Debt Collector Predicts Payment Outcomes with TIBCO Data Science By TIBCO Software on 2019 – 05 – 30 Debt collection is challenging. You need to balance from getting customers to pay up with the space to make money and maximize … Continue reading →

Rep. Anna Eshoo, D-Calif., speaks at a news conference on Capitol Hill in Washington, Wednesday, May 16, 2018Photo: Andrew Harnik / AP On Tuesday, members of the Communications and Technology Subcommittee unanimously approved several amendments to a popular House anti-robocall … Continue reading →

Kelly Gooch – Tuesday, June 25th, 2019 Print | Email Recovering bad debt is a monthslong process for many medical practices, according to a new survey. TSYS, a global payments company that serves 800,000 merchants nationwide, surveyed about 640 patients and … Continue reading →

What is the difference between your overall credit utilization ratio and individual utilization ratios and why does it matter to your credit? Keep reading to find out.

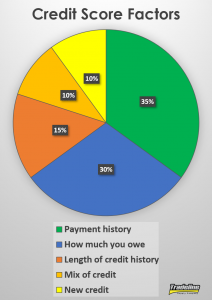

Credit utilization makes up 30% of a FICO score.

What Is Credit Utilization?

To put it simply, credit utilization is the amount of debt you owe compared to the amount of your available credit. In other words, it is the amount of your available credit that you are actually using.

In terms of your credit score, credit utilization makes up 30% of your score, second only to payment history.

The reason credit utilization is such an important part of your credit score is that the ratio of debt someone has is highly indicative of whether they will default on a debt in the future. The more you owe, the harder it becomes to pay off all that debt on time every month, which makes you a riskier bet for lenders.

Components of Credit Utilization

According to FICO, there are several components that fall within the category of credit utilization, such as:

The total amount you owe on all accounts (overall utilization)

The amount you owe on different types of accounts

The utilization ratios of each of your revolving credit accounts (individual utilization)

The number or ratio of your accounts that have high balances

The amount of debt you still owe on your installment loans (e.g. mortgages, auto loans, student loans)

What Is the Difference Between Overall and Individual Utilization?

Your overall utilization ratio is the amount of revolving debt you have divided by your total available revolving credit.

For example, if you have one credit card with a $450 balance and a $500 limit and a second credit card with a $550 balance and a $3,500 limit, your overall utilization ratio would be 25% ($1,000 owed divided by $4,000 available credit).

However, the individual utilization ratios of your respective credit cards are 90% ($450 balance / $500 credit limit) and 16% ($550 balance / $3,500 credit limit).

Since credit scores consider individual utilization ratios, not just overall utilization, having any single revolving account at 90% utilization is going to weigh negatively on the credit utilization portion of your score.

Overall Utilization May Not Be as Important as You Think

Typically, when people think of the effect that credit utilization has on credit scores, they often assume that overall utilization is the most important variable.

By this assumption, it would be fine to have individual accounts that are maxed out as long as the overall utilization is still low.

Individual utilization ratios may be more important than the overall utilization ratio.

However, we have seen that this is not always true.

For example, sometimes clients with maxed-out credit cards will buy high-limit tradelines in order to reduce their overall utilization ratio, but then they don’t see the results they were hoping for.

This means that the individual accounts with high utilization are still weighing heavily on the clients’ credit scores, despite the fact that they have improved their overall utilization. In other words, the decrease in the overall utilization ratio did not make much of a difference.

Cases like this seem to indicate that overall utilization may not play as big a role as traditional wisdom has led us to believe and that the individual utilization ratios may be more important.

Although the age of a tradeline is often its most valuable asset, tradelines can still help with some of the credit utilization variables.

Since our tradelines are guaranteed to have utilization ratios that are at or below 15%, this means that at least 85% of that tradeline’s credit limit is going toward your available credit, which helps to lower your overall utilization ratio.

Buying tradelines also allows you to add accounts with low individual utilization to your credit file, which can help to improve the number of accounts that are low-utilization vs. high-utilization.

Tips to Keep Your Credit Utilization Low

Spead out your charges between different cards

Since we have seen that it’s important to keep individual utilization ratios low, one strategy to accomplish this is to make charges on a few different credit cards instead of charging everything to one card. Spreading out your charges prevents an excessively high balance from accumulating on any one individual card.

If you spend a lot on one of your cards, consider spreading out your charges between different cards or paying down the balance more often.

Pay off your balances more frequently

If you do spend a lot on one card, it helps to pay off your balance more than once a month. If your card reports to the credit bureaus before you have paid off your balance, it will show a higher utilization than if you had paid some or all of the balance down already.

You can either time your payment to post just before the reporting date of your card or you can make payments several times per month. Some people even prefer to pay off each charge immediately so their card never shows a significant balance.

Set up balance alerts to monitor your spending

To prevent mindless spending from getting out of control, try setting up balance alerts on your credit card. Your bank will automatically notify you when the balance exceeds an amount of your choosing, so you can back off of spending on that card or pay down your balance.

Don’t close old accounts

Even if you don’t use some of your old credit cards anymore, it’s often a good idea to keep the accounts open so they can continue to play a positive role in your overall utilization ratio and the number of accounts that have low utilization vs. high utilization.

Ask for credit limit increases

Another way to decrease your utilization ratios is to call your credit card issuers and ask them to increase your credit limit. By increasing your amount of available credit, you decrease your utilization ratio, both on individual cards and overall.

Keep in mind that your bank may do a hard pull on your credit to decide whether or not to grant your request, which could ding your score a few points temporarily. However, the small negative impact of the inquiry could be offset by the benefit of the credit line increase.

Also, this might not be an ideal strategy if you think you will be tempted to use the new credit available to you.

Open a new credit card

Like asking for a higher credit limit, opening a new credit card can also lower your credit utilization, provided you leave most of the credit available.

Again, this will add an inquiry to your credit report, as well as decrease your average age of accounts, so this could have a negative impact on your score temporarily, which may be outweighed by the decrease in your credit utilization.

ALBANY – Seven people from Maryland face charges in Albany, accused of stealing protected personal employment information from government computers, federal prosecutors said. The scheme involved impersonating the debtors in order to gain information that the group would then sell … Continue reading →

Consumer Payment Card News U.S. consumer credit card losses are rising no matter how you slice or dice it, reflected by all indices. In the face of a strong economy, bubbling U.S. consumer confidence may have induced cardholders to … Continue reading →

Attorney generals from 47 states, the District of Columbia and three U.S. territories have asked Secretary of Education Betsy DeVos to forgive disabled veterans’ student loans. In a letter sent to the Department of Education head days before the Memorial … Continue reading →

In 2009 the U.S. Congress passed, and President Obama signed into law, the Credit Card Accountability, Responsibility, and Disclosure Act of 2009. This law, which is more commonly referred to as the CARD Act, restricts credit card issuers from extending credit to consumers who are under 21 years of age, except under limited conditions. The impact of the CARD Act, among other things, has made it harder for young people to build credit reports and establish credit scores.

Some experts suggest getting a co-signer to build credit, but an authorized user account may be a better option.

This is just one example of the difficulties various segments of our population endure when they are trying to build or rebuild their credit reports. Certainly people over 21 who have experienced their own credit disasters have their own unique hurdles with which to deal when trying to build or rebuild their credit reports.

It’s not uncommon for financial experts to advise consumers to look for co-signers, open secured credit cards, or take out credit-builder loans as various strategies to build or rebuild their credit. All of these credit-building strategies have their own respective pros and cons. Some work better than others, some work faster than others, and some are just bad ideas.

The “Authorized User Strategy”

One common method for building credit reports and credit scores is to become an authorized user on a credit card account that belongs to another consumer. The way it works is fairly simple. The primary cardholder adds the new consumer’s personal information to their account and “authorizes” them to use the credit line. The newly added authorized user has the same permissions to use the card as the primary cardholder but has no liability for the debt. Think of it as a credit card but with training wheels.

Most credit card issuers will then report the history of the credit card account to the authorized user’s credit reports at Equifax, Experian, and TransUnion. The addition of the credit card helps to build or rebuild the credit reports of the authorized user.

The Impact of Authorized User Tradelines on Credit Scores

Credit scoring systems, such as those built by FICO and VantageScore Solutions, will consider the newly added credit card account the next time the authorized user’s score/s are calculated. And, if the credit card account has been managed properly, it can certainly help to improve the consumer’s scores almost immediately.

To the extent you are thinking of becoming an authorized user on the credit card of another person, you should first learn a little bit about the card and how it has been managed. You’re going to want to find out the age of the card, and the older it is the better it will be for your credit scores.

You’re going to want to find out the credit limit of the card and also its average monthly balance. This is important because credit scoring models will penalize you if the balance represents too much of the credit limit. This is formally referred to as the card’s “revolving utilization ratio” and it is calculated by dividing the card’s balance by the card’s limit, as they appear on your credit reports. The lower the ratio, the better for your scores.

And finally, it should go without saying that you’re going to want to ensure the card has always been paid on time and there is no record of late payments associated with the account. Late payments, of course, are not good for your credit scores.

In the perfect scenario, you’d like to become an authorized user on a card that is decades old, has a very high credit limit, a low balance, and has always been paid on time. This the optimal account to have on your credit reports and it is a fantastic way to build your credit reports and credit scores.

John Ulzheimer is a nationally recognized expert on credit reporting, credit scoring and identity theft. He is the President of The Ulzheimer Group and the author of four books about consumer credit. Formerly of FICO, Equifax and Credit.com, John is the only recognized credit expert who actually comes from the credit industry. He has 27+ years of experience in the consumer credit industry, has served as a credit expert witness in more than 370 lawsuits, and has been qualified to testify in both Federal and State courts on the topic of consumer credit. John serves as a guest lecturer at The University of Georgia and Emory University’s School of Law.

Disclaimer: The views and opinions expressed in this article are those of the author John Ulzheimer and do not necessarily reflect the official policy or position of Tradeline Supply Company.

On June 14, the Texas governor signed HB 996, which prohibits debt buyers from commencing an action against or initiating arbitration with a consumer for the purpose of collecting a consumer debt after the statute of limitations (SOL) has expired. … Continue reading →

That credit or debit card in your wallet is apparently dirtier than you might have suspected. Continue Reading Below A recent study by LendEDU.com showed credit and debit cards were dirtier on average than cash or coins. The financial website released its … Continue reading →