State Rep. Will Guzzardi, D-Chicago, speaks during a House committee meeting Feb. 6 at the Capitol in Springfield. Guzzardi was the House sponsor of a bill signed into law Monday by Gov. J.B. Pritzker that reduces the interest rate charged … Continue reading →

Debt collection firm Credit Corp has lifted full-year profit nine per cent More Debt collection firm Credit Corp has lifted full-year profit nine per cent to $70.3 million despite a slight dip in collections in Australia and New Zealand. … Continue reading →

NEW YORK, Aug. 20, 2019 /PRNewswire/ — S&P Dow Jones Indices and Experian released today data through July 2019 for the S&P/Experian Consumer Credit Default Indices. The indices represent a comprehensive measure of changes in consumer credit defaults and show that … Continue reading →

Monday, August 12, 2019 Under the Fixing America’s Surface Transportation (FAST) Act, the IRS can notify the State Department when taxpayers owe a seriously delinquent tax debt. If the IRS certifies a taxpayer’s debt as “seriously delinquent” to the State … Continue reading →

Tuesday, August 20, 2019 In a precedential opinion, the U.S. Court of Appeals for the Third Circuit concluded that a plaintiff in a class action complaint had Article III standing and was properly awarded summary judgment when a debt collector … Continue reading →

View photos This post originally appeared on The Basis Point: Household Debt—How Much Money Does Everybody Owe? Q2 2019 Edition Every quarter, the Federal Reserve Bank of New York releases data on how much household debt Americans … Continue reading →

Lawsuits filed by Glens Falls (N.Y.) Hospital against people over unpaid medical bills have led to court delays, according to The Post-Star. Glen Falls City Court Clerk Greta Guarino told the newspaper patients who answer summonses are scheduled for mediation … Continue reading →

If you have credit cards with low credit limits, you may be interested in increasing your credit limit. In this article, we’ll talk about why your credit limit is important, reasons to increase your credit limit, when and how to request a credit line increase, and more. Keep reading for everything you need to know about how to increase your credit limit.

How Does Your Credit Limit Affect Your Credit Score?

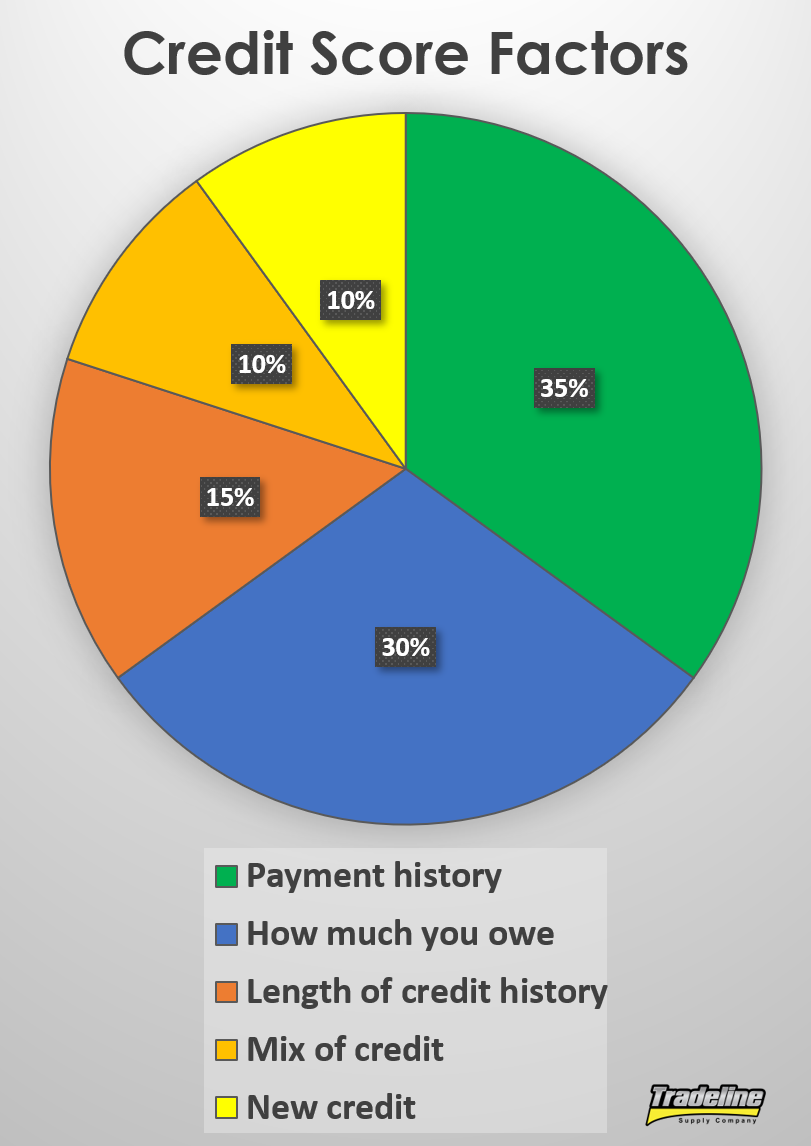

The obvious reason why you should care about your credit limit is that it controls the amount you can spend on that particular credit card. But beyond that, your credit limit also indirectly affects your credit score.

Although credit limit itself is not a factor in credit scores, it plays a role in your credit utilization ratio, which is an important part of your credit score. In fact, utilization makes up about 30% of a FICO score.

Your credit utilization ratio is the amount of debt you owe divided by your credit limit, typically expressed as a percentage. For example, if your credit card has a $10,000 credit limit and you owe $2,000 on it, your utilization on that card is 20% ($2,000 / $10,000 x 100% = 20%).

The above example is an individual utilization ratio since it is the utilization ratio of a single card. Your overall utilization ratio is similar, but it includes all of your revolving debt added together divided by the total credit limit of all of your revolving accounts. Both individual and overall utilization are accounted for in your credit score.

Why is utilization such an important part of one’s credit score? High utilization means high risk for lenders. If you are using most or all of your available credit, this indicates that you may be overextended and you might have trouble paying off your debts. Therefore, high utilization lowers your credit score because it means you are more likely to default.

Utilization (how much you owe) makes up 30% of your FICO score.

On the other hand, low utilization means you are not using very much of your available credit, which indicates to lenders that you are at low risk of defaulting. Therefore, keeping your utilization low is a good thing for your credit score.

Why Increase Your Credit Limit?

To bring this all back to your credit limit, remember that your credit limit affects your utilization ratio. Consider an example in which someone owes $500 on a $1,000 limit credit card. Their utilization is 50%, which is high enough to potentially have a negative impact on their score. But if they were to increase their credit limit to $2,000, their utilization would go down to 25% ($500 / $2,000 x 100% = 25%), which could help out their credit score.

Essentially, increasing your credit limit helps lower your utilization ratio, which can benefit your credit health.

Plus, it gives you more spending power if you ever need it to make a big purchase.

One important caveat: this strategy only works if you do not run up the balance on your credit cards. If increasing your credit limit means you will just continue to spend up to your credit limit and get in more debt, then it’s probably not a good idea.

How to Increase Your Credit Limit

There are a few different ways to go about raising your credit limit.

Wait for the credit card issuer to automatically increase your credit limit.

Lenders will often automatically bump up your credit limit after you have had the credit card after a certain amount of time, provided you have used it responsibly and paid on time every month. However, you usually have to wait several months after opening a card to be considered for a credit limit increase.

Request a credit limit increase.

If you haven’t gotten an automatic credit limit increase, you can request one. You can do this over the phone or on the credit card issuer’s website.

Generally, if you apply for a credit line increase online, this will result in a hard credit pull. However, if you call and talk to a representative, you may be able to get an increase with only a soft pull, depending on the situation.

When you request a credit line increase, you should be ready to provide your total annual household income, your employment status, and the amount of your monthly rent or mortgage payment. Credit card issuers typically state that you can include income from someone else if that person’s income is regularly used to pay your expenses.

Some lenders may ask you to explain why you need or deserve a credit line increase, so be prepared to explain the reason for your request. They may also inquire about how much you spend on credit cards each month.

When to Request a Credit Line Increase

It’s best to wait until the right time to request a credit line increase. Just like applying for a new credit card or loan, you want your credit and your income to be in good shape when you request it.

Potentially good times to request an increase:

A good time to request a credit line increase is after you get a pay raise at work.

After you receive a raise

After you have been a responsible cardholder for at least 6 months

If you have not requested an increase in at least 6 months

When you do not have many inquiries on your credit report

When your credit score is high

Situations when you might want to hold off:

If you lose your job or take a pay cut

If you have recent late payments or other derogatories

If your cards are maxed out or at high utilization

If you have only been making the minimum payments on your card

If your account is less than 6 months old

If your credit limit has changed within the past 6 months

If you have applied for multiple other credit cards or loans recently

When your credit score is low

How Much Should You Request?

There is no hard-and-fast rule when it comes to how much of an increase to ask for.

You could try calling your bank and asking the representative if there is an amount they could approve without doing a hard pull.

Another approach is to ask for more than you think you need. If the bank does not approve the full credit line increase that you asked for, they will often counter with the maximum amount that they can offer you.

Will Requesting a Credit Limit Increase Affect Your Credit Score?

Depending on the lender and the amount that you request, the credit card issuer may conduct a soft or hard inquiry on your credit. They want to see what your credit report looks like before taking the risk of granting you even more credit.

Check with your credit card issuer to see if requesting a credit limit increase will trigger a soft or hard inquiry.

Are inquiries really killing your credit? Click the image to read the article.

As we discussed in “Are Inquiries Really Killing Your Credit?” a hard pull could reduce your credit score by a few points, but it’s not the end of the world. As long as you keep your inquiries to a minimum, it shouldn’t present much of a problem. It’s when you have several recent inquiries on your credit report that you start to look like you are desperate for credit and you may get denied by lenders.

However, as we discussed earlier, the more significant potential impact to your credit score is the decrease in your utilization ratio if you do get approved for a credit line increase. Since utilization makes up about 30% of a credit score, improving that factor could benefit your score and would likely outweigh the impact resulting from a hard inquiry.

What Are the Downsides to Increasing Your Credit Limit?

Besides the impact on your credit score of potentially getting a hard inquiry, there are a few other drawbacks to consider when increasing your credit limit.

Some credit card issuers may charge sneaky fees to increase your credit limit. If you don’t want to pay a fee, make sure to check the terms of your card before requesting a credit line increase.

In addition, having access to more credit could encourage you to spend more, which could end up doing more harm than good to your credit score and to your overall financial health.

Other Ways to Increase Your Credit Limit

If you can’t get a credit line increase on an existing card, you can open a new credit card.

You don’t necessarily have to ask for a credit line increase if you want to get a higher credit limit.

Another option is to transfer some or all of your credit limit from another credit card to the card you want to extend. However, with this method, the two cards need to be from the same bank, and not all banks allow customers to do this.

If your bank does allow credit limit transfers, you could open a new credit card with them, take advantage of any signup bonuses offered, and then transfer the limit to your older card.

If transferring is not an option, opening up a new credit card with any bank will still increase your overall credit limit and utilization ratio, assuming you do not run up a balance on the card.

Have you tried requesting a credit limit increase before? Which of these methods do you plan to try next? Let us know in the comments below!

CLEVELAND, Ohio — If you’ve been drooling for Apple’s new slick titanium, laser‑etched, no-fee credit card since it was announced in March, the wait is almost over. People who signed up to get notifications when Apple Card would be available … Continue reading →

If you have credit cards with low credit limits, you may be interested in increasing your credit limit. In this article, we’ll talk about why your credit limit is important, reasons to increase your credit limit, when and how to request a credit line increase, and more. Keep reading for everything you need to know about how to increase your credit limit.

If you have credit cards with low credit limits, you may be interested in increasing your credit limit. In this article, we’ll talk about why your credit limit is important, reasons to increase your credit limit, when and how to request a credit line increase, and more. Keep reading for everything you need to know about how to increase your credit limit.