Losing something can put you in a panic. If it’s a credit card, losing it can be especially troublesome.

A thief who steals it or someone finds it could ring up charges on your credit card, which you may have to pay some of if you don’t report it lost soon enough.

And even if you get all the money back from credit card fraud, your credit score could be temporarily hurt if a thief quickly runs up a lot of charges on your card.

Worse than that is if someone uses the information from your lost or stolen credit card to create a fake identity in your name and uses the information to open a new account in your name.

People reported losing $1.48 billion to fraud in 2018 according to the Federal Trade Commission.

The first thing you should do when realizing your credit card is lost or stolen is to call the issuer and report it missing. We’ll get into how to do that later, but the simple thing to do is to call ASAP to report it missing.

The reason is the sooner you report it missing, the more you’ll be protected from being responsible for fraudulent charges and the chance that your information can be used by an identity thief. If the credit card is canceled, a thief can’t use it to buy things or create a new card.

Under federal law, if you report a credit card as missing before it’s fraudulently used, you’re not responsible for any unauthorized charges.

However, if a card is used by a thief before you report it missing, you could be responsible for some of those charges. The maximum liability amount is $50 under federal law. Some credit cards offer zero liability.

So if your missing card is still used after you report it missing, you won’t be liable for the charges you didn’t authorize. If your card wasn’t stolen but your credit card number was, you aren’t liable for any unauthorized charges.

How to Report a Missing Credit Card

Your credit card statement has instructions on how to report a missing card. Most companies have 24-hour, toll-free numbers. If your spouse has the same credit card, the phone number will be on the back of their card.

Call your issuer as soon as you realize your card is missing. Even if you think you might have misplaced it, you can still call your credit card company and ask it to suspend charges immediately but temporarily until you can determine if the card is really missing or if you’ve left it in the car or find it elsewhere.

Once you’ve determined that the card is gone, file a report by phone and follow the credit card company’s instructions. Also follow up with a letter to the company, providing your account number, date you noticed the card missing, and the date you filed the report.

You should check your card statement carefully for transactions you didn’t make. Report them to your card issuer as quickly as possible.

After you’ve reported a missing card, your card issuer will send you a new card, usually within a few days and sometime overnight.

If you have automatic payments tied to your credit card, such as for a phone bill, call your creditors or go online and update your accounts.

What To Do If You Lose Your Debit Card

If you lose a debit card, the consequences can be a lot worse, so you need to call your bank as soon as possible to report it lost or stolen.

Debit cards, which pull money immediately out of your checking account when used, must be reported missing within two business days of learning of their disappearance so that your liability is limited to $50.

Longer than that and up to 60 days after your next bank statement is sent to you, and you’re responsible for up to $500 in losses. Wait more than 60 days after your statement is sent to you, and all losses are your responsibility.

Thieves can quickly drain accounts linked to debit cards. Even if you quickly report the card lost, it can take awhile to get your money back from the bank.

Other Hassles of Lost Credit Cards

With the $50 liability limit set by federal law on missing credit cards, you may assume it’s OK not to report it missing. Not true. If you don’t report it missing, other problems could crop up.

Thieves who steal credit cards often start using them as quickly as they can so they can buy things before the card is canceled by the bank. But if it’s not reported missing soon, they can keep ringing up charges that you’ll have to dispute with your credit card company.

If you have a good credit card company, they’ll notice the fraudulent charges and alert you immediately. But if more purchases accumulate, you’ll spend more time trying to fix things.

A lot of fraudulent charges could also hurt your credit score temporarily. Once the fraud is found and resolved, your score should return to normal.

Retirement should be filled with plenty of carefree days, peppered with a few bucket-list-worthy adventures. Headaches, such as student loans, ideally should be long gone. But increasingly, some retirees are wondering how they’re going to pay the utilities or the … Continue reading →

Christian Assembly Church in Eagle Rock, California, raised $US50,000 to wipe out more than $US5 million in medical debt through the organisation RIP Medical Debt. RIP Medical Debt works with private foundations and donors to help people pay off debt … Continue reading →

TPG’s executive editorial director Scott Mayerowitz discusses the holiday season’s top credit cards, airlines and the importance of using your points. Americans appear to be off to a good start financially in 2020 – as many are set up well … Continue reading →

December 20, 2019 • 4 min read by Jeanine Skowronski0 Comments Getting a call from a collection agency looking to recoup an old debt you owe is more common than you think. A lot of people have to field debt collection calls during holiday … Continue reading →

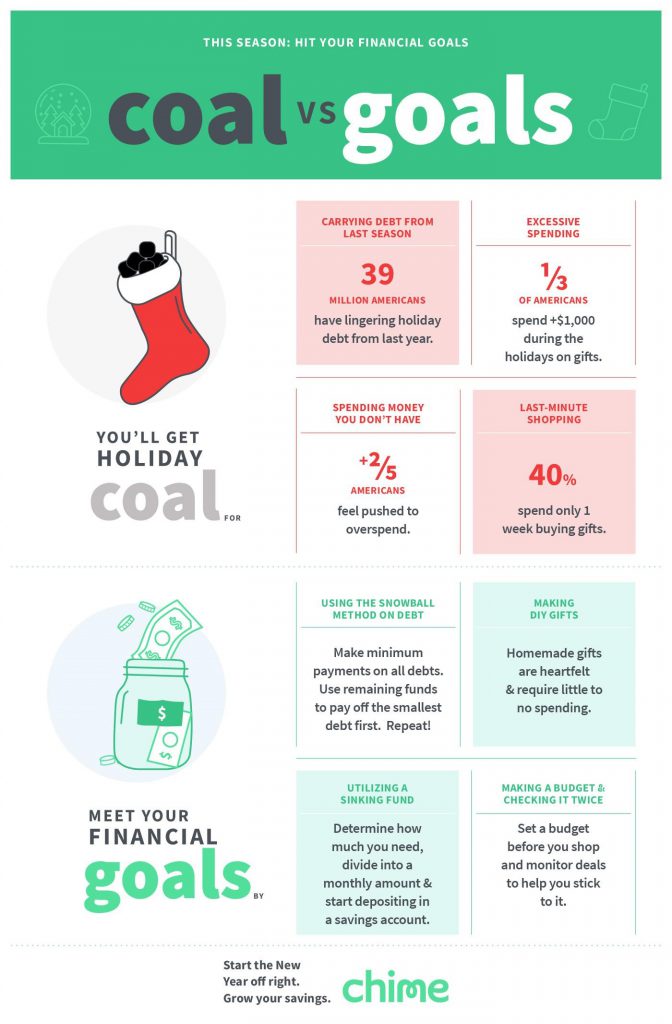

In 2018, over 39 million Americans had lingering debt from the previous holiday season—not only were they in debt, but they were still paying it off a year later. If you want to avoid falling into the same trap, you need to develop a financial plan heading into this holiday season. This means keeping track of yourself and your spending, as well as implementing some cost-saving measures. Here are three ways that you can avoid acquiring debt this holiday season.

Set a Spending Limit

Before you even begin to budget for different gifts, you need to determine your absolute spending limit based on your personal finances. Review your account balances and determine how much can you pull from these accounts without risking going into debt. The only one that can hold you to this spending limit is yourself. You must be disciplined and maintain the willpower to not exceed this limit.

Once you have set your spending limit, you can then decide how you will break it down between gifts, food, parties, etc. Rather than working in dollar amounts, try to turn your budget into percentages using an online budget calculator. For example, 50% can be spent on gifts for relatives, 25% on friends, and another 25% on food. This gives a more accurate representation of how much you can spend on various items, rather than overspending initially and then having to cut back later.

Avoid Overdraft Fees

One way to help you stay in line with your spending limit is by making purchases with a debit card, rather than your credit card. This way, you will be pulling from an account with money already in it. If you pay with a credit card and don’t have the funds to pay it back, you’ll rack up interest and make the debt worse. However, if you’re not careful with a debit card and overdraw your account, many banks will charge you an overdraft fee.

An average overdraft fee is roughly $34 and Americans spend roughly $250 on these fees annually—think of all the additional gifts you could buy with that money! Luckily, some online banks will let you overdraw your account without any charge, which could save you a lot of money around the holidays. Some accounts, like Chime Bank, even let you overdraw up to $100 without a fee and simply subtract it from your next deposit.

Take Time to Comparison Shop

Even if you miss or pass on shopping holidays like Black Friday and Cyber Monday, you should still spend time researching the best deals. Prices can fluctuate a lot around the holidays, so it’s important to check multiple stores—both online and brick-and-mortar—to find the best deals. Not only should you compare prices, but you should search for coupon codes and promotional sales as well.

While the price may be higher at one store, oftentimes you can find better discounts and factor in shipping prices to get an even better deal. For example, stores like Best Buy and Bed, Bath & Beyond will price match with Amazon. This means that you can get these products cheaper in person if Amazon doesn’t offer free shipping.

If you’re willing to do your due diligence while shopping and stay committed to your spending limit, you should have no problem making it through the holidays without tacking on additional debt.

Check out this fun infographic on what behaviors will earn you coal and what actions you can take instead to reach your financial goals this season!

Heading into the new year, it appears that the credit market will be in good shape, according to the TransUnion 2020 Credit Forecast. Among the findings, TransUnion reports that serious delinquency rates will either drop or remain stable for auto … Continue reading →

Resolving a circuit split, the U.S. Supreme Court (the Court) recently held that the Fair Debt Collection Practices Act’s (FDCPA, 15 U.S.C. § 1692) statutory language means what it says: the statute of limitations period for an FDCPA claim begins … Continue reading →

There’s never a bad time to start building good credit, but there is definitely a good time to start: as early as possible. The earlier someone starts building credit, the easier it will be to seek credit as an adult. The question is: at what age can you start building credit?

Whether you want to start building your own credit or whether you want to help your child get a head start on preparing for their financial future, this article is for you. We answer the questions of when you can start building your credit, how to build credit for a minor, and how to build your child’s credit.

Why You Should Start Building Credit Young

Obviously, most children and teenagers don’t have access to credit cards or other credit products, for good reason. However, this doesn’t mean that teens cannot or should not build credit. In fact, quite the opposite is true.

Let’s look at an example to understand why it’s important to start building credit even before turning 18. If you’re an adult and you’ve never used credit before, but you now need an auto loan, what do you think is going to happen when you go and apply for a loan?

Since you don’t have a credit history, chances are, you’re probably going to get denied. If you do somehow get approved for an auto loan with no credit, it’s likely going to have a very high interest rate since you will be perceived as a risky borrower.

The moral of the story is that you can’t wait until you need credit to start thinking about building credit. You need to start building up a positive credit history early on so that you can have that good credit to rely on when you eventually end up needing it.

Beyond the issue of having access to credit when you need it, having good credit may also be important when entering the workforce. Many employers conduct background checks and check the credit reports of prospective hires, and having a solid credit history will reflect positively on applicants.

Having already established good credit will also come in handy when shopping for insurance, applying to rent a home, setting up utilities, and maybe even buying a cell phone plan. All of these industries typically conduct credit checks on applicants before getting into business with them.

How Do You Start Building Credit?

To build credit, of course, you need to use credit products. This is why many people wait until they are well into adulthood to try to start building credit, which, as we just learned above, is a mistake because it can hold you back when you actually need to get credit.

However, we all know how difficult it can be to get approved for credit when you don’t have yet have a credit history that shows creditors that you can manage credit responsibly. Lenders don’t want to take on the risk of lending to someone whose future behavior is hard to predict.

Secured credit cards, which require a security deposit as collateral, can be one way to start building credit.

So how do you start building your credit without a credit history? One option is to apply for a secured credit card, which involves putting down a security deposit as collateral against the credit limit of your card. Lenders can issue these cards to consumers with no credit without taking on as much risk since they can keep the deposit if you default on payments. [Disclosure: This article contains affiliate links.]

Another strategy is to apply for a credit-builder loan, which works in the reverse order of a traditional loan: first, you make all the monthly payments toward the balance of the loan; then, once you have finished making the payments, you receive the loan disbursement.

Since you have already fronted the money, lenders don’t have to face the risk of you not being able to pay back the loan. Because of this, as long as you have enough income to make the monthly payments, your chances of getting approved for a credit-builder loan are very high.

There’s an easier way to start building credit, though. If you can’t get approved for any primary accounts on your own, or if you want a “shortcut” to building credit without having to wait for your primary accounts to age, you can build credit fast by piggybacking on someone else’s credit.

Piggybacking simply means becoming associated with someone else’s credit account for the purpose of building credit. There are three ways to piggyback, which you can also see in our infographic:

Get a cosigner or guarantor who can be held responsible for the debt if you cannot pay it.

Open a joint account with someone who has good credit and can help you get approved for the joint account.

Become an authorized user on someone else’s seasoned tradeline that is in good standing.

The first two of these three piggybacking methods involve opening new primary accounts, which means you have to wait a few years for the accounts to gain seasoning before they start to help your credit in a more significant way.

On the other hand, piggybacking as an authorized user means you can be added to an account that already has plenty of age and on-time payment history. That’s why it’s one of the most convenient ways to start building credit fast.

How to Help Your Child Build Credit

Teach your child about credit before they get a credit card so they don’t make the mistake of getting deep into debt.

Unfortunately, financial literacy is usually not emphasized in schools, so the responsibility of educating children about credit and helping them build credit falls primarily to parents and guardians.

It’s important to not only know how to help build your child’s credit but also to teach them the basics of financial literacy so that they will one day be able to manage their finances and their credit on their own.

Lay a solid foundation by teaching them about budgeting and saving. If your child is old enough to work, that can be a good opportunity to see how they manage their income.

Then you can move on to the world of credit. Your child needs to have an understanding of how credit works before getting a credit card or they could be headed for disaster.

In a survey of college students conducted by U.S. News in August of 2019, about 35% of students surveyed said they were not taught about fundamental financial topics before getting a credit card. A lack of understanding about how credit works and how to use it responsibly can easily lead to getting deep into debt and a lifetime of financial troubles.

In the same survey, 13% of students said they had over $8,000 in credit card debt, and almost 23% said they didn’t even know how much credit card debt they had. No one wants that to happen to their child, so make sure your kid knows how to use credit cards properly before they get one.

But beyond teaching your child the fundamentals of credit, can you build your child’s credit even before they get a credit card or loan of their own?

How to Build Your Child’s Credit Score by Piggybacking Credit

While helping them learn the ins and outs of the credit system, it’s also smart to help them get a head start on actually building credit via credit piggybacking, which means becoming associated with another person’s credit account.

If you have good credit, consider adding your child at an early age as an authorized user to one or more of your credit cards that are in good standing. If they’re not yet ready to use the account responsibly, you don’t necessarily have to give them access to a credit card. Alternatively, if you want to let them use a credit card, some credit card issuers may allow you to set spending limits for authorized users.

Piggybacking credit can help your child build credit early in life.

Being an authorized user on the account will still help them even if they don’t have spending privileges on the card. The positive payment history of that account will usually be reported on the authorized user’s credit profile, which can help kick start their credit score.

Unfortunately, according to the U.S. News study, about 75% of the college students that participated in the survey said they did not become an authorized user on someone else’s account before getting their own credit cards. That means they likely missed out on the lower interest rates and other perks that come with having an established positive credit history.

This statistic is not surprising. As we learned in our article, “What Happened to Equal Credit Opportunity for All?” equal credit opportunity is sadly not a reality in our country. Wealth disparities and historical discrimination prevent many Americans from being able to establish good credit and get ahead in life.

Those with wealth and financial education commonly used the authorized user piggybacking strategy to help their children build credit, while at the same time there are many young people who don’t have parents or loved ones that can help them establish credit. The tradeline industry helps to address this problem by providing access to authorized user tradelines to all consumers.

It’s clear that the authorized user strategy is an ideal way to help your child build credit. But when can you actually start building credit? Is there a minimum age requirement to be an authorized user? Can you start building credit before 18, for example?

At What Age Should You Start Building Credit?

It can be difficult for young adults to get approved for a credit card on their own since credit card issuers are required to check applicants’ income before issuing them credit. However, by using the authorized user credit piggybacking strategy, young people can start building credit earlier than you may think.

Minimum Age for Authorized User on Credit Card

Many credit card issuers have no minimum age requirement for authorized users.

A survey by creditcards.com revealed that half of the major credit card issuers surveyed, including Bank of America, Capital One, and Chase, had no minimum age requirement for authorized users! That means that with many of the most common credit cards, you can add your child as an authorized user at any age.

Credit card companies that do have age requirements, such as American Express, Barclays, Discover, and US Bank, typically impose a minimum age limit that is between 13 to 16 years old.

Check with your credit card issuers to see what the minimum age requirement is for authorized users on your cards.

In addition, check with your credit card issuers to see whether they report authorized user information to the credit bureaus since not all banks do. If you’re purchasing a tradeline, however, you don’t have to worry about that, since all of the banks we work with do report to all three major credit bureaus.

Conclusion

It’s a smart idea to help your child build credit early so they can start their adult life on a financially sound footing. If you have good credit yourself, the easiest and fastest way to build your child’s credit is by adding them as an authorized user to one or more of your credit cards that have a perfect payment history.

Kids can become authorized users at any age with some credit cards, while there is a minimum age requirement of 13 to 16 years with other cards. Check to see what your bank’s policy is.

Unfortunately, many people do not have access to this credit-building strategy. If you are one of those people, consider purchasing a seasoned tradeline when it comes time for your child to start establishing a credit history.

It’s never too early to start building good credit!

Did your parents teach you about credit at a young age? How do you plan to help your child build credit? Share your thoughts below!