Education Secretary Betsy DeVos at a Cabinet meeting in July. (Alex Brandon/AP) Despite a court order barring the Education Department from collecting on the federal student loans of former Corinthian College students, the agency continued to pursue the debts. … Continue reading →

Image source: Getty Images What is good credit, anyway? There’s no one definition of “good” credit, as the answers can vary depending on who you ask. That said, the company behind the FICO® Score offers these good credit guidelines: DESCRIPTION … Continue reading →

If you want to know how today’s economy is doing, look no further than the consumer. Consumer spending makes up 68% of gross domestic product (“GDP”) in the U.S. That’s a bit hard to believe. Two-thirds of our economy is … Continue reading →

When consumers ask me questions about their credit reports it’s normally about how to get an item removed or corrected. Sometimes, however, I do get questions about having information added to a credit report. This type of question brings up an interesting concept, which is whether or not consumers have the right to certain credit report information or even the right to a credit report at all.

The Fair Credit Reporting Act

The Federal statute that governs the credit reporting agency’s actions, the use of credit reports, and the furnishing of information to the credit reporting agencies is the Fair Credit Reporting Act or “FCRA.” The FCRA is a consumer protection statute that has been around since the early 1970s and confers rights to consumers as it pertains to their credit reports. The Act has been amended dozens of times.

There is no language in the FCRA that affirmatively gives consumers the right to have a credit report. And, there’s also no language in the FCRA that gives consumers the right to demand that they do not have a credit report. The act is silent on those two issues.

The Voluntary System

What this means is you cannot demand that a credit reporting agency push a button, delete your credit report information, and then never again collect information about your credit obligations. Conversely, you also cannot force a credit reporting agency to reach out to your bank or other service providers, get information about how you manage your accounts, and then add them to your credit reports.

Your credit scores might not be the same.

There are some very limited scenarios with federally guaranteed student loans and their servicers. The loan servicers may be required by the Department of Education to credit report debtor obligations, but that’s not the same as a lender choosing to report, or not to report. That’s entirely voluntary.

From a more granular perspective, you also don’t have the right to identical credit reports and certainly, you don’t have the right to identical credit scores across the credit reporting agencies and the various brands of credit scores. So, you cannot demand that your credit reports at Equifax, Experian, and TransUnion be the same and you cannot demand that your FICO and VantageScore credit scores are identical.

In fact, you don’t even have the right to a credit score, at all. There are certain minimum criteria that must be met before your credit report will even qualify for a credit score. When your credit report is created, a process that normally occurs the first time you apply for credit, it will not qualify for a credit score because there isn’t enough information to make it scorable.

Consistency, or Inconsistency

Another interesting aspect of credit reporting and our control (or lack of control) over what goes on and what does not go on our credit reports is the issue of consistency. For example, I can be added as an authorized user on Credit Card A and also added as an authorized user on Credit Card B, and there’s no guarantee that both card issuers will choose to report the account on my credit reports.

There’s also no guarantee that the issuer of Credit Card A will credit report all of their authorized users. They may choose to report some of them, and then choose to not report the rest. There’s nothing I can do about this. There’s nobody to complain to about the consistency issues and you can’t leverage your rights to consistency, because you don’t have any.

You also cannot control whether or not any of your lenders report to all three of the credit bureaus. For example, you may have a lender that reports to Equifax, but not to Experian and TransUnion. You can come up with any number of other combinations, and those would be true as well.

Not all credit card issuers report authorized user data to the credit bureaus.

This can be an issue with the use of secured credit cards, which are a common tool used by consumers to build or rebuild their credit. Notwithstanding the fact that becoming an authorized user on a loved one’s credit card is a much better alternative, there’s no guarantee that your secured card issuer will report to any of the credit bureaus.

Users of Credit Reports

There’s one final issue to cover on this topic of consistency. The users of credit reports, as in lenders and debt collectors, also don’t have the right to use credit reports or to furnish information to any of the credit bureaus. All users of credit reports had to apply for service with the credit bureaus and then go through a process of consideration and evaluation by the credit bureaus before their accounts were approved.

And even if a company has an account with the credit bureaus, buys credit reports, and furnishes information to the credit bureaus there’s no guarantee that they will always have that account. The credit bureaus can choose to stop doing business with a lender or a debt collector. They can also choose to purge data provided by a former client. And like consumers, there’s nothing they can do to force a credit bureau to change their mind.

John Ulzheimer is a nationally recognized expert on credit reporting, credit scoring and identity theft. He is the President of The Ulzheimer Group and the author of four books about consumer credit. Formerly of FICO, Equifax and Credit.com, John is the only recognized credit expert who actually comes from the credit industry. He has 27+ years of experience in the consumer credit industry, has served as a credit expert witness in more than 370 lawsuits, and has been qualified to testify in both Federal and State courts on the topic of consumer credit. John serves as a guest lecturer at The University of Georgia and Emory University’s School of Law.

Disclaimer: The views and opinions expressed in this article are those of the author John Ulzheimer and do not necessarily reflect the official policy or position of Tradeline Supply Company, LLC.

For several years now, New York courts have grappled with the issue of what constitutes revocation of the acceleration of mortgage debt. Because the Appellate Division of New York has four Departments that preside over different counties within the state, … Continue reading →

Q. I am planning to apply for a new apartment soon and my credit score is 678 from Equifax and 608 from Transunion. What do most rental companies require to get approved? This is a low-income property.

I also want to get a new credit card for someone with low income and no annual fee. Are there any credit cards that will give me a card with my current credit scores? Also, should I wait to get a credit card after the apartment complex does their credit check or should I get a credit card first?

Dear Reader,

Each rental company will look at your credit report differently. Ultimately, they want to know if they can trust you to pay them on time every month. Because your credit score is considered fair, you may end up needing to have a bigger deposit to secure an apartment.

Having only fair credit can make it difficult to get a credit card with a decent interest rate. However, you can look for a secure credit card. These cards work like regular cards, but they are secured by a deposit you make. Secured cards provide a great way for people with no credit or with a low score the opportunity to improve their scores and their credibility.

Be sure to do your homework and compare several secured credit cards. Look for one that meets your needs–in this case, one that does not have an annual fee. Another option for improving your credit would be to check out Experian Boost. It uses your phone and utility bill payments to “boost” your score if you have been paying those regularly and on-time.

Now, whether you should wait to get your card after the apartment company reviews your credit, I think you should. Whenever you ask for new credit, even for a secured credit card, a hard inquiry is generated on your report, and it lowers your credit score. So, it’s best to have the highest possible score to get your apartment.

After that, apply for the card and use it strategically, always paying on time and only using up to 30% of your available credit or less. If you need additional guidance, feel free to contact an NFCC-certified credit counselor from a local nonprofit near you. They are ready to help and can provide more personalized recommendations for improving your credit. Good luck!

Sincerely,

Bruce McClary, Vice President of Communications

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

Derogatory items on your credit report can be a big problem for your finances. These negative marks can stay on your credit report and damage your credit scores for several years. Fortunately, there are some things you can do to avoid getting derogatory marks as well as reduce the damage if you do end up with a negative item on your credit.

We’ll help you understand minor and major derogatories, how derogatory items affect your credit score, and what you can do about them.

What Is a Derogatory Credit Item?

The word derogatory simply means negative, so a derogatory credit item is a negative item on your credit report.

Derogatory items hurt your credit score and can impact your chances of getting approved for credit.

There are two types of derogatory items: minor derogatories and major derogatories.

Minor Derogatory Items

A minor derogatory is a payment that was past due, either 30 days late or 60 days late. If, after the 30- or 6-day late, you brought the account current again, then it is considered a minor derogatory mark. However, if you are currently 30 to 60 days late, it is considered a major derogatory, which we will discuss below.

30 Days Past Due

Lenders cannot report your account as late to the credit bureaus until 30 days have elapsed since the missed due date, so if you pay your bill anywhere between one to 29 days after the due date, you should not see a derogatory item reflected on your credit report.

However, your lender may charge a late fee, so it’s still best to pay all of your bills on time. If you’ve never been late on the account before, you can contact your lender and see if they can waive the late fee for the accidental late payment. Many lenders are willing to do this for account holders that otherwise have good records.

In addition, if you have a promotional interest rate, you will most likely forfeit the promotional rate if you miss a payment, even if you were only a few days late.

A 60-day late payment could result in an interest hike from your credit card issuer.

60 Days Past Due

If you miss your due date twice in a row and become 60 days late, the situation becomes more serious. At this point, the credit card issuer can hit you with a penalty APR of up to 29.99%.

Not only will this high interest rate apply to all your purchases for at least the next six billing cycles, but in this case, the bank is also allowed to apply the penalty rate to your existing balance as well. Not all credit cards have penalty APRs, however, so check the terms of your card to see if you could be subject to one.

Thankfully, “universal default” is a thing of the past—the practice of credit card companies raising consumer’s interest rates if they were late on any loan with any lender was banned by the Credit Card Act of 2009.

However, the exception is if you have multiple cards with the same bank. In this case, if you miss a payment on one of the cards, the bank is allowed to raise your rates on all of the cards you have with them.

Major Derogatory Items

A court judgment against you is a major derogatory.

A major derogatory credit item is typically defined as an account that is 90 days past due or more. If you have a major derogatory on your credit report, that is a huge red flag to lenders, and it may hinder you from being able to qualify for credit.

Examples of major derogatory credit items include:

Charge-offs – This is when a creditor writes off your account as a loss because you are so delinquent on the debt that they assume that the debt is unlikely to be paid. This typically happens after six months have passed without payment. Collections – After your account has been charged off by the lender, they may try to regain a portion of their losses by selling the account at a discount to a debt collector, who then becomes the owner of the debt and will try to collect the funds from you.

Court judgments – A judgment is when a lender or debt collector sues you over an unpaid debt and the court orders you to repay it. A court judgment gives the lender or debt collector more powerful options to collect the money you owe them, such as garnishing your wages or putting a lien on your home.

Foreclosures – This happens when you become so delinquent on your home loan that the bank takes possession of the home so that they can try to recover the balance of the loan by selling the property.

Settlements and short sales – A settlement is an agreement between you and your lender that you will pay back part of the debt you owe them. The lender will then stop trying to collect more money from you after you have paid the settlement amount, but since you did not pay the full amount you owed, it is a derogatory item. A short sale is considered to be a type of settlement since the lender is agreeing to sell the property for less than the mortgage balance you owe.

Bankruptcy is the most serious derogatory credit item.

Repossessions – This is when the lender takes back possession of something such as your car or your house because you defaulted on the payments.

Public records – Public records such as delinquent taxes, liens, unpaid alimony, and unpaid child support, are derogatory items that can be severely damaging to your credit, especially if there is still a balance owed.

Bankruptcy – Filing bankruptcy means you are asking to be legally released from paying back some or all of your debts. Because of this, and because it affects several credit accounts, not just one, it is the most damaging derogatory item. It will almost certainly devastate your credit score and reduce your chances of getting approved for credit for a significant amount of time, although it is possible to recover from bankruptcy eventually.

How Do Derogatories Affect Your Credit Score?

As you may have guessed, any derogatory mark on your credit report can seriously damage your credit score. However, they do not affect everyone equally. There is no predetermined amount of points that is associated with any given credit action.

“There is no fixed value to any derogatory entry. Their value is always relative to the presence or absence of other similar derogatory entries on a credit report. So, the answer to the question ‘how much?’ varies from ‘not at all’ to ‘a whole lot’ — and everything in between.”

In other words, the effect of a derogatory item could range from a significant drop in your credit score to potentially no difference in your credit score at all. It is going to depend on 1) what else is already in your credit file and 2) the severity of the derogatory information.

For those who have pristine credit records, even one 30-day late payment can do some serious damage to their credit scores. On the other hand, if you already have some delinquencies on your report, additional delinquencies won’t have as great of an impact.

Derogatory items will also have a larger impact on those with thin or short credit files, meaning they do not have very much positive credit history to help soften the blow of a negative mark. In contrast, those with a thicker file or longer credit history will have more positive history in their file to help balance out any negative events.

Credit scorecards, or “buckets,” can affect the impact of a derogatory item on your credit score.

Another complication is the concept of credit scoring scorecards or “buckets,” which score groups of consumers differently based on certain characteristics of their credit profile.

As a hypothetical example, there could be a scorecard for consumers with no major derogatories and a scorecard for consumers with one major derogatory. In this case, getting your first major derogatory mark could put you into a different scorecard, wherein your score would be calculated in an entirely different way than it was before.

While the impact of a derogatory item is going to vary from person to person depending on their unique individual credit history, one thing we do know for sure is that derogatory items become less impactful to your credit as time passes.

In fact, it is still possible to have good credit with a derogatory mark on your credit report if it is an old item and you have balanced it out with positive credit history since then.

How Late Payments Affect Your Credit Score

In terms of how bad late payments are for your credit, it’s not so bad to miss a payment on one account for one or two months, according to an article on The Balance. However, missing payments on several different accounts for one to two months will be worse for your credit. And finally, missing even one payment for three months in a row will be equally as harmful as a charge-off or collection since they are all major derogatory items.

The Impact of a Derogatory Item May Depend on the Credit Scoring Model

When it comes to collection accounts, for example, collections that have been paid off and small-balance collections have different impacts depending on which credit score is used.

FICO 8, the most widely used credit score, considers both paid and unpaid collections to be major derogatories. That’s one reason why paying off a collection account may not always increase your credit score.

FICO 9 and VantageScore 3.0 and 4.0 disregard collection accounts altogether once they have been paid. In addition, these three scoring models assign less weight to medical collections. FICO 8 and FICO 9 ignore collections that had an original balance of less than $100.

Paying the past-due balance does not make the derogatory mark disappear, but it is usually still a good idea.

Does Paying the Past-Due Balance Delete the Derogatory Mark?

Unfortunately, simply bringing the account current by paying the past-due balance does not make the derogatory mark disappear. It does not negate the fact that you were late paying your bill, which is important information that helps determine your credit score and helps lenders decide whether they want to do business with you.

Payment history is the most important part of both your FICO score and your VantageScore for a reason. It is highly predictive of how much of a credit risk you represent to lenders. For that reason, accurate derogatory information must stay on your credit report even after you have caught up on payments.

However, can still be beneficial to pay off the derogatory items on your credit report. Experian says, “While paying off a derogatory account won’t automatically remove it from your credit history, it will be updated to show it has been paid, and lenders may view a paid derogatory more favorably than an unpaid one.”

How to Minimize the Credit Score Impact of a Derogatory Item

Although bringing an account current will not remove the negative information from your credit report, it is still a good idea. Having made a late payment in the past and then catching up is better for your score than currently being late.

Moving forward, do your best to make sure you’re not late again.

Maintaining a positive credit history from now on is the most important thing you can do to minimize the effect of a derogatory item and restore your credit back to health.

Once you have done all you can to mitigate the damage of a derogatory item, then it simply becomes a matter of waiting until the negative mark ages off your credit report.

How Long Can Derogatory Credit Items Stay on Your Credit Report?

In general, derogatory marks can be reported for up to seven years after the account was first reported as late, which is referred to as the date of first delinquency (DOFD).

If you get a court judgment against you, however, that will remain on your credit report for seven years after the judgment was issued, not seven years from the date you were first late on the original debt.

Certain types of accounts can stay on your credit report even longer. Depending on the type of bankruptcy, for example, bankruptcy may stay on your credit report for up to 10 years.

According to Experian, since a Chapter 13 bankruptcy requires you to pay some of the debts you owe, this type of bankruptcy is removed from your credit report after seven years. With a Chapter 7 bankruptcy, you don’t pay back any of the debt, so it is removed 19 years after the date of filing instead of seven years. The individual accounts associated with the bankruptcy will still disappear seven years after the DOFD for each account; filing for bankruptcy does not affect the seven-year timeline.

Dispute derogatory items on your credit report that are inaccurate via mail.

Besides a Chapter 7 bankruptcy, all other delinquencies are required by law to be deleted from your credit report after seven years. However, the impact of a derogatory mark on your credit score will decrease over time, especially if you maintain a positive credit history going forward that can help outweigh the negative items.

Removing Derogatory Credit Items From Your Credit Report

If you have inaccurate negative items on your credit report, it’s in your best interest to dispute the derogatory items on your credit report as soon as possible.

Your credit reports should have instructions on how to dispute derogatory credit items that have been put on your credit report in error. The best way to dispute inaccurate negative information is to send a separate letter for each dispute via certified mail, along with any accompanying evidence that is needed to verify the validity of your claim.

Make sure to dispute the derogatory items on your credit report with the credit bureaus as well as with the creditor that is furnishing the data.

Should You Write a Letter Explaining Derogatory Items on Your Credit Report?

You may need to write a letter explaining derogatory items on your credit report when applying for a mortgage.

A letter of explanation is a letter that you write to a lender explaining the reason for negative marks on your credit report. This may be required by your lender when you apply for a mortgage, particularly when applying for a home loan that is subsidized by the government, such as an FHA loan or VA loan.

Your mortgage lender needs to be certain that you will be able to pay off your home loan. They will want to understand the circumstances of any derogatory items on your credit report in order to determine whether you have learned from your mistakes and taken steps to improve your situation or whether you may still be at risk of defaulting on a loan in the future.

A good letter of explanation should be truthful, clear, and detailed. If there were extenuating circumstances that led to you becoming behind on your bills, explain what happened and how you resolved the problem. As with a credit report dispute, be sure to include any documentation that supports your story along with your letter of explanation. Try looking up sample letters of explanation online if you need help.

How to Avoid Getting Derogatory Marks on Your Credit Report

Since accurate and timely derogatory information can’t legitimately be removed from your credit report, the best strategy is to prevent them from happening in the first place.

If you accidentally miss a payment, call your creditor right away to see if they can waive your late fee.

Here are some tips to help you keep your credit in the clear.

To ensure you never miss a payment, set up automatic payments for all your loans and credit cards.

As an additional precaution, also set up notifications that alert you when your statement is available and when your due date is coming up so that you can keep an eye on your accounts and make sure that the payments are going through. Knowing exactly when your bill is due and how much you need to pay will also allow you to make sure that you have sufficient funds in your bank account to make the required payments.

If you are in a period of financial hardship and can’t afford to make the minimum payment, contact your creditor and try to work out an arrangement with them to temporarily reduce or defer payments.

If you accidentally miss a payment but you usually pay on time, bring the account current by making the payment as soon as possible. Then, contact the lender and ask if they would be willing to waive the late fee. If you pay before 30 days have passed since your original due date, you can avoid getting a derogatory mark reported to the credit bureaus. If you’re 30 to 60 days late, you’ll have a minor derogatory on your credit report, but not a major derogatory. Try your best to pay before the account becomes 90 days past due, at which point it will count as a major derogatory.

Regularly check your credit reports for derogatory items that don’t belong to you so you can dispute the errors and have them removed from your credit report.

Conclusions

Having derogatory items on your credit report, particularly major derogatories, can be highly damaging to your credit for a long time. If there are derogatory items in your past, balance out the negative effects by adding positive payment history going forward, and use smart credit strategies to avoid getting derogatory marks in the future.

If you have bad credit or no credit at all, you’ll likely have a hard time getting a loan. After all, the paradox of credit is that it’s hard to get credit without already having a credit history, much like trying to get a job without any work history.

A credit-builder loan can be a good option for those with no credit or bad credit because credit-builder loans do not require the borrower to have good credit to get approved. However, you will need to show that you have enough income to cover the monthly payments.

Just like a traditional loan, your payment history will be reported to the major credit bureaus. That means you need to make all of your payments on time if you want to build up your credit score.

How Do Credit-Builder Loans Work?

Credit-builder loans, also sometimes called “fresh start loans” or “starting over loans,” are set up differently than traditional loans in order to minimize risk for lenders.

These loans are typically small amounts, such as $500 or $1000. In addition, unlike other types of loans, you do not receive the money upfront and pay it back later. Instead, this process is reversed.

The definition of a credit-builder loan is a loan where you make the payments first and receive the funds after you have finished paying off the loan. The lender deposits the amount you are borrowing into a savings account or certificate of deposit that will be held for you until you finish making all the payments. Until that point, you can’t access the funds.

Do You Need a Credit Check to Get a Credit-Builder Loan?

Because credit-builder loans are low-risk, in many cases, you can apply for credit builder loans with no credit check. You’ll likely just need to provide your income to prove that you can afford to make the payments.

Banks That Offer Credit-Builder Loans

Most of the big national banks, such as Chase, Bank of America, and Capital One, do not typically offer credit-builder loans, although Wells Fargo offers secured personal loans.

The best credit-builder loans can often be found at local banks and credit unions or through online lenders.

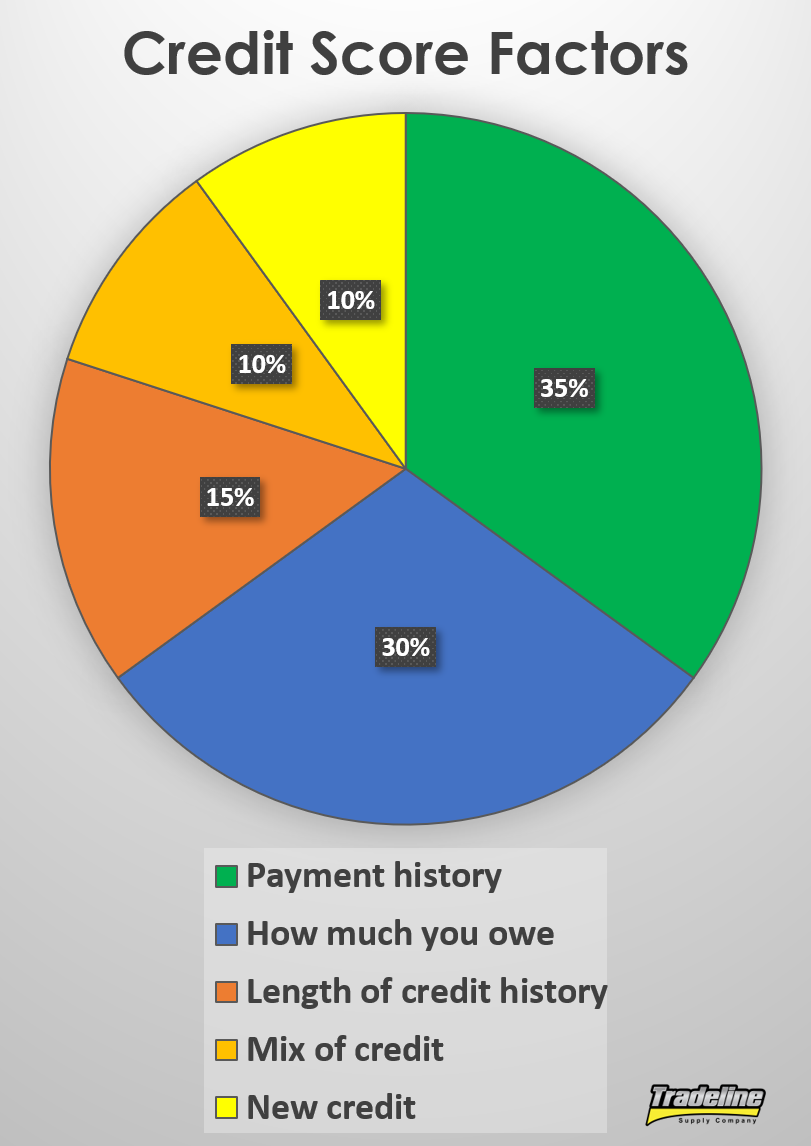

Payment history makes up 35% of your FICO score.

Are There Downsides to Getting a Credit-Builder Loan?

With a “fresh start” loan, as with any loan, it can hurt your credit score if you miss any payments. Remember, payment history is the biggest contributing factor to your credit score, weighing in at 35%. So when it comes to building credit, you need to be prepared to make every single payment on time.

In addition, you will be paying interest on the loan and potentially an application fee or other fees, although some lenders may partially refund the interest if you pay the loan back on time.

Finally, it may be several months to over a year before you finish paying off the loan and receive your borrowed funds. Building up a credit score by making payments on a loan takes a minimum of six months of payment history, according to FICO.

Other Ways to Build Credit

For those looking to build or rebuild credit, credit-builder loans are just one option. If you need to build credit fast, also consider one of the credit piggybacking methods we cover in “The Fastest Ways to Build Credit.”

By purchasing authorized user tradelines, for example, you can add seasoned tradelines with years of credit history to your credit report within just days.

Conclusions on Credit-Builder Loans

For those who may be struggling to build credit due to bad credit or lack of credit history, a credit-builder loan represents one way to get a loan with no credit check and start building a positive credit history.

Just like other types of loans, credit-builder loans come with interest and fees, and the main downside of this type of loan is that you don’t have access to the funds until after you have made all the payments.

On the other hand, when you finish paying off the loan, you will have built up a record of on-time payments and you will have a chunk of savings to take home.

AMARILLO — If 69-year-old Lynda Sue Costley wants to shower, she has to go to a friend’s house. Her trailer, on a gravelly road outside Amarillo, hasn’t had running water since 2014 — when her husband died from cancer. She … Continue reading →

The CEO of Melaleuca pitched a proposal to put limits on medical debt collection to almost half of the Idaho Legislature Monday evening. “I can’t imagine very much objection to this, given every single family is affected by this one … Continue reading →

When consumers ask me questions about their credit reports it’s normally about

When consumers ask me questions about their credit reports it’s normally about

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast. Derogatory items on your credit report can be a big problem for your finances. These negative marks can stay on your

Derogatory items on your credit report can be a big problem for your finances. These negative marks can stay on your