Most of the time, when we talk about credit, we are talking primarily about the impact of open accounts. But are we underestimating the importance of closed accounts? Let’s shed some light on the less commonly addressed question of how closed accounts can affect your credit.

What Is a Closed Account on a Credit Report?

A closed account on your credit report is simply any credit tradeline that has been closed, whether it was terminated by the customer or the creditor.

There are several different reasons why an account may be closed.

If you don’t use your account for several months, it could get shut down for inactivity. Photo by Hloom on Flickr.

If you don’t use a credit card for several months, for example, you could get your credit card closed for inactivity. In this case, your credit report might say “account closed by credit grantor” for that account since the lender was the party who terminated the account.

Other reasons a credit card may be closed by the creditor include:

The credit card issuer is no longer offering that type of credit card or is replacing it with a different card

The credit card issuer determined that there was fraudulent activity on the account

The card was stolen or lost

Consumers may also want to close their own credit accounts from time to time, in which case the account might be notated as “account closed by consumer.” As an example, if one of your credit cards increases its annual fee or if you no longer feel that the fee is worth it, you might decide to close that account.

What Do Closed Accounts Mean on Your Credit Report?

Closed Accounts and Credit Utilization

Use our tradeline calculator to calculate your credit utilization ratios.

Now that you know what a closed account is and why an account may be closed, you may be wondering what a closed account on your credit report means for your credit.

The main impact of closing an account on your credit is the effect on your utilization ratio. By closing an account, you are reducing your total available credit limit, which could increase your overall utilization ratio if you have balances remaining on your other accounts.

Therefore, if you have balances on any of your other cards, you probably don’t want to close an account that is helping to keep your overall utilization down, as well as improving your ratio of low-utilization to high-utilization accounts.

On the other hand, if you pay down all your other credit cards to 0% utilization, you can safely close an account without impacting your credit utilization.

Many people believe that once an account is closed, it will no longer count toward your credit age. However, according to an article by credit expert John Ulzheimer in The Simple Dollar, this is a myth.

“Credit scoring models like FICO and VantageScore do indeed consider the age of your oldest account and the average age of your accounts when calculating your credit scores. However, closing an account does not remove its history — including its age — from your credit reports.

Not only will the history of a closed account remain on your credit reports, but credit scoring models will continue to consider the age of the account as well. And, even better, a closed account continues to age. So, if you closed a five-year-old credit card today… in 12 months it’s going to be a six-year-old credit card.”

Are Closed Accounts on Your Credit Report Bad?

Closed accounts on your credit report are not inherently a bad thing. In fact, they can often be a good thing, as we will elaborate on below.

Closed accounts on your credit report, unless they are derogatory, are not bad for your credit. In fact, they are probably giving your credit a boost.

However, derogatory closed accounts can definitely have a negative impact on one’s credit.

For example, if you had a credit card closed due to delinquency, meaning the creditor closed the account because you had stopped paying it, the account likely still has a balance owed.

Having a closed credit account with a balance on your credit report could really hurt your credit. According to some sources, closing a credit account removes its credit limit, so a credit card account closed with a balance would be considered maxed out or over-limit.

Credit utilization is a major influence on your credit score, so maxing out your utilization by having a credit card account closed with a balance could result in a big dip in your score.

However, other sources say that a closed account with a balance will be treated as an open account until the balance is paid off, at which point you can expect some damage to your score, especially if you have balances on your other credit cards.

The specific way that closed accounts are treated may depend on which credit score algorithm is used to calculate your score as well as other variables in your credit profile.

Should I Pay Off Closed Accounts on My Credit Report?

If your account was closed with a balance but remains in good standing, maintain its good standing by continuing to make payments until the account is paid off.

If your account was closed due to delinquency, the first thing to do is call your credit card issuer to check the status of the account. If the debt hasn’t been sold to a collections agency yet, you’ll want to start paying off the account immediately to prevent it from going to collections. You could end up with bad credit if you have a collection account on your file.

If the account is already in collections, however, whether or not you should pay it off is an entirely different question that depends on your individual situation.

See our article on collection accounts on your credit report for more information on how to handle collections.

Open vs. Closed Accounts on Credit Report

In the tradeline industry, we often get questions about whether closed accounts have an impact on one’s credit and, if so, what value they hold relative to open accounts.

It is possible to have a good credit score without having any open accounts. Photo by CafeCredit.com, CC 2.0.

This is an important question, because generally when you buy tradelines you are an active authorized user for two reporting cycles, and after you are removed from the account, it will begin to show as a closed account on your credit report.

Therefore, it is useful to know what impact the tradeline might have after it converts to a closed tradeline.

From what we have seen, closed accounts often can still be a very powerful influence on one’s credit score.

Remember, the age of a closed account still factors into your credit, and accounts continue to age even after they have been closed. Age and payment history go hand-in-hand and together make up 50% of a FICO score, and since closed accounts can still contribute to these factors, this implies that closed accounts can still have a strong effect on your credit.

However, closed accounts may have a diminishing impact over time, since credit scores tend to prioritize recent events.

Can You Have Good Credit With Only Closed Accounts?

It is possible to have a good credit score while only having closed accounts in one’s credit report. We have seen examples of people with credit scores in the 700’s who only had closed accounts in their credit file.

Can I Have Closed Accounts Removed From My Credit Report?

If you have closed accounts on your credit report that are not delinquent or hurting your credit, then there is no need to remove them. They may actually be helping your credit, even though they are closed.

Accounts that were closed in good standing should automatically fall off your credit report after 10 years, while delinquent closed accounts will fall off your credit report after 7 years.

How to Get Rid of Closed Accounts on Your Credit Report

If your credit card has been closed, you can try calling your credit card issuer to ask if the account can be reopened, but don’t wait too long.

If a closed account on your credit report is reporting inaccurately, then you can dispute it and have the credit bureaus update the account with the correct information or remove it.

Contact each credit bureau or check their websites for instructions on how to dispute accounts on your credit report.

If a Credit Card Is Closed, Can It Be Reopened?

In some cases, consumers may be able to reopen closed credit cards.

If your account was closed due to fraud or delinquency, banks typically do not allow these accounts to be reopened.

If it was closed voluntarily on your part or closed due to inactivity, however, you might have a chance to reopen the account if you don’t wait too long.

Only some banks will allow this, and those that do have varying time limits as to when you can reopen an account, so check with your credit card issuer.

If you’re within the time window and your account is eligible to reopen, here’s how to reopen a closed credit card account:

Call the phone number provided on the back of your credit card (or if you don’t have the physical card anymore, look up the phone number for the customer service department for that card).

Be ready to provide your personal information and answer security questions.

Explain why you closed the account and why you are requesting to reopen it.

Some issuers may require a hard inquiry before they can approve your request, which could cause a small, temporary drop in your credit score.

If your bank doesn’t allow you to reopen the card, the next best solution might be to re-apply for the same card or apply for a new credit card altogether.

Take-Home Points About Closed Accounts

Accounts may be closed voluntarily by the consumer or closed by the creditor due to inactivity, fraudulent activity, or delinquency.

Closed accounts are not necessarily bad and can even help your credit.

Closing an account could affect your credit utilization.

Closed accounts still contribute to your credit age and they continue to age even after they are closed.

Closed accounts can still have a powerful impact on credit scores.

Continue paying off accounts that were closed with balances to prevent them from going to collections.

You can dispute closed accounts that are not reporting correctly.

You may be able to reopen a closed credit card account depending on the circumstances.

As identified coronavirus infections increase rapidly in the U.S., the biggest economic effects will be felt months from now. Still, analysts at Oppenheimer have projected that five U.S. credit card lenders will remain profitable in 2021, despite a large increase … Continue reading →

Borrowers who have defaulted on their federal student loans will get a temporary reprieve from having their wages, Social Security benefits and tax refunds garnished by the federal government, the U.S. Education Department announced on Wednesday. This break will last … Continue reading →

Wednesday, March 25, 2020 Last week in Gonzales v. Credit One Bank, N.A., No. 19-cv-00733-DAD-BAM, 2020 U.S. Dist. LEXIS 46236 (E.D. Cal. March 17, 2020), the court compelled arbitration of a plaintiff’s TCPA lawsuit against Credit One. Plaintiff sued Credit One … Continue reading →

WASHINGTON — The U.S. Congress is considering authorizing the Federal Reserve to pay the tab as local governments ramp up shipments of testing equipment, masks and ventilators desperately needed to diagnose coronavirus cases, treat patients and keep medical personnel safe. … Continue reading →

Wednesday, March 25, 2020 In re Midland Credit Mgmt., Case No. 11-md-2286-MMA (MDD), 2020 U.S. Dist. LEXIS 49091 (S.D. Cal. March 18, 2020) originated in 2011. A lead class action member and several dozen individual member cases that alleged the … Continue reading →

Federal financial regulators are encouraging banks, credit unions, and other financial institutions to offer responsible small-dollar loans to consumers and small businesses during the coronavirus crisis. Small-dollar loans — which are typically between $300 and $5,000 — can help Americans … Continue reading →

By Brad Petrishen Telegram & Gazette Staff Posted Mar 24, 2020 at 9:03 PMUpdated Mar 24, 2020 at 9:03 PM WORCESTER – A subsidiary of Target has agreed to pay nearly $2.3 million to settle a class-action lawsuit filed by a Clinton woman who alleged it engaged in illegal debt … Continue reading →

Chase (JPM), Citi (C), and Capital One (COF) are just some of the credit card companies offering financial assistance to those affected by the coronavirus pandemic. The credit card issuers, in some cases, are offering deferred payments, waiving fees, and increasing credit limits … Continue reading →

FICO, the company behind the creation of the original FICO credit score and its many subsequent iterations, has announced the latest model in their line of credit scoring algorithms: the FICO Score 10 and the FICO Score 10 T. The “T” in the latter scoring model stands for “trended,” which reflects the incorporation of trended data over time into the algorithm.

Thanks to not only the trended data but also a few other major changes, the new scoring models are claimed to be superior to all previous FICO scores.

Although the majority of consumers are not likely to see a dramatic change in their credit scores, some groups of consumers may experience more extreme shifts. Ultimately, the new FICO scores are predicted to widen the gap between consumers with good credit versus those with bad credit.

However, none of that matters until FICO 10 and 10 T actually start being used, which could still be a few years away.

Keep reading to get all the facts on FICO 10, including what makes it different from previous FICO score versions, the impact it will have on credit scores, and when we will start to see lenders adopting it. Most importantly, we’ll tell you how to get a good credit score with FICO 10.

Why Did FICO Come Out With a New Credit Scoring Model?

The whole point of a credit score is to communicate a consumer’s level of credit risk to lenders so that lenders can make less risky decisions when granting credit. Lenders want to avoid extending credit to borrowers who are likely to default on a loan because defaults represent losses for the company.

So, the more accurate a credit scoring model is at predicting consumer credit risk, the more useful it is to lenders. With a predictive credit scoring model, lenders can make more informed lending decisions, which helps their bottom line.

For this reason, the goal of each new credit score is to make it better than the last version at predicting credit risk, and that is exactly what FICO 10 is designed to do.

Consumer Debt Is on the Rise—But So Are Credit Scores

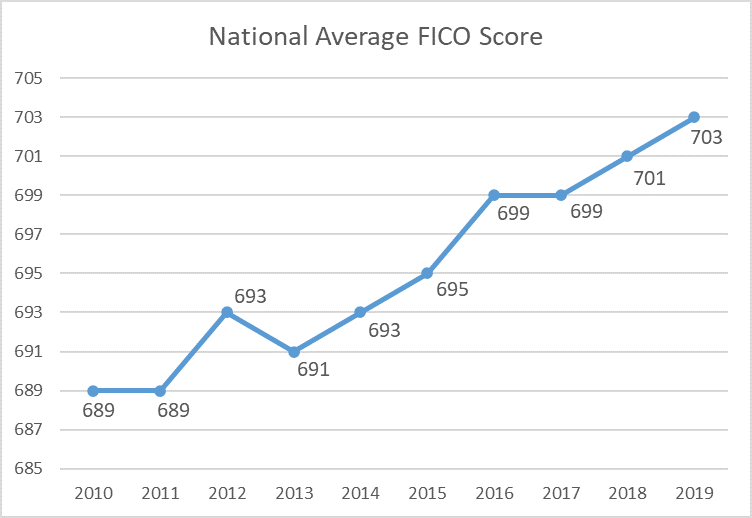

According to The Balance, consumer debt has increased to record levels, and yet the average credit score in the United States has also increased to 706 as of September 2019. This can be attributed partly to economic conditions over time, but there is another major factor that has the banks worried.

The national average FICO score has been on the rise for the past decade and it surpassed the 700 mark in 2018.

It has now been 12 years since the Great Recession of 2008, which means almost all of the delinquencies and derogatory marks on consumers’ credit reports from that period of financial hardship have been removed from their records. Therefore, creditors can no longer see how consumers handled the recession and whether they were able to pay all of their bills when the economy went south.

Couple this with the fear of another possible economic recession on the horizon, and you can understand why lenders have started to feel concerned that delinquencies and defaults may soon begin to rise to a level that is not reflected in consumers’ high credit scores.

Because of these economic factors, the credit scoring system needed an overhaul that would take into account the changing economic climate as well as changing consumer behavior and allow for better predictions of credit risk and default rates.

FICO 10: More Accurate Predictions of Credit Risk

FICO predicts that FICO 10 will lower defaults on auto loans by 9% and defaults on mortgages by 17%.

Due to the changes made to the scoring model that we discussed above, especially the inclusion of trended data for the FICO score 10 T, FICO claims that the new scores perform better than all previous FICO scores by substantially lowering consumer default rates.

Here’s what else FICO has to say about their new products:

“By adopting the FICO® Score 10 Suite, a lender could reduce the number of defaults in their portfolio by as much as ten percent among newly originated bankcards and nine percent among newly originated auto loans, compared to using FICO® Score 9. The reduction in defaults is even higher for newly originated mortgage loans, at 17 percent compared to the version of the FICO Score used in that industry. These improvements in predictive power can help lenders safely avoid unexpected credit risk and better control default rates, while making more competitive credit offers to more consumers.”

How Is FICO 10 Different Than Previous FICO Scores?

Although FICO routinely updates their credit scoring algorithms every five years or so, this will be the first time that they are releasing two different versions of the same general scoring model: FICO 10 T, which uses trended data; and FICO 10, which does not use trended data.

Both FICO 10 and FICO 10 T will be drastically different than the previous FICO score, FICO 9. FICO 9 was designed to be very forgiving to consumers, which led many to believe that it produced credit scores that were higher than they should have been.

With FICO 9, for example, medical collections were given less weight than other types of collections, which was a benefit to consumers struggling with medical debt.

Furthermore, FICO 9 completely ignored paid collection accounts, meaning that if you had a collection on your credit report but then paid the balance, it would no longer affect your credit score. Many felt that this change contributed to FICO 9 overestimating the creditworthiness of consumers, which in turn led to the scoring model not being accepted by many industries.

In contrast, the FICO 10 scores represent a swing back in the opposite direction. It is designed to be less lenient toward consumers with risky credit behaviors in order to avoid understating consumers’ credit risk. In that sense, it is probably more similar to FICO 8 than to FICO 9. However, FICO 10 also rewards consumers who have successfully managed their credit.

To accomplish this, FICO made some significant changes in creating their latest set of credit scoring algorithms.

Trended Data

The new FICO 10 T score is the first FICO score to look at trended credit data.

The FICO 10 T score will incorporate trended data, which means that it will not just consider your credit profile as a “snapshot” in time, but rather, it will take into account your credit behavior over the previous 24 to 30 months and how your credit profile has changed in that time.

VantageScore 4.0, a competing credit scoring model, has been using trended data since it debuted in 2017. Now, FICO is following suit with their 10 T score.

Because of the more extensive temporal data set FICO 10 T has to draw from, it is even more predictive of a borrower’s credit risk than the basic FICO 10 score, which can only see a “snapshot” of your credit report at a given point in time.

For consumers, the trended data factor is especially significant for the credit utilization portion of your credit score. Of course, credit scores already looked at your payment history from the past seven to 10 years, but until now, they only looked at your credit utilization ratios at a given point in time.

This means that with most credit scoring models, even if you max out your credit cards one month and your credit score suffers as a result, as long as you pay down your cards again by the next month, your score can still bounce right back to where it was before you maxed out the card.

With FICO score 10 T, however, it won’t be so easy to recover from high balances, because a record of being maxed out could stick around for the next 24 to 30 months.

In addition, if your balances have been climbing higher over the last two years or if you have been seeking credit more aggressively, you could be penalized by FICO 10 T, because this kind of behavior indicates a higher risk of you defaulting in the future.

On the other hand, if you have been managing your credit well and your debt levels have been decreasing over the past two years, you will be rewarded for that behavior.

Personal loans from online lenders have exploded in popularity, but it’s best to avoid them if you want to get a high FICO 10 credit score.

Personal Loans Will Be Penalized

The vice president of scores and analytics at FICO, Joanne Gaskin, has said that the most significant change to the scoring algorithm is the way it treats personal loans.

Personal loans are growing faster than any other type of consumer debt, even credit cards. Consumers are turning to personal loans to consolidate credit card debt more frequently than in the past, and the proliferation of financial technology companies has made personal loans easier to qualify for and more accessible.

With older FICO models, personal loans are treated the same as any other installment loan. Since the balances of installment accounts don’t affect credit scores as much as the utilization ratios of your revolving accounts, with most scoring models, taking out a personal loan to consolidate credit card debt (essentially converting revolving debt into installment debt) would benefit a consumer’s credit score.

However, many consumers who take out personal loans to pay off revolving debt don’t change the spending habits that got them into debt in the first place. Consequently, after getting a personal loan and paying down their credit cards, they may run up their cards again and find themselves even deeper in debt.

According to FICO, the credit risk of such consumers is higher than you would think based on their credit scores using previous FICO models. To account for this, FICO 10 is treating personal loans as their own category of credit accounts and is potentially penalizing consumers for taking out personal loans.

With FICO 10 T, recent missed payments will matter even more than they already do with other FICO score versions.

Therefore, with FICO 10, the strategy of consolidating credit card debt with a personal loan might not help your credit score as much as you hope and might even hurt it. However, the negative impact of taking out a personal loan can be mitigated by steadily working to reduce your overall debt level.

On the other hand, if your overall debt load stays the same or continues to increase after you take out a personal loan, that could hurt your credit score because it shows lenders that you are getting deeper into debt and not managing your credit well.

Recent Missed Payments Will Be Penalized More Heavily

Payment history has always been the most important part of a FICO credit score, but it is even more important with FICO 10 T, the trended data score.

Using historical data, it can assign late and missed payments even more weight based on your behavior in the past 24 months. For example, if you’ve been getting progressively farther behind on payments over time, the negative impact on your credit score could be even greater than it would with a previous FICO score.

If you have delinquencies that are at least a year old, though, then those older negative marks on your credit report won’t hurt your score as much, according to MSN.

How Will the FICO 10 Scoring Model Affect Credit Scores?

Overall, it is predicted that the new FICO 10 scoring models will have a polarizing effect on consumers’ credit scores, which means that some consumers who have bad credit scores may see them drop even further, while those who have good credit scores because they are on the right track may be rewarded with even higher scores.

40 million consumers are likely to experience a credit score drop of 20 or more points with FICO 10 compared to previous models. This could push some consumers over the edge into a lower credit rating category.

FICO has estimated that approximately 100 million consumers will probably experience minor changes of less than 20 points to their scores. The company also estimates that about 40 million consumers will see their credit scores drop by 20 or more points, while another 40 million could see their scores increase by the same amount.

You are likely to see a credit score drop if you took out a personal loan to consolidate debt but then kept accruing more debt instead of paying it off, or if you have credit card debt that you are not paying down.

You are most likely to see a credit score increase if you have been penalized for having high balances from time to time, since the temporal data from FICO 10 T will help to average out the peaks in your utilization rate.

While a decrease of 20 points in your credit score isn’t catastrophic, it could be enough to make a difference in your chances of being approved for credit or the interest rates you could qualify for. This is especially true for those whose credit scores sit near the lower border of a credit score category.

For example, if someone with a credit score of 595 with FICO 8 is considered to have fair credit. If FICO 10 gave them a credit score that is 20 points lower, their credit score would be 575, which is considered bad credit. That could very well make or break your chances of getting approved for a loan or a credit card.

On the other hand, the inverse is true for those who stand to gain 20 points. If a 20 point increase pushes a consumer over the edge from fair credit to good credit, for example, this could certainly be beneficial when applying for credit.

It’s estimated that 80 million consumers will see a significant change in their credit scores with FICO 10, which may move them into different credit score ranges.

Less Severe Score Fluctuations

As you may recall from How to Choose a Tradeline, the more data there is contributing to an average, the more difficult it is to affect that average.

Since FICO 10 T looks at your credit utilization for an extended period of time instead of just the current month, it is likely that your credit score will not change as drastically from month to month based on your utilization ratios at the time.

In other words, your utilization data from the past 24 to 30 months will have a stabilizing effect on your score that will protect it from being heavily penalized if you occasionally have high balances. For example, if you spend extra on your credit cards in December to prepare for the holidays, your score that month won’t be hurt as much as it would without the trended data (as long as you pay it off quickly).

Greater Emphasis on Trends and Recent Data

FICO 10 T will especially reward consumers who have a trend of improving their credit over time.

The inclusion of trended data with FICO Score 10 T and extra emphasis on recent data means that your credit score is not based solely on what your accounts look like today, but instead, it will give more importance to whether your credit is getting better or getting worse.

Hypothetically, it’s possible that two consumers with the same amount of debt and derogatory items could have different credit scores based on the trend in their debt levels.

If one consumer has $10,000 of credit card debt, but they have been making progress on paying that down from a starting point of $20,000 of debt, then their credit score would be helped by FICO 10 T because their debt level is demonstrating a trend of improvement over time.

If the other consumer also has $10,000 of credit card debt, but they used to only have $1,000 of revolving debt, that trend shows that they are getting deeper into debt, and their FICO 10 score would be hurt by that pattern of increasing debt.

A Polarizing Effect on Credit Scores

One of the major effects of FICO 10 is that it is likely going to polarize the pool of consumers’ credit scores. In other words, those near the top of the credit score range will get even higher, while those with low credit scores will sink even lower along the scale.

According to CNBC, consumers with scores of lower than 600 will experience the largest reductions in their credit scores with FICO 10. Those with scores of 670 and above could possibly gain up to 20 points.

This creates a distribution of credit scores that is more concentrated at the two extremes, as opposed to most consumers’ credit scores being concentrated around the average.

Unfortunately, that means the negative effects of the new FICO scores will disproportionately impact consumers who are already struggling with debt. This will make it even harder for consumers to get out of debt and may force them to seek out costly, predatory loans, which only accelerates the downward spiral of debt.

This perpetuation of inequality in the credit scoring system is not new, but it seems that FICO 10 will only serve to increase credit inequality rather than improve it.

Ultimately, FICO’s clients are the banks, and their products are designed to give banks the upper hand, not consumers.

When Will the New FICO Score Be Rolled Out?

By widening the divide between consumers with good credit and those with bad credit, it seems that FICO 10 will exacerbate credit inequality.

According to FICO, the FICO Score 10 Suite of products will be available in the summer of 2020. The vice president of scores and predictive analytics at FICO, Dave Shellenberger, told The Balance that Equifax will be adopting the new score shortly thereafter.

As to when lenders will actually start to use the new credit scoring system, that is a different question.

Lenders Are Slow to Adapt to New Credit Scoring Systems

The financial industry adapts very slowly to systemic changes. As we discussed in “Do Tradelines Still Work in 2020?”, there are many, many different versions of FICO, and the majority of lenders are still using versions of the score that are years or even decades old.

Before FICO 10, the latest version had been FICO 9, which has largely gone unused by lenders.

FICO 8 is the credit scoring model that is currently being used by the three major credit bureaus and it is also the most widely used model among lenders today. FICO 8 debuted in 2009, which means it has now been around for over a decade.

There are certain industries that rely heavily on FICO score versions that are even older than FICO 8. In the mortgage industry, the most popular FICO scores are versions 2, 4, and 5, the earliest of which debuted in the early 1990s. Auto lenders may use FICO scores 2, 4, 5, or 8, while credit card issuers use models 2, 3, 4, 5, and 8.

Furthermore, many industries and even some large lenders have their own proprietary FICO scoring models which have been customized for that particular institution and the consumer base they serve.

Lenders have amassed huge troves of data based on a specific credit scoring model. Having reliable data is crucial to minimizing risk during the underwriting process. If lenders were to change to a new scoring model, all of the credit scoring information they have collected so far would no longer be applicable, since it was calculated using a different algorithm.

It is likely that the FICO 10 T score will take longer to implement than the basic FICO 10 score because FICO 10 T will require businesses to train employees to use a new set of reason codes.

They would essentially be starting from scratch, which would mean taking on more risk until they have tested the new model for long enough to understand how it works for their businesses. Because of this, lenders are often reluctant to upgrade to a newer scoring model and slow to implement it.

Therefore, we can make an educated guess that it will most likely take at least a few years for FICO 10 to gain traction with lenders on a large scale. According to Shellenberger of FICO, it may take “up to two years” before lenders start using the new model, although based on past examples, it seems likely that it could take a lot longer than that.

FICO 10 T Will Be More Challenging for Lenders to Adopt

According to FICO, the standard FICO 10 score uses the same “reason codes” as older FICO scores. Reason codes, also referred to as “adverse action codes,” are the codes that lenders must provide if they have rejected your application for credit based on information from your credit report. These codes usually consist of a number and a brief statement of something that is impacting your score in a negative way, such as revolving account balances that are too high compared to your revolving credit limit.

Because FICO 10 shares the same reason codes with previous versions of FICO scores, this means it will be compatible with lenders’ current systems, at least with regard to reason codes.

In contrast, FICO 10 T comes with a new set of reason codes, which means it will be a more extensive undertaking for banks to implement the new score and train employees on how to use it.

For this reason, it seems likely that the basic version FICO 10 may see widespread use among lenders before FICO 10 T does.

How to Get a Good FICO 10 Credit Score

Although some significant changes have been made to the FICO 10 credit scoring products, the overall principles of managing credit remain the same. Most importantly, make all of your payments on time, every time, and try to keep your credit utilization low.

However, there are a few specific points to keep in mind if you want to get a good credit score with FICO 10.

Think twice about taking out a personal loan

Since personal loans will be more heavily penalized with FICO 10 scores, you’ll want to avoid taking out a personal loan unless it’s absolutely necessary. Instead of relying on personal loans to support your spending, try to save up for large purchases in advance, and start funneling some cash from each paycheck into an emergency fund in case you run into financial hardship.

If you do end up needing to use a personal loan, try to pay it down as quickly as you can. In addition, don’t run up the balances on your revolving accounts again, because the FICO 10 T algorithm does not reward this behavior, and your credit score will reflect that.

Consider setting up automatic payments for all of your accounts so that you never accidentally miss a payment.

Never miss a payment

Avoiding late or missed payments is of the utmost importance with any credit score, but it is even more important with the new FICO scoring system. Late and missed payments may be assigned more weight based on your recent credit history, especially missed payments that occurred within the past two years.

To avoid missing any payments, set up all of your accounts to automatically deduct at least the minimum payment from your bank account before your due date each month. Also, it’s a good idea to get into the habit of checking your accounts regularly to make sure there haven’t been any errors or issues with processing your automatic payments.

If you do accidentally miss a payment, pay the bill as soon as you notice and consider asking your lender to waive the late fee. If you manage to catch up before 30 days have gone by, then you can avoid getting a derogatory item added to your credit report.

In the event that you find yourself with a 30-day late (or worse) on your credit report, then you will need to be extra vigilant about making payments on time for at least the next one to two years if you want your score to recover.

Pay off your credit cards in full every month

Paying off your credit cards in full is always a good idea in general because that way, you can avoid wasting money on interest fees. In addition, paying off your full balance each month prevents your credit utilization from increasing from month to month, as opposed to carrying over a balance and then adding more to it each month.

With trended data playing a large role in your FICO 10 T score, consistency is key, and paying your bills in full every time will help boost your score.

If you want to get a good credit score with FICO 10 and FICO 10 T, try to keep your revolving debt low by paying off your credit cards in full every month.

Lower your credit utilization ratios

With FICO 10 T, it will be more important than ever to be vigilant about maintaining a low credit utilization ratio. Since the trended scoring model accounts for patterns in your credit utilization over the past 24 months, it won’t be so easy to get away with maxing out your credit cards one month and then quickly paying the balance down to improve your score again the next month.

High credit utilization at any point in the past two years could be factored into your credit score, especially if your utilization has been increasing over time.

For this reason, if your credit is being scored with the FICO 10 T model, you’ll get the best results if your credit utilization has been consistently low or if it has shown a pattern of decreasing over time.

However, just because you pay off your credit card in full every month doesn’t mean it will report a zero balance. The balance that reports to the credit bureaus is the balance that you have at the end of your statement period. If your balance happens to be high on that date, then it could negatively affect your score, even if you pay off the balance soon after.

One way to get around this is to pre-pay your credit card bill before your due date and your statement closing date. That way, the balance will be low when the card reports to the credit bureaus, which is better for your credit score.

Another helpful credit hack is to spread out multiple smaller payments throughout the month so that the balance never climbs too high to begin with.

Requesting a credit line increase can be an easy way to improve your utilization rate, but this method should be used with caution if you think it might encourage you to rack up more debt.

Increase your credit limit

One way to easily lower your utilization rate is to increase your credit limit. Spending $1,000 on a card with a credit limit of $5,000 is a lot better than spending the same amount on a card with a credit limit of $2,000.

Increasing your credit limit might be easier than you think. It could be as simple as calling up your card issuer on the phone or applying for a credit line increase online. Most people who ask for a higher credit limit get approved, according to creditcards.com.

However, this strategy is not encouraged for consumers who may be tempted by the higher credit limit to spend even more on the card.

For tips on how to get a larger credit limit, as well as some pitfalls to watch out for before requesting an increase, check out “How to Increase Your Credit Limit.”

Work to improve your credit health over time

With FICO score 10 T including more information about your credit history over the past 24 months, it will be important to demonstrate an improvement in your credit over time. Consumers who have been working to manage their credit responsibly and who have reduced their amount of revolving debt over time will be rewarded.

On the other hand, those whose credit health has been declining due to increasing debt levels or a series of missed payments will see their credit scores take a dive.

Will the New FICO 10 Score Affect the Tradeline Industry?

First, remember that it’s likely that it’s going to take at least a few years for FICO 10 to be widely adopted by lenders (if lenders choose to use it in the first place, which they may not), which means that nothing is changing for the tradeline industry in the near future.

Secondly, many lenders may choose to adopt only FICO 10 and not FICO 10 T because it will be technically easier to implement. For lenders using FICO 10 without the trended data, there is no change to how authorized user tradelines work.

However, things get more interesting when considering the impact of FICO 10 T on buyers and sellers of tradelines. Until FICO 10 T is adopted by major lenders, we can only speculate as to the changes that will result, but here is one possibility.

What If FICO 10 T Reveals a Tradeline’s Balance History?

One concern that consumers may have is that FICO 10 T will expose a tradeline’s previous high balance if it had one at any point during the past 24 to 30 months. That may be true, but we also know that FICO 10 T places a lot of importance not just on the numbers themselves, but on how they change over time.

All of the tradelines on our tradeline list are guaranteed to have a utilization ratio of 15% or lower. If a tradeline had a higher balance at some point in the past two years or so, then it would show a trend of the balance decreasing, since the balance would have been brought down to under 15% in order to participate in the tradeline program.

FICO 10 T rewards downward trends in utilization, so it seems that authorized user tradelines would still provide value even if higher balances can be seen in the past.

If a tradeline has not had a high balance in the past two years, then that means it will show a pattern of consistently low utilization, which is also beneficial.

Conclusion: What Does the New FICO 10 Credit Score Mean for Consumers?

A lot of speculation and bold claims have been circulating about the new FICO scores, FICO 10 and FICO 10 T. Naturally, consumers and tradeline sellers alike are concerned with the question of how these new scores might affect authorized user tradelines.

It is true that FICO has made some significant changes to their latest credit scoring model, and it’s also likely that some consumers may experience marked increases or decreases in their credit scores compared to previous FICO scoring models. Fortunately, however, there is no need to panic.

Follow the general guidelines of good credit to get a high score with any credit scoring model.

First, let’s remember that FICO 10 is not in use yet, and it’s probably going to take a few years or more for the majority of lenders to adopt it. In addition, the scoring model that people are most concerned about, FICO 10 T, will take even longer than FICO 10 to reach mainstream popularity since it requires lenders to learn how to start using a new set of reason codes.

For this reason, consumers do not need to worry about lenders seeing the past two years of their credit histories just yet. However, knowing that widespread use of trended data may be on the horizon, you may want to start preparing your credit now. That way, when trended data credit scores become more popular, your credit will be strong and ready to withstand the changes.

To achieve a high credit score with FICO 10 and FICO 10 T, avoid taking out personal loans if you can, as they will be penalized more heavily than in the past. It’s also important to demonstrate either an improvement in your credit over time or consistently good credit habits, which will be rewarded.

Aside from these special considerations, FICO 10 and FICO 10 T still rely primarily on the same credit score factors you are already familiar with: payment history, credit utilization, length of credit history, credit mix, and new credit. While the peripheral details of different scoring models may vary, the core components always remain the same.

Ultimately, if you work on developing good credit practices in these general areas, your credit will be in great shape no matter which scoring model is used.

FICO, the company behind the creation of the original FICO credit score and its many subsequent iterations, has announced the latest model in their line of credit scoring algorithms: the FICO Score 10 and the FICO Score 10 T. The “T” in the latter scoring model stands for “trended,” which reflects the incorporation of trended data over time into the algorithm.

FICO, the company behind the creation of the original FICO credit score and its many subsequent iterations, has announced the latest model in their line of credit scoring algorithms: the FICO Score 10 and the FICO Score 10 T. The “T” in the latter scoring model stands for “trended,” which reflects the incorporation of trended data over time into the algorithm.