If low inflation, a wobbly economy and tariff jitters weren’t enough to push the Federal Reserve to lower interest rates, there’s also the simple reason of the swelling national debt. The recent debt deal struck between the White House and … Continue reading →

Based on the announcements in December, the parking lot of the former Telvista building should’ve been a hive of activity by now. Instead, knee-high blades of grass now poke through the cracks in the asphalt along Cane Creek Boulevard. PRA Group, … Continue reading →

Businesses these days revolve around creating the perfect customer experience. Trends and preferences change with the blink of an eye, and businesses that can’t keep up are cut out of the race. A study shows that only 80% of the businesses cross their first-year mark and around 45% to 51% of the business survive for more than five years. One of the main reasons for this may be the lack of financing for immediate business requirements.

Recently, there has been an evolution in financing structure and procedure to facilitate easy and quick loans for businesses. Today, financing for small businesses can be classified into two types – traditional financing and alternative financing.

Traditional funding is given by established institutions. A few examples of the traditional financing options available are below.

1) Bank Loans:

Most banks offer term loans, a business line of credit or equipment loans. Term loans are preferred if you need money to fulfill your immediate business needs. A lump sum amount of money is given to be repaid in a fixed time period. The bank interest rate for the amount borrowed is added to the repayable amount. With a business line of credit, you can borrow money from the bank when you want per your business requirement. The interest rate will apply only for the money you have borrowed. Equipment loans are lesser-known bank loans that can cover between 80 to 100% of your business equipment costs This type of loan is useful in most business industries especially construction and auto repair.

Bank loans are one of the hardest loans to qualify for because the average APR for bank loans is 2.24% to 4.47% . The lower the interest rate, the tougher it is to get.

2) Government Grants

Bank loans and their strict lending requirements give rise to other kinds of traditional financing options. Banks and other lending institutions will provide the loan when it’s guaranteed by the government to small businesses. Government grants are not applicable for starting a business, paying off debt or for operational expenses. To learn whether a grant applies to your small busines, visit grants.gov.

3) Investment Capitals

The Small Business Administration has an Small Business Investment Capital(SBIC) program that is powered by private equity fund managers who pool capital for small businesses. This loan is guaranteed by the government and is a win:win for both the investor and the small business owner.

Alternative financing is not cash, stocks or bonds. It is immediate capital that is provided to the business to streamline their existing processes or launch new ones. The prerequisites for acquiring these types of funding is also comparatively lenient to their traditional counterparts and varies by type.

4) Crowdfunding

The accumulation of money from various investors for a single cause or business is called crowdfunding. There are many crowdfunding platforms where you can enroll and get huge financing from multiple investors. The best part of crowdfunding is that you do not have to depend on a single person or entity to provide you with a large sum of money.

5) Invoice Factoring

In this method, the lender takes responsibility for your invoices and directly collects the money from the concerned people/business. Invoice factoring or accounts receivable factoring allows you to bring cash inflow to your business and not sit around waiting for customers to settle their invoice amounts.

6) Short Term Loans

Short term loans are one of the most common types of alternative funding where you can borrow an amount of up to $200,000 depending on your business requirements. You can repay this amount within the next 3 to 18 months but, the APR (Annual Percentage Rate) is usually higher than the traditional financing sources.

Short term loans do not need a high credit score, a business plan or even three months bank statement and the amount requested will be approved almost immediately. It’s important that you have a plan for repayment of all types of loans, especially this one since the payment terms are for a shorter amount of time and have a higher interest rate.

7) Small Business Administration (SBA) Loans

SBA loans are government aided financing options where you can get loans for your small business with interest rates like bank loans. This loan does not fund businesses directly but allows lenders to pool in money and finance your business. As this is a government-led scheme, the SBA (small business administration) covers the losses of lenders in case of failed businesses.

Running a business can be an arduous task. With all the different types of financing options presented to you, it’s up to you to choose the best ones that fit your business model and requirements.

If you are struggling with getting the funding you need because your credit isn’t up to par, reach out to an NFCC small business coach today!

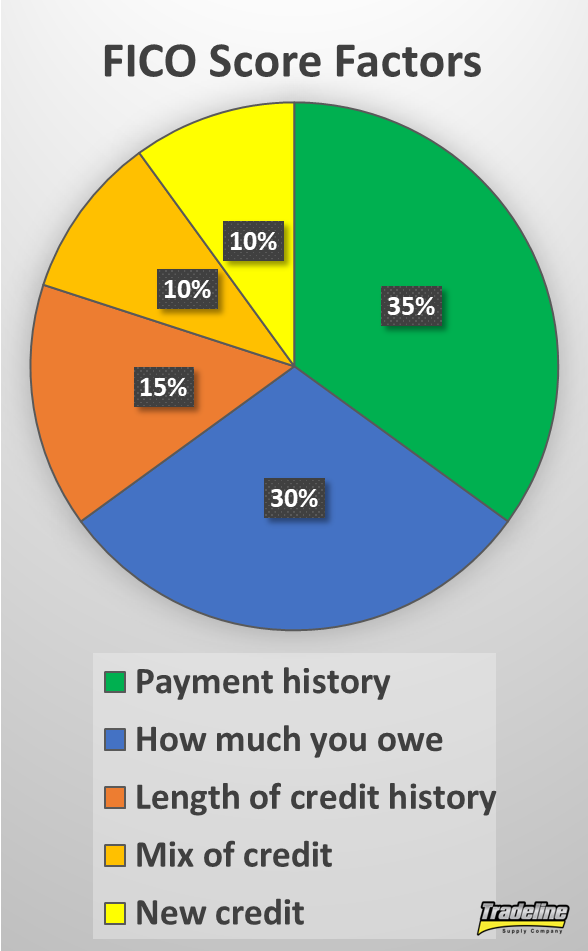

Credit mix, also called mix of credit, is one of the factors that your credit score takes into account. It is one of the least important factors, weighing in at 10% of a FICO score.

Credit mix is the diversity of types of credit accounts in your credit report. Having different types of credit accounts in good standing in your credit file demonstrates that you can use credit responsibly. Lenders ideally want to see that you have successfully managed a diverse mix of multiple types of accounts.

Types of Credit Accounts

Depending on how you define the types, there are 3-4 general categories when it comes to types of credit.

Revolving credit is a form of credit with which you can “revolve” or carry a balance each month. You are assigned a credit limit that you can charge up to and you make a payment each month. Interests will typically be charged if you carry a balance from month to month. Credit cards and lines of credit are the most common types of revolving credit accounts.

Charge cards are similar to credit cards, except the balance must be paid in full every month.

Service credit includes accounts with your service providers, such as utilities, cell phone service, etc. These are considered credit accounts because the service is provided before you pay the bill.

Installment credit is a loan of a specific amount of money that you pay back in regular payments of the same amount over a certain period of time. Types of installment loans include car loans, mortgages, student loans, etc.

Credit Karma simplifies the categories to 3 types of credit:

Revolving credit

Open credit (includes charge cards)

Installment credit

Examples of Revolving Credit

As we touched on above, the two most common types of revolving credit are credit cards and lines of credit.

Credit cards include those issued by banks such as Capital One, Bank of America, and Chase, as well as store cards, which can typically only be used at a particular retailer.

Lines of credit are similar to credit cards in that you have access to a set amount of money—your credit limit—that you can draw from. After you borrow money from your line of credit, the balance starts accruing interest, and when you pay it back, that credit is then available again for you to use. This is why it’s considered revolving credit: you can use it again and again as long as you keep paying it back.

Types of Lines of Credit

A home equity line of credit (HELOC) is secured by your home.

Lines of credit can be either secured, which means the borrower has provided collateral to back the line of credit in case of default, or unsecured, meaning no collateral is required.

Beyond those general categories, there are three main types of lines of credit.

A home equity line of credit (HELOC) is a line of credit secured by your equity in your home, which is the difference between the value of your home and the amount you still owe on your mortgage. Since your home equity serves as collateral, if you default on a HELOC, you could risk losing your home to foreclosure.

A personal line of credit is usually unsecured, although sometimes you may be able to provide collateral in the form of savings or investments.

A business line of credit may be secured or unsecured. They are offered by financial institutions as well as many commercial vendors.

Examples of Installment Loans

An auto loan is one type of installment account.

Types of installment credit include:

Auto loans

Mortgages

Student loans

Personal loans Credit-builder loans

Home equity loans (not to be confused with a HELOC, which falls under revolving credit)

The breakdown of account types outlined above is a simplified version of how credit scoring systems actually categorize different types of accounts. In reality, credit scoring models may consider as many as 75+ account types.

In addition, each type of account could have a different effect on your credit.

How Does Credit Mix Affect Your FICO Score?

As we mentioned at the top of this article, credit mix makes up about 10% of your FICO score. With VantageScore, type of credit and credit age are combined into the same category, which makes up approximately 21% of your VantageScore.

With both types of scores, credit mix is a relatively small portion of what determines a credit score, so having the perfect credit mix is not necessarily essential in order to have good credit. However, it’s still a good thing to aim for, especially if you want to get a perfect 850 credit score or somewhere close to it.

What Is a Good Credit Mix?

When it comes to your credit score, the most important thing is to demonstrate that you have managed both revolving and installment accounts. Therefore, it’s best to have at least one type of account of each type.

FICO high score achievers have an average of seven credit cards on their credit reports. Photo by Hloom on Flickr.

For example, you might have a credit card (revolving) and an auto loan (installment). Or, you could have a mortgage (installment) and a HELOC (revolving). Any combination of one revolving account and one installment account is a good start for your credit mix.

FICO supports this idea, saying, “Having credit cards and installment loans with a good credit history will raise your FICO Scores.”

FICO also says that people who have managed credit cards responsibly are better off than consumers that don’t have any credit cards, who can be seen as risky because they have not demonstrated experience in using revolving credit.

Statistics show that high FICO score achievers have an average of seven credit cards on their credit reports, which includes both open and closed accounts.

People with credit scores in the 800s also typically have installment loans such as mortgages and auto loans, according to Experian.

The total number of accounts in your file may also play a role. FICO has indicated that those with high credit scores can have 20+ credit accounts in their credit reports.

How Many Credit Cards Is Too Many?

Having too many credit card accounts could hurt your credit score.

Keep in mind that it is possible to have too many accounts on your credit file. According to the FTC, having too many credit cards could have a negative effect on your credit score, as could having loans from some types of companies.

There is no hard-and-fast rule when it comes to how many credit cards is too many because the impact of any given factor on your credit score depends on what is already in your credit profile, says FICO.

However, in figure 1 in the article “How Credit Actions Impact FICO Scores,” the hypothetical consumer “Rachel,” who has 33 credit accounts, has a lower credit score than “Maria,” who has 21 accounts. This would seem to imply that at some number between 21 and 33 accounts, one’s credit score might begin to suffer. However, these two consumers have other differences in their credit profiles, so the difference in their credit scores cannot be solely attributed to the number of accounts in their files.

Can Some Account Types Hurt Your Credit?

Certain types of loans on your credit report could make you seem like a more risky consumer and therefore could end up hurting your score instead of helping.

Why? It’s all based on statistics and who the credit score algorithms have deemed to be risky borrowers.

For example, taking out a furniture loan could actually drop your credit score. That’s because furniture loans are often reported as “consumer finance loans,” which are typically reserved for borrowers with bad credit who are statistically more likely to default on loans. Therefore, having this type of account on your credit report could be viewed as risky by lenders and credit scoring algorithms.

Alternatively, the financing arrangement may be reported as revolving debt, which will appear nearly maxed out until you make enough payments to get the balance to a lower level.

Payday and title loans, however, are typically not reported to the credit bureaus, so these types of loans won’t count toward your credit mix or credit score—unless, of course, you default on a loan and it gets sold to a collection agency, who will then report it as a collection account.

Conclusions on Credit Mix

Since credit mix makes up about 10% of your credit score, it is helpful to try to achieve a balanced mix of credit by keeping a few revolving and installment accounts in good standing. The best credit mix should ideally include a few credit cards and at least one or two installment loans, such as mortgages or auto loans.

However, it’s also important to note that credit mix is much less important than other credit score factors, such as payment history, credit utilization, and credit age. It’s probably not worth obsessing over because you won’t automatically get an excellent credit score just by having the perfect mix of accounts.

In addition, most people naturally accumulate different types of accounts over time, so it’s not necessarily the best idea to start opening new accounts left and right just to build up your credit mix. This strategy could result in lots of inquiries and new accounts bringing your score down in the short term, and having access to credit you don’t need could also encourage extra spending.

As with all credit-related decisions, it’s up to you to take your overall financial goals and priorities into account before taking action. You might decide that you don’t need to worry too much about improving your credit mix, and that’s fine. On the other hand, improving your credit mix can only help your credit score, and it is something that you should pay attention to if you want to get a perfect 850 credit score.

For the past two months, Becky Beach, an avid shopper with a low credit score, has found herself trapped in the “shop more, earn more points” game that retailers play. Beach, a 37-year-old stay-at-home mom, has been overdue on two … Continue reading →

The Trump administration is proposing reforms to the country’s mortgage-finance system. Photo: Steve Helber/Associated Press By Aaron Back Aaron Back The Wall Street Journal Biography @AaronBack [email protected] Sept. 5, 2019 6:08 pm ET America’s mortgage-finance system isn’t going to change … Continue reading →

Paul Olden walked out of prison last year with $26,000 in debt. Without knowing it, for years he racked up child support payments while he was behind bars. Olden was shocked to learn of his debt in 2012, when his grandmother … Continue reading →

Home improvements allow you to to make upgrades and add convenient features to your house. In 2018, American homeowners spent around $394 billion on improvement projects, including air conditioning and heating systems, waterproof roofs, soundproof rooms and renewable energy.

Do you want to save money for your dream renovation? Then follow the six tips below for creating a budget and sticking to it.

1. Determine Your Goals

Before you begin a renovation project, ask yourself what you hope to accomplish. Perhaps you want more counter space for appliances and dinner prep? Maybe you’d like an upgraded bathroom with a whirlpool tub and heated tiles? Once you’ve narrowed it down to one goal, determine how much you’re willing to spend.

2. Estimate the Costs

You have a goal — it might be a new patio or expanded master bedroom. Now it’s time to determine the costs. Experts say you should never spend more on a room than its value toward the home. For example, say your home is worth $200,000, and the kitchen takes up 15% of the square footage. In this case, you wouldn’t want to spend more than $30,000 on a kitchen remodel.

3. Account for Hidden Fees

You never know how much a renovation will cost until you start digging. Sure, your home looks perfect on the outside. However, it’s not uncommon for a remodel project to dig up hidden issues, whether beneath floorboards or under wallpaper. Plan for these expected fees by cushioning your budget with an additional 10-20%.

4. Understand Cost vs. Gain

You’ve probably heard the saying, “You need to spend money to make money.” The same is true when it comes to remodeling your home. The added value often outweighs the cost of upgrades and improvements. If you’re ever planning on selling your home, the added return on valued renovations can help with your budget down the line.

This is a personal decision, as only the homeowner can know which changes they’ll value most. But if you’re tempted to spend less in the moment, you may be reducing the chance to earn on long-term gains. As a general rule, opt for renovations with timeless appeal, including hardwood flooring, mid-range kitchen upgrades and bathroom accessibility changes.

5. Limit Your Wants

When you first start a new project, you might feel the urge to splurge. It may seem like you have plenty of funds for fixtures and finishes, only a small fraction of the entire budget. As the project continues, though, you’ll begin to see the money slowly disappear. It’s OK to make a few sacrifices for something you want, but it’s necessary to limit your wants to save for potential setbacks.

6. Assess Financing Options

Most people can’t cover all remodeling expenses with cash. In this case, you’ll have to borrow to finish the project. One option is a home-equity line of credit, which allows you to borrow money — up to a certain amount— when needed. Another choice is a home equity loan, where you apply for a lump sum up front and repay at a fixed interest rate in monthly installments.

Are you planning a home improvement project? Save money the easy way by creating a budget. Determine your No. 1 goal and come up with the estimated costs. Don’t forget about hidden fees and think about the value of the upgrade once complete. If you don’t have enough cash on hand to cover a remodel, consider convenient financing options to fund the changes you’re dreaming of.

(WBNG) — Hundreds of Sidney Federal Credit Union customers are asking for answers after a wave of fraudulent charges appeared on bank accounts over Labor Day weekend. The charges, stem from a single ATM at the SFCU Walton branch. According … Continue reading →

Attorney General Phil Weiser filed a “friend of the court” brief Tuesday, backing Pennsylvania in its efforts to sue student loan service giant Navient, alleging unfair and deceptive practices. Colorado becomes the 32nd jurisdiction to join in the amicus brief … Continue reading →