint auto loans.

This can allow couples to more easily manage their shared finances together. As we discussed in “The Fastest Ways to Build Credit,” if one spouse doesn’t have the credit score to get approved for an account on their own, then applying for a joint credit account with their partner can be a good way to help them build credit.

As with a joint mortgage, opening any other type of joint credit account together means you can both be held fully responsible for the debt. That can be a risky move since it means you can be held accountable and your credit score will suffer the consequences if your partner shirks their financial responsibilities.

Credit piggybacking as an authorized user can help build credit if one spouse’s credit file is thin or less than perfect.

Becoming an Authorized User

When one spouse has better credit than the other, then the partner with good credit can add the other as an authorized user to one or more of their credit cards with positive payment history.

This practice, known as credit piggybacking, often results in the age and payment history of that positive account being added to the credit report of the authorized user. This can be a great way for a spouse to help their partner build credit.

In addition, unlike opening a joint account, it’s low-risk for the authorized user, who can remove themselves from the account at any time if the relationship goes south or the account becomes derogatory.

Does Divorce Hurt Your Credit Score?

Although no one goes into a marriage planning to get divorced later on, unfortunately, divorce is a reality for many couples. To protect your credit, it’s important to be realistic about the possibility of divorce and to keep it in mind when making financial decisions.

Now, let’s answer the question of whether getting divorced can hurt your credit.

If you have been operating under the belief that your credit report merges with your spouse’s when you get married, then you might have assumed that getting a divorce will hurt your credit. However, as we have seen, the act of getting married itself does not affect your credit. It’s how you manage your credit that determines how your credit score might change.

Getting a divorce can be very costly, but if you want to keep your credit in tact, don’t neglect your other bills.

The same idea applies when getting a divorce. Your change in marital status will not be shown on your credit report and will not have any bearing on your credit score. However, it is certainly possible that getting divorced from your spouse can affect your credit by other means.

The Cost of Getting a Divorce

Since you’ll most likely need to hire legal counsel, unfortunately, getting a divorce can often be quite costly. This can make it more difficult to keep up with the rest of your bills. Do whatever you can to pay all of your bills on time so that you don’t end up with any minor or major derogatory items on your credit report.

If you’re really struggling to stay afloat financially in the midst of a divorce, reach out to your creditors and ask if there are any ways in which they can accommodate your situation in this time of financial hardship. For example, some lenders may be willing to lower your payments temporarily or even let you postpone a few payments.

In addition, you could also consider getting a personal loan to help pay for your expenses until you can get back on your feet financially after your divorce.

Managing Your Joint Accounts While Going Through a Divorce

As we discussed previously, many married couples may end up with joint credit accounts, such as a mortgage, an auto loan, or joint credit cards. Getting a divorce doesn’t nullify the debt or release either party from financial responsibility. It’s a legal agreement between you and your ex-partner, not with your creditors. Your joint debts still need to be paid.

In a divorce, it can be hard to resolve who will be responsible for paying off the debt and canceling joint accounts, especially if there are strong emotions at play.

A divorce agreement may dictate who is responsible for paying joint bills, but your lenders can still hold both of you responsible for the debt.

Although a judge may assign certain debt repayment responsibilities to each party, again, this is not an agreement with the lenders, who care only about whether your bills get paid, not who pays them. Both of you can still be held liable for joint debts by the lenders.

If your ex agrees in court to pay off a joint account but doesn’t follow through, those missed payments can damage your credit score just as much as it hurts their own. If the account goes into collections, that could be disastrous for your credit.

Since you may not trust your ex to responsibly manage shared credit accounts, you’ll probably want to pay off and close any joint accounts as soon as possible.

Unfortunately, most lenders don’t allow one person to be removed from a joint account, so you can’t simply convert it to an individual account. Instead, you will most likely need to close the account altogether and then apply for a new account on your own.

As you may know from our article about closed accounts, closing an account hurts your credit utilization. If you have to close any joint credit cards that you had with your ex-spouse, for example, the credit limit of those cards will no longer be factored into your overall utilization ratio. As a result, your utilization is going to go up and your credit score likely could go down, since credit utilization is 30% of your FICO score and about 20% of your VantageScore.

Ideally, you and your ex could decide how to assign responsibility for your joint debts outside the courts. If all goes smoothly when divvying up and paying the debts during your divorce proceedings, then your credit could theoretically remain unscathed aside from the hit to your credit utilization.

However, things can get messy quickly if there is any conflict as to who should pay certain bills.

If your ex decides they don’t want to make payments on a debt that they were supposed to pay, or even if they simply make a mistake and forget to pay, then your credit will suffer from those missed payments unless you pick up the slack. Since payment history is the biggest factor in your credit score, this situation has the potential to destroy your credit.

If your ex-spouse misses a payment on a joint debt, that negative mark will also affect your credit.

Let’s say you didn’t know your ex was behind on payments and the account went to collections. Then you would have a major derogatory on your credit report, through no fault of your own!

What Happens to a Joint Mortgage When You Divorce?

Resolving the question of what happens to your joint mortgage after your divorce can also get tricky, but there are several options to consider. Each of these options will likely affect your credit but in different ways.

Option 1: Sell the House