Enlarge this image Carrie Barrett, a former defendant in a suit brought by Methodist Hospital, testifies during service at Apostolic Fellowship Church on Sept. 15, 2019 in Memphis, Tenn. Her debt to the hospital was cleared following a MLK50 and … Continue reading →

I was speaking to a consumer group recently and the topic of credit repair came up as a discussion point. I fielded questions about whether or not credit repair is legal, how to identify good credit repair companies, and whether the process of traditional credit repair is better or worse than adding tradelines to your credit reports. It occurred to me that there was a considerable disconnect between what is traditional or garden-variety credit repair versus adding tradelines to your credit reports, thus the purpose of this writing.

Traditional Credit Repair

While I have no dog in the fight between credit repair companies and the tradeline industry, it appears some credit repair companies misrepresent their services. Credit repair is often positioned as a way to get inaccurate or unverifiable information removed from your credit reports. It appears, however, that traditional credit repair is built more around getting negative information removed from your credit reports, whether it is accurate, verifiable, or not.

Some credit repair companies “jam” the credit bureaus with repetitive dispute letters.

While some credit repair companies are more surgical in their approach when communicating with credit bureaus and lenders, some credit repair companies choose to simply bury them with repetitive dispute letters. This process is commonly referred to as “jamming.” Sometimes jamming is successful in getting negative information removed while other times it isn’t. And, of course, if you’re successful in getting negative information removed from your credit reports, your credit scores may improve.

Traditional credit repair comes with a price tag. The price tag, frankly, is what makes credit repair credit repair. If a company charges you a fee for a service represented as one that will help you to improve your credit, that meets the definition of a credit repair organization in the Federal statute known as the Credit Repair Organizations Act. If there is no fee or valuable consideration, then it’s not credit repair.

Adding Tradelines

There are only three ways to add tradelines to your credit reports, and two involve associating your name with a credit card account. You can certainly apply for and open a new credit card account. If you are approved the lender will likely report the account/tradeline to your credit reports.

You can also have your name added to an existing account as an authorized user. An authorized user is someone who is authorized to use the credit line of a credit card account, but doesn’t have any liability for the debt. Credit card issuers often report credit card account information to the credit reports of the authorized user. And, if the account is in good standing and has a low balance relative to the credit limit, the result can be an improvement in your credit score.

You can add tradelines to your credit report by becoming an authorized user on someone’s credit card.

Being added to someone’s credit card as an authorized user is free, meaning the card issuer isn’t going to send you a bill for adding someone to your credit card account. There are, however, companies that will broker the authorized user process and they do normally charge a fee for their services.

The third option is fairly new, Experian Boost. Boost is an Experian service whereby they will add your utility accounts to your Experian credit report if you pay them from your bank account. The service, as of the date of this article, is free.

Boost requires a leap of faith as you will be asked to provide the name of your bank and your login credentials, including your username and password. Using that information Experian will gain access to your utility payment transactions and add them to your credit report. If you do not pay your utilities with your bank account, you cannot add them to your credit report using Boost.

It appears the difference between traditional credit repair and tradelines is really the difference between addition and subtraction. Garden variety credit repair is built around getting negative information removed or “subtracted” from your credit reports. The tradeline or authorized user strategy is built around adding positive credit card accounts to your credit reports.

Because there is no single path to a lower credit score, there is also no single path to a higher credit score. As such, both credit repair and tradelines can result in higher credit scores. However, there is no guarantee that either will lead to higher scores as the impact of removing information or adding information is highly individualized and difficult to predict with a great deal of precision.

John Ulzheimer is a nationally recognized expert on credit reporting, credit scoring and identity theft. He is the President of The Ulzheimer Group and the author of four books about consumer credit. Formerly of FICO, Equifax and Credit.com, John is the only recognized credit expert who actually comes from the credit industry. He has 27+ years of experience in the consumer credit industry, has served as a credit expert witness in more than 370 lawsuits, and has been qualified to testify in both Federal and State courts on the topic of consumer credit. John serves as a guest lecturer at The University of Georgia and Emory University’s School of Law.

Disclaimer: The views and opinions expressed in this article are those of the author John Ulzheimer and do not necessarily reflect the official policy or position of Tradeline Supply Company, LLC.

The U.S. Small Business Administration (SBA) Office of Advocacy submitted comments on the Consumer Financial Protection Bureau’s proposed rule for the Fair Debt Collection Practices Act (Regulation F) in line with ACA International’s suggestions on consumer communications and disclosure notices … Continue reading →

Chicago Public Library is now the largest public library system in the nation to stop penalizing residents for overdue library books. Chicago will no longer fine residents for returning library books past due. Beginning Oct. 1, city libraries will stop … Continue reading →

A bill signed by Pennsylvania Gov. Tom Wolf allows consumers to permanently register their phone number on the Do Not Call (DNC) List. HB-318, the Telemarketer Registration Act, applies to telephone solicitors only, but debt collectors should take note of the precedent … Continue reading →

On September 18, 28 state attorneys general filed a comment letter in response to the CFPB’s Notice of Proposed Rulemaking (NPRM) amending Regulation F to implement the Fair Debt Collection Practices Act (FDCPA) (the “Proposed Rule”), urging the Bureau to … Continue reading →

Nearly half of Americans believe a credit score and a credit report are the same thing, according to a study by the American Bankers Association. That’s a big problem because it means many of us are seriously misinformed about how the credit system works.

Since credit is such an integral part of our financial ecosystem, it affects nearly all of us at some point in our lives. Your credit health can determine not only your access to credit and the cost of using credit but also employment opportunities, housing options, and more. Not understanding how credit works, therefore, can have serious consequences.

We want to help address this problem by making it easy to understand what your credit report is and why it’s important, the difference between your credit report and credit score, how to get a free credit report, and how to dispute errors on your credit report.

What Is a Credit Report and Why Is It Important?

A credit report is a detailed report on your credit history prepared by a credit reporting agency, also known as a credit bureau. The three main credit bureaus are Experian, Equifax, and TransUnion, and we’ll discuss each below. What is in your credit report can be different for each bureau, since they are private companies that do not share information.

What Is in a Credit Report?

Credit reports contain identifying information such as your name, social security number, and current and previous addresses. They also contain a detailed summary of your credit history, which includes items such as the following:

Credit reports include a list of your credit accounts and financial records.

A list of current and past tradelines (credit accounts), along with the date opened, credit limit, balance, and payment history of each account Inquiries into your credit history

Public records of bankruptcies, foreclosures, tax liens, etc. Accounts in collections

How Far Back Do Credit Reports Go?

The information in your credit report usually goes back about 7-10 years.

Current accounts should show up on your credit report as long as they are open.

Negative information, such as collections, will fall off your credit report seven years after the delinquency occurred. Closed accounts that were closed in good standing fall of your credit report in 10-11 years.

What Is the Difference Between a Credit Report and a Credit Score?

A list of all your credit accounts and related personal information

A three-digit number between 300 and 850 meant to represent your creditworthiness

Information in your credit report is used to calculate your credit score

Reflects the information in your credit report

You are legally entitled to get a free credit report from each bureau once a year

You are not legally entitled to check your credit score for free (although some credit card companies may offer this to customers)

Does not include your credit score

Does not include information on your credit history

Does Checking My Credit Report Hurt My Score?

While this is a common misconception, you can rest assured that checking your credit report won’t lower your credit score. Checking your own credit is what’s known as a “soft inquiry” or “soft pull,” which doesn’t hurt your credit. “Hard” inquiries can ding your score, but these are used by creditors when making lending decisions, not for checking your own credit report.

How to Get a Free Credit Report

By law, everyone is entitled to receive one free credit report from each of the three major credit bureaus once every 12 months. You can order all three at the same time or order each individual report one at a time.

Some people like to spread them out and get a free credit report from a different bureau every four months so that they can regularly check their credit reports for errors and inconsistencies. Each credit bureau is a private, for-profit company, and they don’t share information, so you could have errors on one of your credit reports but not the others.

Free credit monitoring websites like CreditKarma provide free credit reports and scores.

The best way to check your credit report for free is to order your free credit report from annualcreditreport.com. In fact, this is the only website authorized to provide the annual free credit report you are legally entitled to, according to the FTC—so beware of other sites claiming to offer free credit reports or free trials, especially if they ask for your credit card information.

However, there are now several free credit report websites that earn money through advertising and are thereby able to offer free credit monitoring services. Sites that offer completely free credit reports include:

You can also check your credit report for free if you have been denied credit because of the information in your credit report. You are entitled to get a free credit report from the bureau who provided the report that the lender used to make their decision.

You are entitled to a free credit report if you are unemployed and applying for jobs.

For example, if the lender who denied you credit looked at your Experian credit report, you can request your Experian free credit report. The adverse action letter informing you of the reason for your denial should have instructions on how to request your free credit report.

There are a few more cases in which you can qualify for an additional free credit report, including:

If you are unemployed and planning to look for work.

If you receive government assistance.

If you are a victim of identity theft.

Although experts recommend checking your credit reports at least once a year, the Consumer Financial Protection Bureau (CFPB) estimates that less than one in five consumers get copies of their credit reports each year. Don’t miss out on this opportunity to get your credit report for free so you can make sure your credit report is accurate and identify any problems before they get worse.

Can I Get a Free Credit Report Directly From the Credit Bureaus?

You can also get your credit report directly from each of the credit bureaus, but you may have to pay a fee if you go this route. If you want to get a credit report for free, your best bet is to order from annualcreditreport.com.

However, some people may want to check their credit reports more than once a year, so we’ll discuss additional options for obtaining your credit reports below.

Experian Credit Report

You can get a free Experian credit report that refreshes every 30 days through Experian’s website. They also offer paid options that come with additional information. The Experian free credit report does not include a free credit score.

Equifax Credit Report

You can get your TransUnion and Equifax free credit reports on third-party websites.

While you cannot get an Equifax free credit report from the bureau directly, you can pay a fee to access your Equifax credit report and score. To get your Equifax credit report, visit their website.

You can also view your free Equifax credit report and score through CreditKarma, which updates once a week.

TransUnion Credit Report

Accessing your TransUnion credit report requires signing up for a paid monthly subscription service with TransUnion. However, you can get a free TransUnion credit report from CreditKarma or NerdWallet.

How to Dispute Errors on Your Credit Report

Unfortunately, studies have shown that as many as one in five consumers may have errors on their credit reports, and about one in 20 have errors that are significant enough to potentially lower their credit scores. This means it is crucial to monitor your credit reports regularly and be aware of how to fix errors on your credit report.

The credit bureaus offer online forms to submit credit report disputes, but experts warn against using this option, as it does not allow you to write a detailed explanation of why you are disputing the information or provide sufficient supporting evidence. This leaves room for the credit reporting agency to deny your claim because you did not provide enough information.

The best way to dispute a credit report is to write a detailed credit report dispute letter and mail it to the bureau along with plenty of documentation verifying your identity and supporting your claim.

Once a dispute has been filed, the bureaus typically have 30 days to investigate the claim. If they verify that the item is accurate, it will remain on your report; if not, they must either update the item with the correct information or delete it entirely.

Errors on your credit report can, unfortunately, lead to bad credit. For this reason, checking your credit report regularly and disputing any errors is an essential step in maintaining your financial health.

It’s important to check your credit report for errors regularly.

If you have a lot of errors on your credit report or if you have been the victim of identity theft, it may also be worth considering hiring a reputable credit repair service to assist you in the dispute process.

Which Errors Can You Dispute?

The law requires that the information in your credit reports must be accurate, complete, timely, and verifiable. Anything that does not meet these requirements can be disputed.

Technically, you can dispute anything in your credit file, but that doesn’t mean you should try to dispute things that you know are accurate. The credit bureaus are allowed to ignore “frivolous” claims, and if they verify something to be true, it will stay on your credit report.

For more tips on how to dispute a credit report, check out this article from creditcards.com.

Quick Credit Report Facts

A credit report is a detailed report on your credit history prepared by one of the credit bureaus: Experian, Equifax, and TransUnion.

The information in your credit report is used to calculate your credit score.

Checking your credit report does not hurt your score.

You are entitled to a free credit report from each of the three bureaus once a year, which you can order from annualcreditreport.com.

You can dispute errors on your credit report by mailing a credit report dispute letter and supporting documentation to the credit bureau.

An Bord Pleanála has given the green light for the restoration of the derelict 19th century cottage at Blackrock to create a new restaurant and bicycle rental shop. In its decision, the Board overruled the recommendation of its own planning … Continue reading →

The Consumer Financial Protection Bureau published its quarterly consumer credit trends report on September 25. In the Report, the CFPB gave an in-depth look at bankruptcy trends and the impact of filing for the period 2001-2018, which includes the enactment … Continue reading →

Length of credit history, also referred to generally as credit “age,” is one of the five main factors in the credit score algorithm, making up roughly 15% of one’s credit score.

FICO breaks up this general category into three parts:

How long each individual account has been open

How long certain types of accounts have been open (e.g. revolving accounts vs. installment accounts)

The amount of time since those accounts were last used

Since a longer credit history provides more evidence that you have responsibly handled credit, generally, those with longer credit histories tend to have higher credit scores than those with shorter credit histories. When it comes to age, more is always better.

Account Age & Payment History Are Linked Together

Age always goes hand-in-hand with payment history, which contributes about 35% of your credit score, making it the most heavily weighted category. Obviously, an account needs to have age in order to have a payment history, and as an account ages, it acquires more payment history.

Age also affects the power of blemishes in your payment history. For example, a missed payment can cause a big drop in your credit score at first, but as the account ages, the effect will gradually be diminished until the missed payment falls off of your credit report completely.

Since the length of credit history (i.e. age) and payment history categories are closely linked, we can add them together to find out their combined power, which turns out to be 50% of a credit score! Therefore, age-related factors are going to be extremely important when it comes to choosing tradelines.

Some Age Levels May Hold More Weight Than Others

Since age is such a big part of credit, there is a lot of speculation about the specific age-related factors that may play a role in credit scoring algorithms. For example, it is commonly believed that there are certain age levels after which an account has a more powerful positive impact on one’s credit.

In other words, the positive effect of age on an account is not thought to be a gradual and continuous increase in score over time, but rather, a series of jumps upward that happen at certain points in time, such as after a specific number of years or months have passed.

As we said, many speculate on this topic, and we don’t pretend to have the definitive answer. FICO, VantageScore, and other credit scoring companies intentionally keep the details of their credit scoring formulas under wraps. However, based on the examples that we have seen, we have come up with our own observations on the question of which age levels are particularly beneficial for credit.

Age Bracket Experiment

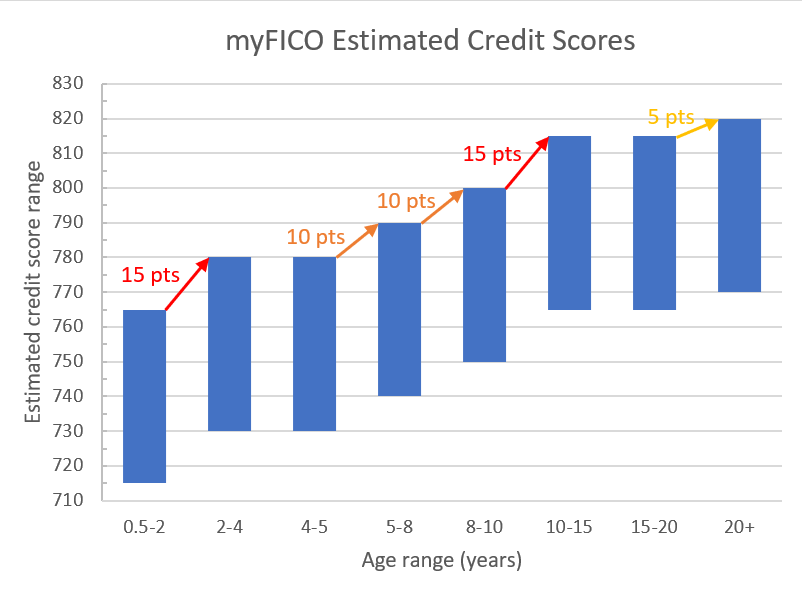

To test out our theory, we conducted an experiment. We chose to use the myFICO Score Estimator specifically since this credit score estimator is owned by FICO themselves, who are the creators of the most widely used and trusted credit score. It stands to reason that using a product straight from the source of the FICO score would give the most accurate findings.

Educational scores such as the VantageScore use different algorithms and are not widely used by lenders. Therefore, since our priority is to understand our FICO score, the FICO score estimator will be the most useful.

We used this credit score estimator to estimate credit score ranges with a different age of oldest account each time, holding all other inputs constant. To minimize any negative impact from other factors that could affect the results, such as late payments or high balances, we chose the options that should represent the best impact on credit while still establishing a credit history.

How Do Credit Card Age Levels Affect Credit?

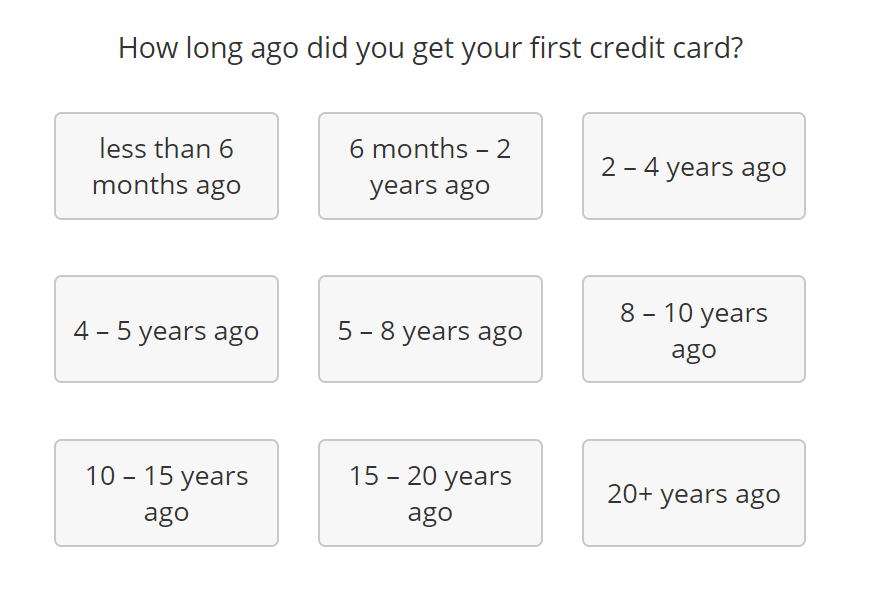

Here are the answers we gave to each question in the credit score estimator:

How many credit cards do you have? 1

How long ago did you get your first credit card? (This is what we were testing, so it changed each time.)

How long ago did you get your first loan? (i.e., auto loan, mortgage or student loan, etc.) Never

How many loans or credit cards have you applied for in the last year? 0

When was the last time you opened a new loan or credit card? More than 6 months ago

How many of your loans and/or credit cards currently have a balance? 0-4

Besides any mortgages, what is the total balance on all your loans and credit cards combined? Less than $500

When did you last miss a loan or credit card payment? Never

How many of your loans and/or credit cards are currently past due? 0

What percent of your total credit card limits do your credit card balances represent? 0% to 9%

In the last 10 years, have you ever experienced bankruptcy, repossession or an account in collections? No

FICO’s Age Brackets

If you take the quiz, you’ll notice that the myFICO credit score estimator gives a hint as to potentially important age levels right in the first question.

The myFICO credit score simulator gives a hint as to potentially important age levels in the first question.

We tested each of the options shown in the screenshot while keeping all other answers the same, as we described. Keep in mind that the score estimator does not give a single number for the answer, but a range of 50 points (e.g. 730-780). You can see the results of our credit score experiment below.

The myFICO Score Estimator predicts that when all other factors are held constant, credit score increases occur after 2 years, 5 years, 8 years, 10 years, and 20 years. The biggest jumps happen at 2 years and 10 years, but the highest credit score can be achieved after 20 or more years.

The myFICO credit score simulator shows credit score boosts after 2 years, 5 years, 8 years, 10 years, and 20 years.

Based on this information, here’s how we would divide up the age levels of tradelines:

Level 1

0.5 – 2 years

Level 2

2 – 5 years

Level 3

5 – 8 years

Level 4

8 – 10 years

Level 5

10 – 20 years

Level 6

20+ years

Why Age Is Top Priority When Buying Tradelines

We have already discussed why we believe age is usually the most important factor when making the decision to purchase tradelines in our buyer’s guide to choosing a tradeline. Since age and payment history are always interconnected, together making up half of the power of a credit score, it is usually most effective to focus on getting a tradeline with as much age as possible.

The information we learned from the myFICO score simulator just goes to show how true that is. There can be a significant difference in the power and value of a tradeline that is 11 years old versus 9 years old or one that is 2 years old versus 1 year old.

Also, keep in mind the importance of your average age of accounts. According to FICO, those with the highest credit scores have an average age of accounts of about 12 years, compared to just 6 years for those with fair credit. Recall from our buyer’s guide that you might be surprised by how old a tradeline would need to be in order to get your average age of accounts up to the next level!

FICO also says that those with credit scores of 795 and above have 27 years of credit history on their oldest tradeline, while those with credit scores of 635 only have 12 years of history on their oldest account.

Credit score

Average Age of Accounts

Age of Oldest Account

Conclusion on the Importance of the Age of a Tradeline

When attempting to understand any system, it is always best to go straight to the source to acquire the most accurate information. Fortunately, FICO provides tools such as their myFICO Score Estimator for everyone to use to experiment with their own credit-related variables.

The payment history of an account is always attached to time; in other words, the age of a tradeline will automatically include the payment history as well. With the length of credit history representing approximately 15% of your credit score, combined with payment history representing approximately 35%, together these add up to approximately 50% of your credit score. This is why the age of a tradeline is almost always the most important variable to consider.

As we can see from the results from this case study, it is also clear that there are key age brackets that hold more weight than others. Knowing this information allows you to set strategic goals and allows you to plan your credit growth more effectively.

Therefore, when choosing tradelines you should keep age as a top priority and aim for the age thresholds that hold the most weight. Make sure to use our tradeline calculator to help you with these calculations so you get the most out of your tradelines.