Sen. Elizabeth Warren’s recent proposal to alleviate student debt for tens of millions of Americans isn’t as palatable for credit unions as it is for borrowers. Warren, who is running for the Democratic nomination for the 2020 presidential election, has … Continue reading →

Credit reports were the most-complained-about product in 2018, an analysis of Consumer Financial Protection Bureau database finds. The three major credit bureaus, Equifax, Experian and TransUnion, were the most-complained-about companies last year. Mistakes on their reports can result in consumers … Continue reading →

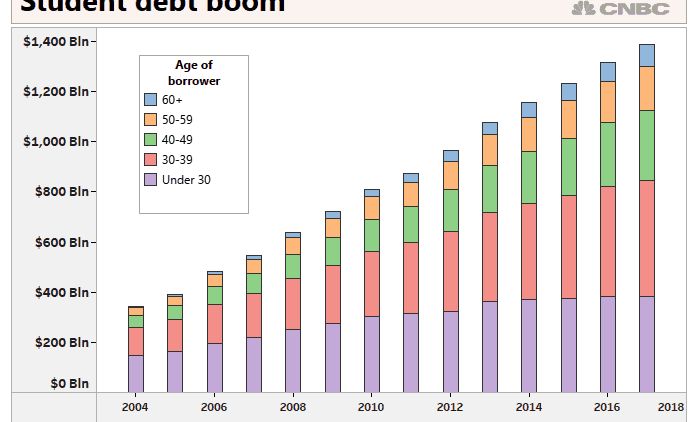

In 2019, more than 44 million Americans collectively owe $1.5 trillion in student loans. Surpassing credit cards and auto loans, student debt is now the second highest consumer debt category, behind only home mortgages. What’s more, 11.4 percent of student … Continue reading →

The majority of American voters give a thumbs up to Democratic presidential candidate Elizabeth Warren’s plan to cancel student debt. In a new Politico/Morning Consult poll, 56% of registered voters said they support the Massachusetts senator’s proposal to wipe out … Continue reading →

If you don’t have any cash on you, walking by an ATM without enough money in your bank account to cover a withdrawal can be frustrating

Many credit cards, however, can be used to withdraw cash from an ATM, whether it’s your bank or not. Just like that, you can have some money in your pocket.

But don’t jump up to the first ATM you see and take out some cash with your credit card just yet. Called cash advances, these withdrawals are actually you borrowing cash on your credit card and must be repaid — usually with high fees and interest rates.

Short-term problems of cash advances

Fees are the first thing you’ll pay on a cash advance. They’re usually based on the amount of cash you borrow, such as $10 or 5 percent of the amount, whichever is greater. That equates to a $10 fee for borrowing up to $200, or 5 percent of the amount borrowed if it’s more than $200.

Immediate interest charges are another reason to avoid cash advances. They don’t have grace periods — as your normal credit card purchases do for about a month— and the credit card company will start charging you interest on a cash advance as soon as you borrow the cash.

Cash advances have high APRs that are much higher than normal purchases. Expect to pay 25 percent interest on a cash advance, again, without a grace period.

Long-term problems

High interest rates can turn into long-term problems if you don’t pay the cash advance off soon, but there are also other problems with cash advances that can follow you for years.

The first is that your credit card company may flag you as a risky borrower. Creditors consider people who use cash advances as being desperate for money, especially if they do a few of them.

Such risky behavior with your money can lead to you being unable to get higher lines of credit or good terms with the bank that gave you the cash advance. Your credit card’s interest rate could rise or your account closed.

A second long-term problem is that cash advances add to your credit card debt and is shown on your credit reports. If you already have high balances on your credit cards when compared to your total available credit, a cash advance can lower it more.

The more credit card debt you have compared to your total available credit — called credit utilization — the more it can hurt your credit scores. If you already have high balances on your credit cards, a cash advance can make raise your credit utilization rate and make you a bigger risk to creditors.

The higher the credit utilization rate, the greater the risk that you’ll default on a credit account within the next two years, according to FICO, a credit scoring company.

“Amounts owed” make up 30 percent of a credit score, and using more than 20 percent of the credit available to you is considered risky.

‘OK, but how do I get a cash advance?’

If the problems listed above haven’t dissuaded you, and you still want to get a cash advance on your credit card, you first need to check that your credit card will work in an ATM.

Either call your credit card company or check the cardholder agreement that came with your card. Look for the sections on “Cash Advance APR” and “Cash Advance Fee,” which if listed with dollar figures or percentages charged are a sign that you card can be used at an ATM.

Your credit card statement may list a cash advance credit line or cash advance credit limit, which is the maximum amount of cash you can take out. The credit limit for cash advances is usually smaller than your credit limit for regular purchases.

To use your credit card at an ATM, you’ll need to find or set the PIN that’s tied to your credit card. You may have gotten it when the card came in the mail. You may have to request it from the credit card issuer by logging into your account online or calling the phone number on the back of the card. It might take seven to 10 days to set up the PIN.

You may get charged a fee for using an ATM that is outside the network linked to the credit card. Check with your credit card provider or your bank to find out how much it is and if you can avoid it.

How to avoid some cash advance fees

Interest charges on cash advances are unavoidable, but some fees can be eliminated through a few options.

If you have a credit card from Discover, it allows up to $120 to be borrowed in cash at checkout when you’re buying something. The money is categorized as a purchase instead of a cash advance, so you’ll avoid bank and transaction fees.

Your regular APR applies to the cash you get and there are no hidden fees, according to Discover. Called “Cash Over,” the transactions are limited to $120 every 24 hours with no monthly limit, though your local store may have allow less money to be cashed out over the purchase amount and may limit the number of times you can withdraw cash.

If you’re having difficulty finding an ATM linked to your bank so you can avoid ATM fees for withdrawing cash from your checking account through a machine that isn’t part of your bank’s network, find a bank that covers ATM fees at other banks. Some brokerage accounts offer free ATM use for customers, so setting up a brokerage account may be worthwhile.

If you’re really strapped for money, consider a balance transfer credit card. It can allow you to transfer a credit card balance and then pay it off without any interest charges for a year or more.

However, there are drawbacks to the cards, and fewer credit card companies are offering them. Be aware of the terms before switching to one.

If you decide to get a cash advance through your credit card, try to pay it back as soon as you can. Interest will start accruing immediately, and having debt get out of control will only add to your cash-flow problems.

As soon as next week, the Consumer Financial Protection Bureau (CFPB) is expected to propose the first substantive regulations under the Fair Debt Collection Practices Act (FDCPA) since the law’s enactment in 1977. This rulemaking has the potential to substantially … Continue reading →

What is credit piggybacking? If you’re not sure what this strange term could possibly mean, you’re definitely not alone.

Credit piggybacking, also referred to as credit card piggybacking or piggybacking credit, is a commonly used credit-building strategy. However, many people are still unaware of how to access this strategy and use it to their advantage.

In this article, we’ll define what piggybacking for credit means and how it can help your credit.

Credit Piggybacking Definition

The general definition of credit piggybacking is building credit by becoming associated with a credit account owned by someone else. There are three main ways in which credit piggybacking can take place, which we discuss in more detail in “The Fastest Ways to Build Credit”:

Opening an account with a cosigner or guarantor is one way to piggyback on someone’s good credit.

Opening an account with a cosigner or guarantor, which is someone who promises to be responsible for the debt if the primary borrower cannot repay it. If the cosigner or guarantor has good credit, the borrower may be able to qualify for credit that they could not qualify for on their own or qualify for better terms.

Opening a joint account with another person, which means both parties have full access to the account and are both held fully responsible for the account. By opening a joint account with a partner who has good credit, a person with less-than-ideal credit may be able to open an account that they wouldn’t have qualified for on their own or get more favorable terms.

Becoming an authorized user for the purpose of credit card piggybacking, meaning you are not responsible for the debt, but the entire history of that account may be reflected in your credit file, regardless of when you were added.

When people talk about piggybacking credit, they are usually referring to authorized user piggybacking.

How Does Authorized User Piggybacking Work?

Here’s how piggybacking works as an authorized user:

When you are added as an authorized user to someone’s credit card, often (depending on the bank), the full history of that account will then be shown in your credit report, regardless of when you were added to the card.

Therefore, piggybacking can almost instantly add years of perfect payment history to the authorized user’s credit file.

Authorized user tradelines can affect many important credit variables, such as your average age of accounts, age of oldest account, overall utilization ratio, number of accounts, mix of accounts, and more.

Historically, only the wealthy and privileged were able to use piggybacking as a credit-building strategy. Now, there is a marketplace where tradelines can be bought and sold, which is helping to democratize the credit system and provide equal credit opportunity.

The issue of piggybacking went all the way to Congress, which upheld consumers’ rights to use authorized user tradelines.

Is Piggybacking Credit Legal?

While Tradeline Supply Company, LLC does not provide legal advice, we can provide evidence that supports the idea that piggybacking credit is legal.

Firstly, piggybacking for credit is an extremely common practice that has been in use since the advent of credit cards. Studies estimate that 20-30% of Americans that have credit records have authorized user accounts in their credit file.

In addition, about 25% of people who have credit reports initially established their credit files by piggybacking in one way or another.

Many banks actually encourage consumers to add authorized users for the express purpose of boosting their credit scores.

You may have heard about FICO trying to take away authorized user privileges in 2008. But what you probably didn’t hear about was FICO backing down after a congressional hearing that involved the Federal Trade Commission and Federal Reserve Board.

During the hearing, FICO admitted that they could not legally discriminate between spousal AUs and other users, because this would unlawfully violate the Equal Credit Opportunity Act.

Since the U.S. Congress has upheld consumers’ rights to use authorized user tradelines, it seems reasonable to conclude that authorized user tradelines are legal.

As we discussed in “Do Tradelines Still Work in 2019?”, credit piggybacking still works, and we think it will be around for a long time.

Piggybacking credit is a well-established credit-building strategy that has been defended in Congress and promoted by banks. It is a significant part of our credit system.

Thanks to the Equal Opportunity Credit Act, authorized user tradelines are still a very important factor in credit scoring models.

Not only that, but even if FICO were to devise an algorithm intended to exclude piggybackers, it would be quite some time before lenders could implement it on a large scale. The slow-moving financial industry is still using FICO scores that were developed decades ago.

Piggybacking companies bring together buyers and sellers of authorized user tradelines.

What Do Piggybacking Companies Do?

Piggybacking companies, more commonly referred to as tradeline companies, simply facilitate the buying and selling of authorized user tradelines.

The tradeline companies act as an intermediary by marketing the tradelines, protecting the identities of the clients, and preventing fraud.

At Tradeline Supply Company, LLC, we provide an innovative platform through which users can buy and sell tradelines entirely online. We also provide educational resources so consumers can familiarize themselves with the credit system and how piggybacking works.

Can Piggybacking Hurt Credit?

If credit piggybacking is done incorrectly, it can backfire and hurt your credit.

Because the full history of the credit account is reflected in the credit file of the piggybacker, that means any negative factors will show up, too.

For example, if the account has any late or missed payments, that could hurt the authorized user rather than help. Similarly, high utilization on the account could also damage the authorized user’s credit.

That’s why we recommend going with a reputable piggybacking company who guarantees perfect payment history and low utilization (15% or lower) on all tradelines. This will virtually eliminate the risk of your credit being hurt by these factors.

The only other way piggybacking could hurt your credit is if you choose the wrong piggybacking credit card. It’s essential to choose the right tradelines for your credit file. To do this, you’ll need to figure out your average age of accounts and how adding a tradeline could affect this statistic.

For example, if your average age of accounts is 5 years and you decide to piggyback on a 2-year-old tradeline, this would bring down your average age of accounts, which isn’t a good thing.

Beacon Journal/Ohio.com Wednesday May 1, 2019 at 1:18 PM May 1, 2019 at 1:18 PM Alliance Data Systems Inc. has given the state of Ohio 60 days notice that it is permanently laying off 150 Akron workers who previously worked for Signet Jewelers. The Columbus-based subsidiary of Alliance Data filed … Continue reading →

What’s your credit card balance right now? If it’s zero, congratulations! You aren’t contributing to America’s record $870 billion in outstanding credit card balances. According to Q4 2018 data from the Federal Reserve, we have just over $1.05 trillion in … Continue reading →

When you apply for a personal loan, your credit report is often studied by the lender to assess your creditworthiness and understand how good you’ve been at managing credit in the past. Many financial technology companies currently active in the … Continue reading →