The bureau further said the company broke a second law — the Consumer Financial Protection Act — when it charged debtors without settling their debts. The agency alleged that Freedom charged fees — sometimes thousands of dollars — even when … Continue reading →

BOSTON (WWLP) – A so-called ‘student loan bill of rights’ could give college students more support when it comes to paying off their debt. Longmeadow State Senator Eric Lesser filed the bill to establish a position within the attorney generals … Continue reading →

Operators allegedly bilked consumers out of more than $23 million The Federal Trade Commission has stopped a student loan debt relief scheme, alleging it bilked more than $23 million from thousands of consumers with false claims that it would service … Continue reading →

“Confirmed Judges, Confirmed Fears” is a blog series documenting the harmful impact of President Trump’s judges on Americans’ rights and liberties. Trump 7th Circuit judge Amy Coney Barrett wrote an opinion in Casillas v. Madison Ave. Associates Inc. ruling that … Continue reading →

Waring Abbott | Getty JPMorgan Chase is trying to make it harder for its credit card customers to sue the bank in court by requiring them to go into private arbitration to settle disputes. The opportunity for JPMorgan Chase credit … Continue reading →

In 2007, Congress enacted the Public Service Loan Forgiveness Program. Signed into law by then President George W. Bush, the policy was intended to help public employees—teachers, nurses, police officers, firefighters, and more—manage their student debt in the face of … Continue reading →

Students in Virginia are struggling less with post-graduation debt than in most other states, according to a study conducted by the financial website WalletHub. “Virginia is the 13th state with the least student debt,” WalletHub analyst Jill Gonzalez told The … Continue reading →

The tradeline industry is full of rumors, myths, and inaccuracies. Since we aim to educate consumers on how tradelines work and how the credit system works, we want to dispell some of these common myths about tradelines.

The Equal Credit Opportunity Act prohibits credit discrimination and helps protect authorized users tradelines.

1. Tradelines Are Illegal

Unfortunately, many people immediately discount the idea of using tradelines because they believe the pervasive myth that tradelines are illegal.

The reason this myth exists is that FICO stated in 2008 that the FICO 9 credit score would eliminate the benefits of authorized user tradelines for credit piggybackers by somehow distinguishing between “real” authorized users and those who just want to use AU tradelines to build their credit profile.

However, the Equal Credit Opportunity Act (ECOA) prevents this kind of credit discrimination, and FICO admitted to Congress that this action would illegally violate ECOA. Thus, FICO was forced to reverse its decision.

It seems that many people assumed that since the issue of tradelines went all the way to Congress, they must have been banned, but that is not the case. To the contrary, Congress actually protected the ability of consumers to use authorized user tradelines.

As further evidence that tradelines are legal, the banks themselves actually promote the practice of becoming an authorized user for the specific purpose of boosting your credit score.

2. Tradelines Don’t Work Anymore

This is another myth that arose out of the FICO controversy in 2008. Since FICO claimed that their new credit scoring model would be able to differentiate between traditional authorized users and those trying to “game the system,” many people assumed that this meant AU tradelines wouldn’t work anymore.

However, as we discussed above, FICO was not legally able to go through with this plan, which means anyone can still take advantage of the benefits of user tradelines.

ECOA protects authorized users from being discriminated against, so AU tradelines are here to stay.

Plus, even if FICO does manage to come out with a score designed to punish piggybackers in the future, it will likely take years or even decades for lenders to start using the new score.

Some people think that it is unethical to buy or sell tradelines because they believe that people who buy tradelines are artificially boosting their credit score and can therefore obtain credit that they are not really qualified for.

Firstly, is it unethical to try to boost one’s credit score using legally allowable methods?

People take actions to boost their credit scores every day, such as asking for credit limit increases, taking out new loans to establish more lines of credit, asking their banks to forgive late payments, paying down credit card balances multiple times a month to keep the utilization low, just to name a few.

Becoming an authorized user for the purpose of building credit is just one of many common methods that people use to try to improve their credit.

You have probably even tried several of these techniques yourself. Therefore, it seems that the majority of people do not believe that it is unethical to manipulate credit scores within the legal limits of the law.

In addition, studies have shown that about a third of people have authorized user accounts in their credit profiles and that those authorized user accounts tend to be superior tradelines to the primary accounts in their own name, which means about a third of people are already benefiting from credit piggybacking.

However, minorities have fewer authorized user accounts and benefited less from them compared to whites.

Creating a marketplace where affordable tradelines can be bought and sold helps to create more equal credit opportunity for those who have historically been disadvantaged by an unfair system.

One of the common complaints about tradelines is that they are expensive. Historically, tradelines were only available to the wealthy and privileged due to their high cost.

That may still be true for a lot of tradeline companies, but Tradeline Supply Company, LLC has been a leader in revolutionizing the tradeline industry and making tradelines affordable for everyone.

Our fully automated online platform allows us to keep costs down and provide fairly priced tradelines to consumers.

Our tradelines range in price from as low as $150 to around $1500. Our inventory of thousands of tradelines means virtually everyone can find tradelines that fit their needs as well as their budget.

We have also helped contribute to lower pricing in the industry as a whole. Other companies have started to follow our lead and lower their prices to stay competitive.

All of this means that tradelines are now more affordable than ever.

5. Primary Tradelines Are Better Than Authorized User Tradelines

People often assume that primary tradelines are superior to authorized user tradelines. They think that since authorized users are not held financially responsible for a credit account, primary tradelines must be more powerful, but this belief is somewhat misguided.

When it comes to building credit, the ultimate goal is to open your own primary accounts and maintain a positive history on those accounts, so in this sense, primary tradelines are the priority.

However, when it comes to buying tradelines, trying to buy a primary tradeline is generally not a good idea. Firstly, the primary tradeline industry is full of scams and questionable practices, some of which may even be illegal.

If you think about it, it doesn’t really make sense to try to “buy” a credit account that, by definition, is supposed to have been issued to you by the creditor. If the account was not issued to you, that means someone else had to have opened that account in their name at some point, so how does it then become your primary tradeline?

Secondly, purchasing a primary tradeline may not even help achieve your goals as much as you might think. A legitimate primary tradeline will have no age and no payment history associated with it and will probably have a low limit as well.

In contrast, you can legitimately purchase authorized user tradelines that have lots of age and perfect payment history in addition to high credit limits.

Which option do you think would be better for your credit: the brand-new account with a low limit, or a seasoned AU tradeline with a high limit? In general, the seasoned authorized user tradeline is going to be the better choice.

An easy way to think about the distinction between tradelines and credit repair is that tradelines add positive information to your credit report, while credit repair removes inaccurate information from your credit report.

If your credit report has damaging errors on it that are lowering your score, any tradelines you add will be limited in their power. For this reason, you may want to undergo credit repair before or in tandem with tradelines.

Similarly, tradelines should not be used as a substitute for credit repair. While they can help to balance out derogatory accounts, this is not the same thing as cleaning up errors in your credit report.

7. Authorized User Tradelines Do Not Count for Mortgages or Auto Loans

For the majority of the most common mortgages, there is no minimum tradeline requirement.

We do not advertise our tradelines saying if you buy our tradelines you can then qualify for a mortgage or auto loan. However, we have done some research and we have found that for the majority of the most common mortgages (most conventional, FHA, and VA loans) there is no minimum tradeline requirement in order to qualify for those loans.

In other words, someone can have zero tradelines and could still potentially be qualified to buy a house. The main factors will typically be the debt-to-income ratio, loan-to-value ratio, and credit score.

Fannie Mae typically updates their underwriting guidelines in regards to authorized user tradelines on their website.

We have heard there are similar guidelines for auto loans as well. Again, we are not claiming that buying tradelines can help someone buy houses or cars, but we are simply addressing this common myth.

8. I Can’t Get Tradelines That Were Opened Before My 18th Birthday

Some people believe that you cannot or should not buy tradelines that were opened before you turned 18 years old. The theory seems to be that it would look suspicious if you were to have an authorized user tradeline while under the age of 18, so somehow the tradeline wouldn’t count toward your credit history.

Contrary to this myth, you do not have to buy tradelines that were opened after your 18th birthday.

In reality, there are many examples to show that this is not true. Parents often add their children as authorized users of their credit cards well before age 18, whether they allow their children to actually use the credit cards or they just want to help their children build a credit history from a young age.

Imagine this hypothetical example: let’s say you are 16 years old. Your father has a credit card that has been open for 20 years. He wants you to be able to use the credit card in case of emergencies, so he adds you as an authorized user to his 20-year-old account. In this case, the tradeline actually extends back to before you were born, but that does not prohibit you from being an authorized user on the account.

Of course, there may be exceptions to this rule, since different banks may have different policies as to the minimum age of authorized users.

However, if you are over the age of 18 and buying tradelines, it should not matter how old the tradeline is.

9. Tradelines Are Only a Temporary Solution

Although tradelines usually only report as open for two months, they remain on your credit report as part of your permanent credit history.

While it is true that a tradeline will typically only report as an open account on your credit report for two reporting cycles, this does not mean that tradelines are only a temporary solution.

Once you are removed from the tradeline, the account will then show as closed, and the closed account will remain on your credit report as part of your permanent credit history for as long as the bank continues to report it.

Although closed accounts are assumed to weigh less on your credit score than open accounts, since the closed tradeline is still a part of your credit history, it will likely still factor into your credit score.

This is because age goes hand-in-hand with payment history, together making up 50% of a credit score. When it comes to the length of your credit history, more is always better.

11. Buying a Tradeline Guarantees a Score Increase

Those looking to improve their credit score sometimes mistakenly assume that they can go out and buy any tradeline and get a guaranteed credit score boost. This is a dangerous myth because if buyers are not educated and choose the wrong tradeline for their specific credit situation, buying a tradeline could actually backfire and hurt their credit.

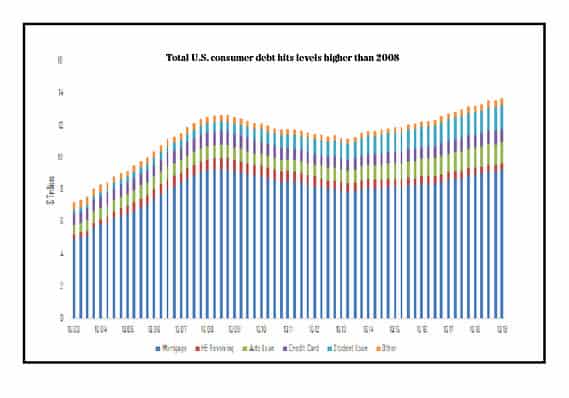

Consumer debt is growing to worrisome levels. Ben Mohr, senior research analyst of fixed income at investment consultant Marquette Associates, calculated that total U.S. consumer debt hit $14 trillion in the first quarter of 2019, surpassing the roughly $13 trillion … Continue reading →

I thought I would share one of our heartfelt stories of a past client of ours. I will not mention the name, but this story is what gives me meaning for what I do.

I received a call and the gentleman proceeded to tell me about his story. He explained that when he was young, his parents never taught him about money, credit, or how to handle finances. He said his parents were very poor and did not teach him how important these topics were.

As this gentleman went through life, he did not have much in terms of financial accomplishments. He worked hard all his life, had a stable job, and was blessed with a daughter who was now graduating high school and had dreams of going to college.

His daughter recently started her first job and became a young adult who was being thrust into “the real world.” Over the years, her father had eventually become financially stable and had been studying ways to help his daughter succeed and navigate through life better than he did.

He began going to numerous banks’ websites and reading about Parent Plus Loans to help his daughter pay for college. He read about how to help his daughter get student credit cards and about “teaching kids about credit.”

He did much of this research directly on the big banks’ websites, thinking that since they are the source of the money, maybe these banks can provide some valuable ideas and options.

In the course of his research on the numerous national bank’s websites, he also began reading what they wrote about the benefits of adding one’s kids to their credit cards as authorized users. According to the banks, this would help them get a head start in building their own credit.

To this man’s surprise, there were numerous articles written about the topic. He began going to all the major bank’s websites and typing in “authorized user” and would read everything they had published on the topic which enlightened him on the strategy of credit piggybacking.

The gentleman described his feeling of hope in learning about such a powerful option, yet he also felt an overwhelming sense of despair knowing that he was not in a position to be able to help his daughter, unlike some of the other more financially savvy parents.

He said it was difficult to find the right words to describe his feeling of hope and despair that existed at the same time. He said that all he could do was pray for a solution.

After several days passed, he had nearly given up on this idea to help his daughter. He decided to go back to his computer and search for “authorized user” one last time, except this time using his primary search engine instead of going directly to a bank’s website. As he searched, his screen filled up with businesses advertising tradelines for sale.

The client decided to purchase tradelines for his daughter as a graduation gift.

He had no idea what tradelines were, so he started reading numerous websites that talked about them and even offered them for purchase. He felt that the answer to his prayers had been delivered.

He wanted to buy a tradeline for his daughter as one of her high school graduation presents. After much research and comparison, he decided to purchase a tradeline for his daughter though Tradeline Supply Company, LLC.

When he called us, he explained how he wanted to be able to do something for his daughter that his parents were not able to do for him.

He told me about his whole journey of learning about authorized user benefits but then becoming depressed knowing that his credit was not good enough to help his daughter. While he knew that it was not his fault that his parents and teachers never taught him the importance of having credit, he still felt guilty that he could not provide this financial advantage to his daughter that more privileged parents are often able to provide.

He said that finding out about our company was literally the answer to his prayers. He ended up buying two tradelines for his daughter and every now and then he gives me updates on how she is doing.

His emotional story almost brings tears to my eyes because he is so appreciative of what I do and how I was able to help him and his daughter. He always felt that growing up in a family of low socioeconomic status was such a disadvantage, and he wanted to do anything he could to give his daughter a fair shot at succeeding in this tough world.

So Mr. _______, if you are reading this post, please know that you made my day by sharing your story and I thank you for bringing a deeper sense of meaning to my work. The appreciation that you have expressed to me is felt deep in my heart and I wish your daughter all the best in her life. You make me proud to help provide equal opportunity for all.