Education Secretary Betsy DeVos is pushing ahead on her plans to cancel only a portion of loans taken out by defrauded college students, even amid legal setbacks and as House Democrats prepare to grill her during a hearing next week. … Continue reading →

Canadians will likely see a slight increase in debt and delinquencies next year, particularly in Western provinces hit by downturns in the oil and farming industries, according to a new report by a consumer credit reporting agency. The average Canadian’s … Continue reading →

What is the difference between your overall credit utilization ratio and individual utilization ratios and why does it matter to your credit? Keep reading to find out.

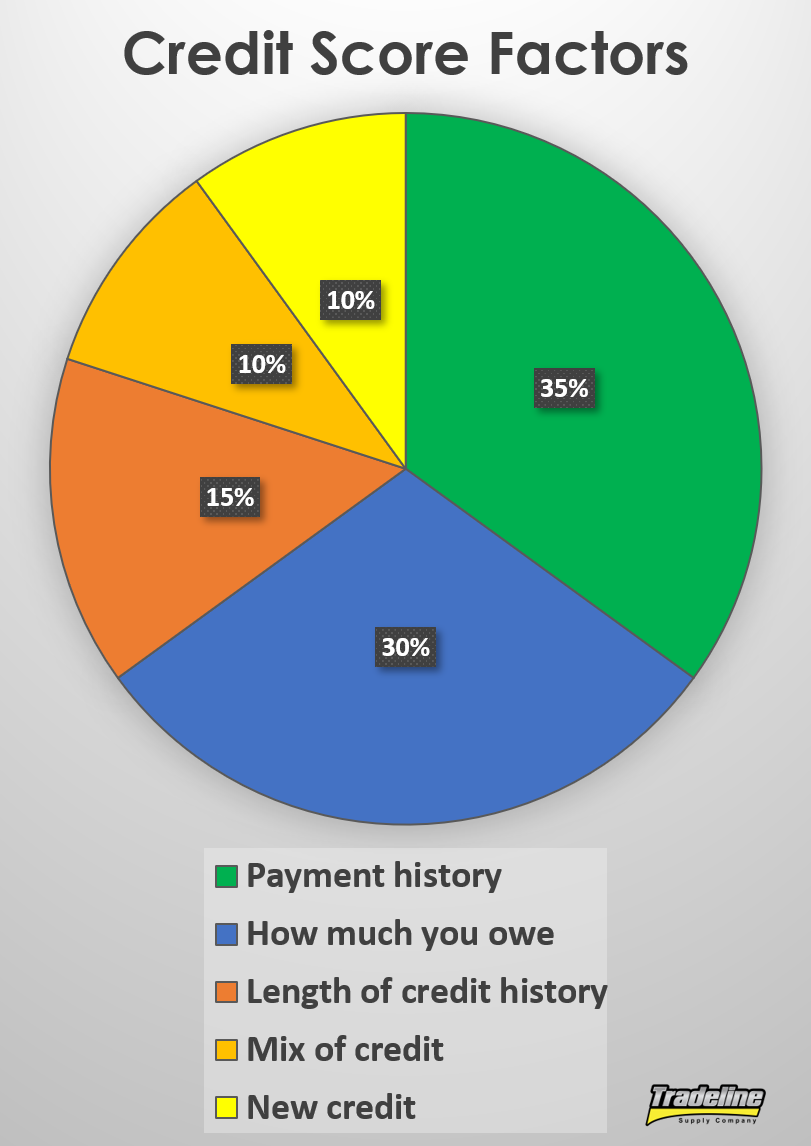

Credit utilization makes up 30% of a FICO score.

What Is Credit Utilization?

To put it simply, credit utilization is the amount of debt you owe compared to the amount of your available credit. In other words, it is the amount of your available credit that you are actually using.

In terms of your credit score, credit utilization makes up 30% of your score, second only to payment history.

The reason credit utilization is such an important part of your credit score is that the ratio of debt someone has is highly indicative of whether they will default on a debt in the future. The more you owe, the harder it becomes to pay off all that debt on time every month, which makes you a riskier bet for lenders.

Components of Credit Utilization

According to FICO, there are several components that fall within the category of credit utilization, such as:

The total amount you owe on all accounts (overall utilization)

The amount you owe on different types of accounts

The utilization ratios of each of your revolving credit accounts (individual utilization)

The number or ratio of your accounts that have balances

The amount of debt you still owe on your installment loans (e.g. mortgages, auto loans, student loans)

What Is the Difference Between Individual and Overall Utilization?

Your overall utilization ratio is the amount of revolving debt you have divided by your total available revolving credit.

For example, if you have one credit card with a $450 balance and a $500 limit and a second credit card with a $550 balance and a $3,500 limit, your overall utilization ratio would be 25% ($1,000 owed divided by $4,000 available credit).

However, the individual utilization ratios of your respective credit cards are 90% ($450 balance / $500 credit limit) and 16% ($550 balance / $3,500 credit limit).

Since credit scores consider individual utilization ratios, not just overall utilization, having any single revolving account at 90% utilization is going to weigh negatively on the credit utilization portion of your score.

Overall Utilization May Not Be as Important as You Think

Typically, when people think of the effect that credit utilization has on credit scores, they often assume that overall utilization is the only important variable.

By this assumption, it would be fine to have individual accounts that are maxed out as long as the overall utilization is still low.

Individual utilization ratios may be more important than the overall utilization ratio.

However, we have seen that this is often not true.

For example, sometimes clients with maxed-out credit cards will buy high-limit tradelines in order to reduce their overall utilization ratio, but then they don’t see the results they were hoping for.

This means that the individual accounts with high utilization are still weighing heavily on the clients’ credit scores, despite the fact that they have improved their overall utilization. In other words, the decrease in the overall utilization ratio did not make much of a difference.

Cases like this seem to indicate that overall utilization may not play as big a role as traditional wisdom has led us to believe and that the individual utilization ratios may be more important.

Although the age of a tradeline is often its most valuable asset, tradelines can still help with some of the credit utilization variables.

Since our tradelines are guaranteed to have utilization ratios that are at or below 15%, this means that at least 85% of that tradeline’s credit limit is going toward your available credit, which helps to lower your overall utilization ratio. In fact, most of our tradelines tend to maintain utilization ratios that are much lower than 15%.

Buying tradelines also allows you to add accounts with low individual utilization to your credit file, which can help to improve the number of accounts that are low-utilization vs. high-utilization.

As a general rule of thumb, simply aim to keep your utilization as low as possible. However, you might be surprised to learn that having a zero balance on all revolving accounts is actually not the best scenario for your score.

According to creditcards.com, “…the ideal scenario tends to be having all but one card show a zero balance (zero percent utilization) and having one card with utilization in the 1-3 percent range.”

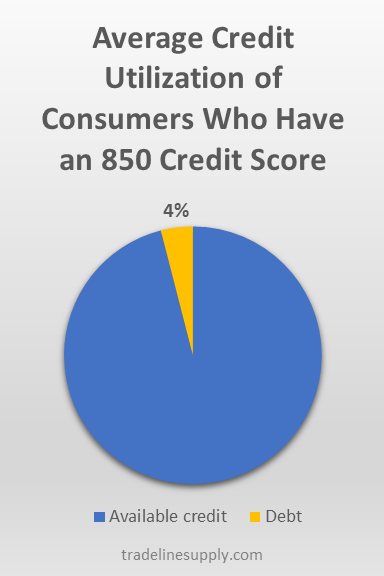

The average credit utilization ratio of consumers who have an 850 FICO score is about 4%.

Why? As it turns out, consumers with a 0 percent utilization ratio actually have a slightly higher risk of defaulting than those with low (but more than 0) utilization. A 0 percent utilization indicates that a consumer may not use credit regularly, which leads to the consumer having a higher risk of default in the future.

However, your utilization doesn’t necessarily have to fall in line with the above scenario in order to have a perfect credit score. In “How to Get an 850 Credit Score,” we found that consumers with FICO credit scores of 850 have an average utilization rate of 4.1%.

For those of us who use credit regularly, however, maintaining a minuscule balance may not always be practical. So what is a realistic threshold to shoot for?

While you may hear the figure 30% cited frequently, many credit experts say this is a myth and that you should aim for 20%-25% instead.

Tips to Avoid Excessive Revolving Debt Utilization

Spread out your charges between different cards

Since we have seen that it’s important to keep individual utilization ratios low, one strategy to accomplish this is to make your purchases on a few different credit cards instead of charging everything to one card. Spreading out your charges helps to prevent an excessively high balance from accumulating on any one individual card.

Pay off your balances more frequently

If you spend a lot on one of your cards, consider spreading out your charges between different cards or paying down the balance more often.

If you do spend a lot on one card, it helps to pay off your balance more than once a month. If your card reports to the credit bureaus before you have paid off your balance, it will show a higher utilization than if you had paid some or all of the balance down already.

You can either time your payment to post just before the reporting date of your card or you can make payments several times per month. Some people even prefer to pay off each charge immediately so their card never shows a significant balance.

Set up balance alerts to monitor your spending

To prevent mindless spending from getting out of control, try setting up balance alerts on your credit card. Your bank will automatically notify you when the balance exceeds an amount of your choosing, so you can back off of spending on that card or pay down your balance.

Don’t close old accounts

Even if you don’t use some of your old credit cards anymore, it’s often a good idea to keep the accounts open so they can continue to play a positive role in your overall utilization ratio and the number of accounts that have low utilization vs. high utilization.

Ask for credit limit increases

Another way to decrease your utilization ratios is to call your credit card issuers and ask them to increase your credit limit. By increasing your amount of available credit, you decrease your utilization ratio, both on individual cards and overall.

Keep in mind that your bank may do a hard pull on your credit to decide whether or not to grant your request, which could ding your score a few points temporarily. However, the small negative impact of the credit inquiry could be offset by the benefit of the credit line increase.

Also, this might not be an ideal strategy if you think you will be tempted to spend the new credit available to you, which could leave you even worse off than you started.

If you want to learn more about how you can successfully ask for credit line increases, check out our article, “How to Increase Your Credit Limit.”

Open a new credit card

Like asking for a higher credit limit, opening a new credit card can also lower your credit utilization, provided you leave most of the credit available.

Again, this will add an inquiry to your credit report, as well as decrease your average age of accounts, so this could have a negative impact on your score temporarily, which may be outweighed by the decrease in your credit utilization.

Transfer your credit card balances to different cards

A balance transfer is when you use available credit from one credit card account to pay off the balance on another credit card, thus “transferring” your debt balance from one card to another.

There are two ways to do this: you can transfer a balance to another credit card you already have, as long as it has enough available credit, or you can transfer a balance by applying for a new credit card and letting the card issuer know in your application which account you want to transfer a balance from and how much you want to transfer.

The latter option is best for your credit utilization, since opening a new credit card means you are adding available credit to your credit profile. In addition, it gives you the opportunity to apply for specific balance transfer credit cards, which usually come with low promotional interest rates on the balances you transfer.

However, using an existing account to do a balance transfer can still be beneficial if done properly, because it can help your individual utilization ratios. Just make sure the account you are transferring the balance to has a higher credit limit than the account that is currently carrying the balance in order to keep the individual utilization ratios as low as possible on each account.

Pay down smaller balances to zero

Having too many accounts with balances can bring down your score since credit scores consider the number of accounts in your credit file that are carrying a balance. If you have any accounts with smaller balances, paying those down to zero will decrease the individual utilization ratios on those accounts, reduce your overall utilization ratio, and reduce the number of accounts with balances, thus improving your credit profile in multiple ways.

KEY POINTS A new survey finds that 84% of individuals would rather save $5,000 than shed 5 pounds in 2020. Another big goal for next year — reducing debt — tops other resolutions, such as reducing computer or phone screen … Continue reading →

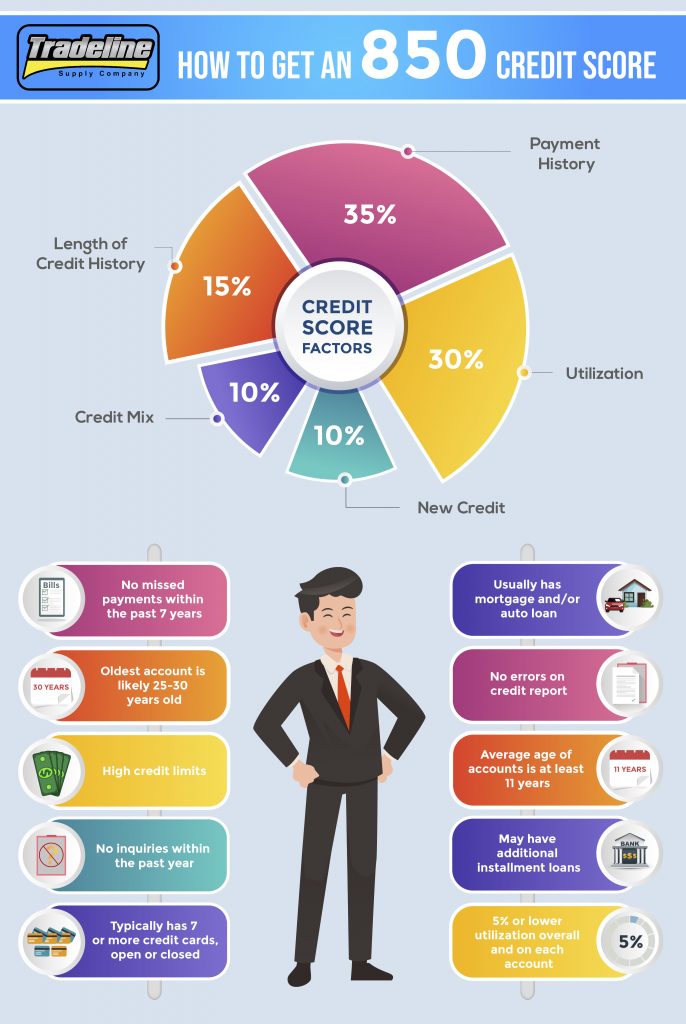

People who are serious about improving their credit often wonder what it takes to get the highest possible credit score. For the FICO 8 credit scoring model, the perfect credit score is 850.

As of April 2019, only about 1.6% of scorable consumers in the United States have the elusive 850 credit score, which is actually an increase from 0.98% in April 2014 and 0.85% in April 2009.

There are many other credit scoring models that are used for different purposes and may have different credit scoring ranges. However, since FICO 8 is the most commonly used credit score, we will use the number 850 as the benchmark for the ideal credit score.

Check out the infographic below for some fast facts on how to get the highest credit score possible, then keep reading the article for even more tips on getting the coveted 850 credit score.

Payment History — 35%

Most people who have an 850 credit score have seven years of perfect payment history.

Your payment history is the biggest slice of the credit score pie, so even one late payment or missed payment can significantly affect your score. Negative items can stay on your credit report for up to seven years, so if you miss a payment, you may not be able to achieve a perfect 850 credit score until at least seven years have passed!

To safeguard against the possibility of forgetting to make a payment, consider setting up automatic bill pay for all of your accounts. Be sure to continue to check your accounts regularly in case of any system errors.

If you do miss a deadline once in a blue moon but have otherwise been an upstanding customer, try negotiating with your creditor to see if they will forgive the late payment and wipe it from your record.

FICO says that 96% of “high achievers,” or those with FICO scores above 785, have no missed payments on their credit report.

Essentially, to get an 850 credit score, you just need to follow one simple strategy: make all of your payments on time for a long time. We will further discuss the connection between payment history and time in the “Length of Credit History” section below.

Credit Utilization/How Much You Owe — 30%

The amount of debt you owe compared to your total credit limit is your credit utilization ratio. To get a perfect credit score, you’ll want to keep this ratio as low as possible, both overall and on each of your individual tradelines.

A study by VantageScore and MagnifyMoney found that people with the best credit scores and people with the worst credit scores actually had similar amounts of outstanding debt. However, those with the best scores had an average total credit limit of $46,700—16 times the credit limit of those with the worst scores!

Therefore, for the high scorers, that outstanding debt made up a much smaller percentage of their total available credit than those with low credit limits and poor scores, which highlights the importance of the overall utilization ratio.

This study reported that the average credit card user has an overall utilization ratio of 20%, which is generally considered to be a safe number for maintaining decent credit. To become someone who has an 850 credit score, however, you’ll need to keep it around 5% or lower. As of 2019, FICO says that the average revolving utilization for those with the “850 profile” is 4.1%.

While consumers with 850 credit scores do use credit cards, they tend to keep their utilization ratios around 5% or lower. Photo by Ellen Johnson.

In addition, keep in mind that even if you have a low overall utilization ratio, individual cards with high utilization could still bring down your score. You can read more about this in our article on individual vs. overall credit utilization ratios.

As a hypothetical example, let’s say you have two cards: one with a $10,000 limit and a $0 balance and the other with a $1,000 limit and a $900 balance. Your total available credit is $10,000 + $1,000 = $11,000 and your total debt is $900. Therefore, your overall utilization ratio is $900 / $11,000 = 8% utilization, which is a very good number.

However, your account with the $1,000 limit has a 90% individual utilization ratio! Since you only have two accounts, that means 50% of your accounts have high utilization, and that could negatively affect your credit. According to creditcards.com, maxing out just one credit card can reduce your score by as many as 45 points.

To get around this problem, if you have any individual cards with high utilization, consider transferring the balance to other accounts to keep the utilization ratio on each account as low as possible.

You could also request credit line increases from your creditors, which can lower your utilization ratios and benefit your score. Try using the tips we provide in “How to Increase Your Credit Limit.”

Another way to help with overall utilization is to add low-utilization tradelines to your credit file.

Optimizing this factor also means not closing old accounts even if you don’t use them very often, because their credit limits could be helping your score. To ensure old accounts don’t get automatically closed by the banks for inactivity, try to use them every 1-2 months, perhaps for small, recurring bills.

Length of Credit History (Age) — 15%

This category takes into account age-related factors such as the average age of your accounts, the age of your oldest account, and the ratio of seasoned to non-seasoned tradelines. (A seasoned tradeline is an account that is at least two years old, which is when the account is believed to have a more positive impact on your credit.)

Age goes hand-in-hand with payment history, because the more age an account has, the more time it has had to build up a positive or negative payment history. Together, age (15%) and payment history (35%) make up 50% of your credit score, which shows how important it is to open accounts early and make every single payment on time.

According to FICO, the age of the oldest account of people who have 650 credit scores is only 12 years, compared to 25 years for people who have credit scores above 800. In addition, individuals with fair credit have an average age of accounts of 7 years, compared to 11 years for those with excellent credit.

Cultivating an 850 credit score takes years of maintaining a positive credit history.

FICO reports that the average age of the oldest account of consumers who have 850 credit scores is 30 years old.

We have an in-depth discussion of which age tiers are most significant in our article, “Why Age Is the Most Valuable Factor of a Tradeline,” but the bottom line for getting the best credit score is simply to get as much age as possible. Seasoned tradelines can help by extending the age of the oldest account and the average age of accounts.

Also, keep in mind that it may be impossible to achieve an 850 credit score without a certain amount of age, even if you do everything else perfectly. So if you have stellar credit habits but haven’t yet been able to join the 850 credit club, you may just need to wait patiently for your accounts to age.

Credit Mix — 10%

While the mix of credit is one of the least important factors in a credit score, to get a perfect credit score of 850, you will still need to consider this factor.

In this category, credit scores reward having a balanced mix of several different accounts, including both revolving credit and installment loans. This is because creditors want to see that you can successfully manage a variety of different types of credit.

As an example, a credit file that includes an auto loan, a mortgage, and two credit cards has a better credit mix than a credit file that has four accounts that are all credit cards.

About the “credit mix” credit score factor, FICO says, “Having credit cards and installment loans with a good credit history will raise your FICO Scores. People with no credit cards tend to be viewed as a higher risk than people who have managed credit cards responsibly.”

The total number of accounts is also considered, with more accounts generally being better, up to a certain point.

FICO also states that high score achievers have an average of seven credit card accounts in their credit files, whether open or closed.

Auto loans are common among people who have 850 credit scores.

If you are looking to improve your credit mix statistics, adding authorized user tradelines can increase the total number of accounts and help diversify one’s credit file.

850 scorers also have installment loans in their credit files. According to Experian, the average mortgage debt for consumers with exceptional credit scores (800 or above) is $208,617. In addition, people who have FICO scores of 850 have an average auto-loan debt of $17,030.

Experian says, “In every other debt category except mortgage and personal loan, people with perfect scores had more open tradelines but less debt than their counterparts with average scores—underscoring the value of being able to manage debt while having numerous credit accounts.”

The “new credit” category of your credit score refers to how frequently you shop for new credit. This includes opening up new credit cards and applying for loans, for example. This “new credit” activity is reflected in the number of inquiries on your credit report.

Since seeking new credit makes you look like a higher risk to creditors, each hard inquiry has the potential to drop your score by a few points. Therefore, if you are going for a perfect 850, it’s best to avoid applying for new credit for a while.

However, it is possible to score an 850 with hard inquiries on your record. FICO recently stated that around 10% of 850 scorers had one or more inquiries within the past year, and about 25% had opened at least one new credit account within the past year.

If you need to shop for an auto loan or mortgage, be sure to complete all your applications within a two-week window in order for all of the credit pulls to count as one inquiry. For credit cards, however, each inquiry will be typically be counted individually.

Fortunately, inquiries only remain on your credit report for two years, and FICO scores only consider inquiries that occurred within the past year, so it shouldn’t take long for your credit to recover if you do have new inquiries on your credit report.

Inquiries aren’t the only thing that matters when it comes to the new credit factor of your credit score, however. It also includes data points such as the number of new accounts you have, the ratio of new accounts vs. seasoned accounts, and the amount of time that has passed since opening new accounts. The main idea if you want to maximize your credit score is to not open too many new accounts at once, which can make you look riskier to lenders and bring down your score.

More Tips on How to Get an 850 Credit Score

In addition to optimizing each of the above five categories that factor into your credit score, it is also important to regularly check for errors on your credit report and dispute any inaccurate information both with the credit bureaus as well as with the lenders who furnish the data to the bureaus.

In addition, those with very high credit scores rarely have serious delinquencies or public records on their credit reports, such as bankruptcies or liens. Obviously, this will be easy to avoid if you follow all of the suggestions above, but if you have a history of bad credit in your past, it could take up to 7-10 years to recover enough to get an 850 credit score.

850 Credit Score Benefits

What are the benefits of being in the 850 credit club? In reality, you’ll be able to take advantage of the benefits of having an excellent credit score whether you have a 760 credit score or an 850 credit score. You don’t need to score a perfect 850 to get the best credit cards or the best interest rates on loans.

Essentially, the main benefit of having the best possible credit score is bragging rights!

Final Thoughts on How to Get the Perfect Credit Score

While it’s probably not necessary to get an 850 credit score, it is smart to work toward the goal of having excellent credit by managing your credit wisely, which will eventually get you into the upper levels of high credit score achievers.

The most important factors of your credit score are payment history, utilization, and age. Therefore, to keep your credit in pristine condition, you’ll need to make all of your payments on time, keep your utilization as low as possible, and maximize your credit age. Beyond that, you’ll also want to maintain a balanced mix of accounts and minimize new credit inquiries.

Finally, take advantage of your three annual free credit reports to make sure your credit reports are free of damaging errors.

To summarize, here’s an example of what the credit profile of someone who has an 850 credit score might look like, as we illustrated in the infographic above:

No missed payments or delinquencies within the past seven years

A high total credit limit

The overall utilization ratio is 5% or lower

Individual credit cards each have low utilization, around 5% or lower

The oldest account is likely about 25-30 years old

The average age of accounts is at least 11 years

Typically has at least seven credit card accounts (whether open or closed)

Usually has an auto loan and/or a mortgage loan

May have additional installment loans

Minimal inquiries within the past year

No damaging errors on their credit report

Have you ever achieved the perfect 850 credit score? Is it a goal that you are currently working toward? Share your thoughts with us by leaving a comment below!

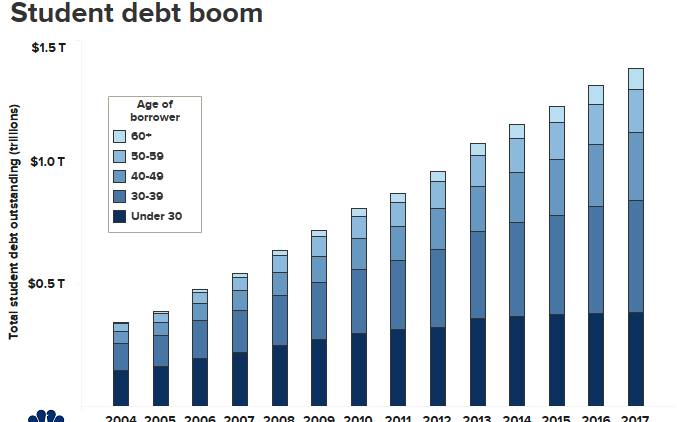

CNBC | Jaden Urbi Outstanding education debt has outpaced credit card and auto debt. The average college graduate leaves school $30,000 in the red today, up from $10,000 in the 1990s. Nearly 40% of students who took out loans in … Continue reading →

WASHINGTON – U.S. consumers ramped up their credit card spending in October. The Federal Reserve said Friday that total consumer borrowing rose in October by a seasonally adjusted $18.9 billion, up from a September increase of $9.6 billion. It was … Continue reading →

The scoop on who’s paying credit card fees and how to avoid them Interest tends to be the biggest cost associated with credit card usage, but it’s far from the only one. Credit cards come with a myriad of charges, … Continue reading →

The analysis by CreditCards.com found that New Mexico strains under the heftiest debt load in the country, while Massachusetts carries the lightest. Southern states take most of the top 10 spots for debt load, and only three Southern states, Delaware, … Continue reading →

Most of us have credit reports assembled about us by the credit bureaus, yet few of us know about the surprising history of credit reporting.

The credit bureaus as we know them today grew from small, local organizations that formed as far back as the 1800s. In contrast, modern credit bureaus market themselves as expansive repositories of consumer information that can be used for an ever-growing number of applications.

Unfortunately, the early credit bureaus were known to use unethical tactics to collect information on consumers and sell this information to businesses.

While it may seem that the problems of these early credit bureaus have been addressed by legislation such as the Fair Credit Reporting Act, the credit reporting system still has serious flaws, some of which we highlight in “What Happened to Equal Credit Opportunity for All?”

In this article, we will explore the story of how credit reporting began, including how the credit bureaus originated and evolved into what they are today, and the many scandals that have taken place along the way.

What Is a Credit Report?

A credit report contains information about a consumer’s credit history. This includes a list of current and past credit accounts, along with the age, credit limit, balance, and payment history of each account.

It also contains identifying information such as your name, address, and social security number.

This information helps lenders evaluate the creditworthiness of potential borrowers so they can decide whether to extend credit and what the terms of the loan should be.

Credit bureaus, also known as credit reporting agencies or CRAs, are the companies that gather credit-related information about consumers and distribute it to lenders—and increasingly, other types of businesses who have an interest in checking people’s credit history.

In the United States today, there are three major credit bureaus: Experian, Equifax, and TransUnion. While there are many other credit bureaus, these three companies dominate the industry.

But it wasn’t always this way. The first credit reporting organizations were a far cry from the modern credit bureaus of today, and the unsavory tactics they used to run their businesses may surprise you.

Early Credit Reporting Agencies

The first recorded group that shared credit information about consumers was the colorfully named “Society of Guardians for the Protection of Trade Against Swindlers and Sharpers,” which was founded in London in 1776. The Society produced reports for its members on the credit history of individual customers, which were often full of gossip in addition to credit information.

The earliest credit reporting “agencies” were groups of merchants who would get together to gossip about customers. Painting by Joseph Highmore, public domain.

Credit bureaus would check local newspapers for news about consumers.

Like the Society, the early credit reporting agencies were small, local organizations that were essentially groups of merchants sharing information about consumers. This allowed them to offer credit to more people and avoid lending to high-risk individuals.

These organizations were industry-specific and did not share information with each other. In 1960, it is estimated that about 1,500 independent local credit bureaus were in operation in the United States.

The bureaus didn’t just collect the information you might expect, such as name and loan information. They also gathered sensitive personal information such as marital status, age, gender, race, religion, employment history, and driving records.

The credit bureaus didn’t stop there. They checked the local newspapers for announcements of promotions, marriages, arrests, and deaths, and attached news clippings to consumers’ credit reports. They would even go so far as to ask someone’s neighbors and colleagues for testimonies about that person’s character.

Even the local “Welcome Wagon” was working undercover for the credit bureaus. This organization would surreptitiously gather information on new residents of an area under the guise of welcoming them to the neighborhood.

The “Welcome Wagon” would secretly collect information on new neighbors for the credit bureaus. Photo by John Fowler on flickr, CC BY 2.0.

The credit bureaus were focused solely on serving the local creditors that belonged to their respective organizations. As such, they typically only reported derogatory information.

Furthermore, there was no standardized way to evaluate a person’s creditworthiness. It was all based on the subjective whims and prejudices of the creditor looking at their credit file.

What’s worse is that the credit bureaus did not allow consumers to view the information that was being reported about them. There was no way for consumers to verify whether the information was correct or where it came from.

Modernization of Credit Reporting

According to the Harvard Business School paper, over the course of the 1960s, many of these small, local credit bureaus started to join together, forming networks that spanned the nation.

In 1971, the Fair Credit Reporting Act (FCRA) was passed to ensure the “accuracy, fairness, and privacy of information in the files of consumer reporting agencies.”

By establishing requirements as to the accuracy and of consumer credit files and access to their information, the FCRA was intended to protect consumers from the unfair practices that were rampant in the credit reporting industry.

The Fair Credit Reporting Act

The FCRA enacted the following rights for consumers:

Consumers must be notified if negative action is taken against them because of the information in their credit file.

Consumers must be able to find out what is in their credit file.

Consumers must be able to dispute inaccurate information and have it corrected or deleted.

Outdated information (generally more than 7-10 years old for negative information) cannot be reported.

Consumers must provide consent for employers to check their credit reports.

Consumers must have the option to request to be excluded from lists for unsolicited credit and insurance offers.

Consumers who appear on a list of prospects requested by a lender must be extended a firm offer of credit.

As a result of the passing of the FCRA, credit bureaus stopped recording events such as marriages and arrests and started focusing more on verifiable credit history information. They also started reporting positive information in addition to negative information.

In 1996, the FCRA was amended to extend additional protections to consumers, including the following:

Consumers have the right to take legal action against anyone who obtains their credit report without a permissible purpose.

Credit bureaus can be held liable for knowingly reporting misinformation.

Credit bureaus must investigate disputes within a certain period of time, usually 30 days.

Banks can share credit information with affiliates, but consumers must be given the opportunity to prohibit this sharing of their information.

The transition to computerized databases allowed some credit bureaus to expand and dominate the industry.

The advent of computer-powered databases allowed some credit reporting agencies to become more efficient and do more business, while smaller agencies that could not afford to make the change got out of the industry.

This consolidation eventually led to the domination of the market by the three major bureaus we know today.

Experian

While Experian did not officially come about until 1996, according to creditrepair.com, the story of Experian can be traced back almost 200 years.

The Manchester Guardian Society was formed in England in 1826 to share information on customers who didn’t pay their debts. This organization eventually became a part of Experian, as did a group of merchants that later formed in Dallas for a similar purpose.

These groups were both acquired by TRW, an engineering and electronics conglomerate that also launched their consumer credit reporting branch as Experian.

Experian was acquired by the British retail company Great Universal Stores Limited (GUS) and became part of their consumer credit reporting arm. In 2006, it demerged from GUS and began trading on the London Stock Exchange.

Although Experian as we know it today did not come along until after the FCRA was passed, the bureau has certainly not been free of controversy.

In 1991, a TRW investigator incorrectly reported that 1,400 people in Vermont had not paid their property taxes, which ruined the credit of those consumers. Several similar cases were discovered throughout New England.

Experian became infamous for their atrocious customer service and was hit with several lawsuits.

Later, Experian settled with the Federal Trade Commission (FTC) for operating a credit reporting scam in which consumers were led to believe they were signing up for a “free credit report” and were not told that they would automatically be enrolled in Experian’s $80 credit monitoring program.

The offending for-profit website, FreeCreditReport.com, is still in operation. As a reminder, the only site authorized to provide free credit reports as required by federal law is annualcreditreport.com.

They settled with the FTC again in 2005 for violating their previous settlement.

In 2015, Experian announced a data breach that existed for over two years and affected as many as 15 million consumers.

The bureau was then fined $3 million in 2017 for deceiving customers about their credit scores, along with TransUnion and Equifax.

TransUnion

TransUnion originally began as the holding company for a rail transportation equipment company in 1968. One year later, they entered the credit reporting industry by acquiring regional credit bureaus. The bureau has expanded steadily since then, although it is the smallest of the three major credit bureaus.

TransUnion has also been guilty of taking advantage of consumers.

Two consumers have sued TransUnion for refusing to remove inaccurate information on their credit reports.

They have also been accused of scamming consumers by not notifying them that they would be charged $18 a month for having a TransUnion account.

In June 2017, the largest FCRA verdict to date forced TransUnion to pay $60 million in damages to consumers who were erroneously included on a government list of terrorists and security threats.

Later in 2017, one of TransUnion’s websites was hijacked and made to redirect consumers to websites that attempted to download malware onto visitor’s computers.

Equifax

Equifax was started as Retail Credit Company by a grocery store owner. Photo by Charles Bernhoeft, public domain.

Equifax was started in 1898 by a grocery store owner who created a list of creditworthy customers and sold the list to other businesses. This business grew and became known as the Retail Credit Company.

The company expanded quickly throughout North America, amassing credit files on millions of Americans by the 1960s.

The Retail Credit Company developed a reputation for collecting extensive personal information on consumers and selling it to just about anyone who wanted it.

Critics accused them of reporting “facts, statistics, inaccuracies and rumors’…about virtually every phase of a person’s life; his marital troubles, jobs, school history, childhood, sex life, and political activities.”

Buyers of these reports would use them to judge the morality of individuals and avoid lending to those who they perceived as morally corrupt.

Consumers were not allowed to see their information, and many had no idea that the company had files on them in the first place.

When the company started planning to computerize their records, which would make consumer information more widely available, the U.S. Congress intervened, holding hearings that led to the Fair Credit Reporting Act being passed.

Equifax had to stop scamming consumers by lying about their identity and their motives when collecting information, among many other changes.

The Retail Credit Company changed its name to Equifax in 1975, which many speculate was a move to improve their damaged reputation after the congressional hearings.

Unfortunately for consumers, Equifax’s issues didn’t end with the Fair Credit Reporting Act. In recent years they have betrayed consumers’ trust even more egregiously.

Equifax ruined their reputation again in 2017, when their systems were breached by hackers twice, impacting hundreds of millions of consumers in the United States, Canada, and Britain.

The scam left the names, social security numbers, birth dates, addresses, driver’s license numbers, and credit cards numbers of consumers exposed for months, from May 2017 until July 2017.

Not only that, but Equifax did not disclose the breach until September of that year, giving top executives plenty of time to sell their shares of the company before going public with the announcement.

They continued to bungle their response to the breach by setting up websites that were supposed to allow consumers to determine whether they were affected by the Equifax breach but instead returned random results.

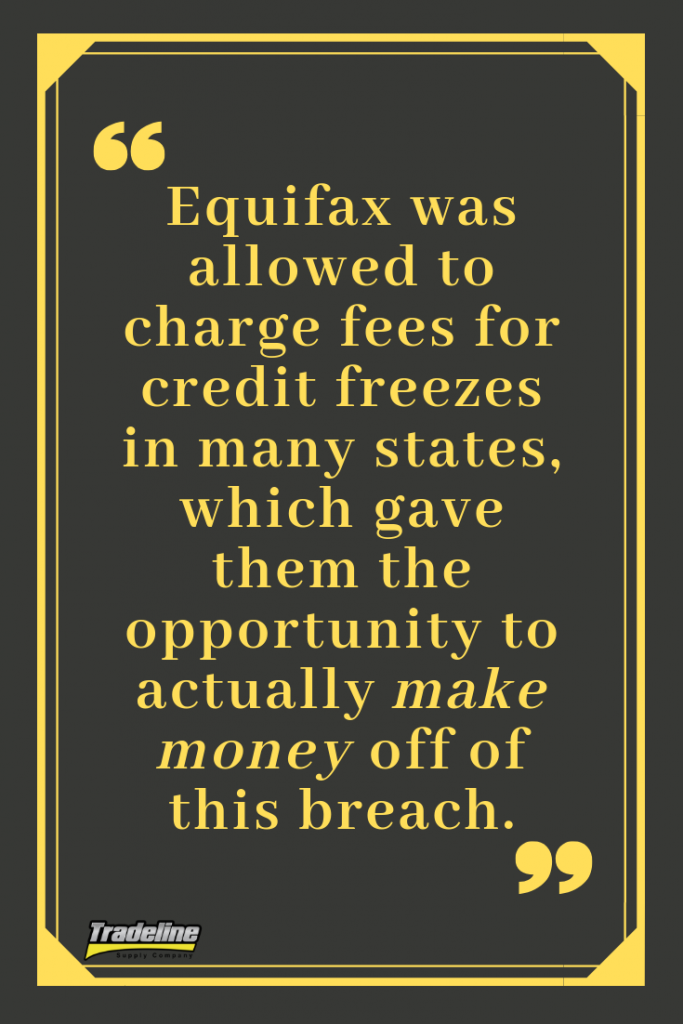

In addition, Equifax was allowed to charge fees for credit freezes in many states, which gave them the opportunity to actually make money off of this breach.

Nearly two years later, Equifax has still not been penalized or held accountable for this horrific failure in any way. In fact, they just went back to selling credit monitoring, and they are now making more money than ever.

For a fascinating in-depth investigation of the 2017 Equifax breach, listen to the podcast “Breach.”

There is virtually no end to the list of disastrous errors committed by Equifax, but here are some more of the highlights:

The bureau repeatedly tweeted a link to a fake Equifax phishing website, directing consumers to enroll in fraud prevention services at the imposter site.

Equifax left their systems vulnerable to a series of cyberattacks that affected hundreds of millions of people.

Equifax left the private data of approximately 14,000 Argentinian consumers and staff members open to anyone who entered “admin” as the username and password for one of its online portals.

The company removed its mobile apps from app stores in 2017 because they had security flaws that left them vulnerable to cyber attacks.

A website operated by Equifax exposed the salary histories of tens of thousands of people to anyone that had someone’s Social Security number and date of birth, both of which were in the hands of criminals after the security breach.

In October 2017, Equifax’s website was hacked and made to serve malware disguised as a software update, leaving visitors to the site at risk of having their computers infected by the malware.

The company has been sued hundreds of times and fined millions of dollars by the Federal Trade Commission for violating the FCRA.

Sadly, it seems Equifax has not changed for the better since their early days of selling people’s private information to anyone and everyone, since they have allowed criminals to easily access consumer data on a massive scale.

Innovis: The Fourth Credit Bureau

Many people are completely unaware that there is actually a fourth major credit bureau called Innovis. It was founded as Associated Credit Bureaus in 1970 and changed its name to Innovis in 1997. The company is now owned by CBC companies, which purchased Innovis in 1999.

In contrast to the other consumer reporting agencies (CRAs), credit reporting is not the primary function of Innovis. In fact, Innovis does not even offer credit scores.

Innovis instead serves businesses by providing “consumer data solutions” such as identity verification, fraud prevention, receivables management, and credit information. According to finance writer Sarah Cain, Innovis’ credit reports are used primarily to compile lists of pre-approved consumers to sell to lenders for marketing pre-screened offers.

Innovis also states on their website that as a CRA, they “enable” personal solutions such as credit reports, credit disputes, fraud alerts, active duty alerts for consumers in the military, credit blocks, security freezes, and opt-outs.

What Is In Your Innovis Credit Report?

Your Innovis report, like your other credit reports, contains your personal information as well as your credit history. However, they do not receive credit information from all of the same lenders that report to the other three major credit bureaus. If you pull your Innovis credit report, you may notice that some of your credit accounts are missing, particularly revolving accounts.

Your credit report will also show inquiries if any businesses have pulled your file from Innovis.

While you can’t get your Innovis credit report from annualcreditreport.com, you can order a copy directly from the company for free once a year.

Who Uses Innovis Credit Reports?

While there are some anecdotal reports of credit card companies pulling consumers’ Innovis credit reports for lending decisions, it seems that their reports are used mostly for pre-screened marketing offers. Innovis’ services are also used by companies such as cell phone service providers.

Is CBCInnovis the Same Company?

Confusingly, there is another company owned by the same parent company as Innovis called CBCInnovis. Although CBCInnovis and Innovis share similar names, they are different companies with different functions.

Unlike Innovis and the other credit bureaus, CBCInnovis does not maintain a repository of consumer credit data. Rather, it serves as a third-party company that pulls consumers’ credit reports from Experian, Equifax, and TransUnion and compiles the information into one “tri-merge” credit report. These tri-merge reports are sold to lenders such as banks and mortgage companies.

Discrimination in Credit Reporting

Unfortunately, historical discrimination is still baked into the credit system.

You might think that discrimination in the credit system is a thing of the past, left behind with the shady information-gathering tactics of the earliest credit bureaus.

Unfortunately, although discrimination is officially prohibited by the Equal Credit Opportunity Act, inequality is still rampant in the credit industry today.

Past and present discrimination against minorities in the United States affects consumers in ways that have dramatic effects on credit scores. A study by the Federal Reserve Board revealed that on average, blacks and Hispanics have lower credit scores than non-Hispanic whites and Asians, even after controlling for personal demographic characteristics, location, and income.

The credit system further burdens those who are less privileged and provides very few opportunities for disadvantaged consumers to improve their situation.

Conclusion on the History of Credit Reporting

Credit reporting agencies have a surprisingly long and sordid history. From the 1800s to today, the consumer credit reporting industry has been plagued with bias, inaccuracies, and serious security issues.

While technological advancements have allowed the credit bureaus to expand and improve, and government regulation has been enacted to protect the rights of consumers, the system is still far from perfect.

Ultimately, the credit bureaus were built to serve lenders, not consumers, and that remains their primary purpose. We are reminded of this every time consumers are harmed by the incompetent or even outright malicious actions of the credit bureaus.

Have you been affected by a credit reporting scam or a security breach? Let us know in the comments, and please share this article if you liked it!