A majority of voters support congressional investigations into Secretary of Education Betsy DeVos’ handling of student debt programs, according to the results of a new poll, which exposes how deeply unpopular the Trump Cabinet member is across the country. DeVos has … Continue reading →

Worried about your debt? Consider this: The U.S. is $23 trillion in the red. Today, the country owes over four times more than it did in 2000, when the national debt stood at around $5 trillion. How did we get … Continue reading →

Congressional leaders and Democratic presidential candidates are proposing huge investments in undergraduate education, including tuition-free public college and larger grants for students from low-income families. Although those policies would reduce the need to borrow for certificates and associate’s and bachelor’s … Continue reading →

Our own Bruce McClary, VP of Marketing and Rebecca Steele, CEO joined Richard Levick on the ‘What’s Working in Washington’ podcast to talk about about consumer debt and the increasing problems consumers are facing when trying to find help. Consumer unsecured debt continues to rise and is currently sitting at $1.5 Trillion.

Rebecca Steeles says, “The first step is always the hardest to take, but it’s important to move past the shame and take it!” In earlier days, there was a sense of shame in taking on debt and people avoided it, now it’s so common, everyone has it and feels it’s ok and it’s more important to buy things to show people you love them, like for example the holidays. Statistics show that the average consumer racked up $1300 on their credit cards just for the holiday season. While one in ten are still carrying debt from the 2018 holiday season! If you make minimum payments on this with an average of 18% interest, it will take six years to pay it off.

On top of taking on debt, American consumers also report not having at least $400 to cover an emergency, which in turn leads them to going further into debt if an emergency arises. People on average have five major credit cards. It’s hard to get out of debt once you are in it. When people are desperate they need to know where to turn because it’s not just one creditor, it’s on average at least five and when they aren’t able to take care of it themselves, predators come out from all directions.

Here more about the dangers of the “wild wild west” of the debt relief industry at the links below, what we mean by predatory, and what consumers should do instead at the links below:

Nonprofit credit counseling can help you figure out the right option for you and how to navigate the landscape of debt relief options. It gives you a safe space to deal with your debt, with a nonjudgmental ear. They are going to help you with a budget, do a thorough review of your complete financial picture and provide a plan customized to you. Credit counseling is typically free. They are there to advocate for you and ensure that you are better prepared to get out and stay out of debt.

“We are not working for the banks, we are working for the consumer,” said Rebecca Steele, “a lot of banks are working with us and we can work with them on your behalf.”

Two of Fresno’s most prominent eviction attorneys are facing lawsuits from evicted tenants who say the lawyers should be ordered to stop their debt collection practices. Representing three tenants in two separate complaints, Central California Legal Services accused attorneys Steve … Continue reading →

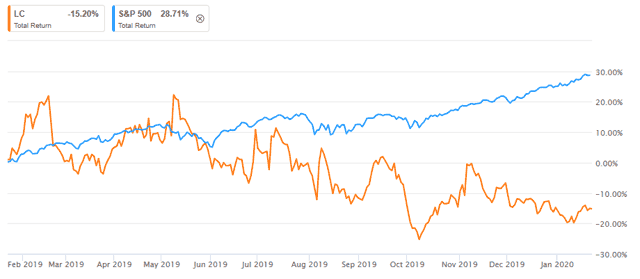

Summary LendingClub originates unsecured personal loans it then sells to investors. Credit losses on its loans are steep and it looks like the company is worse than banks at underwriting. The stock is relatively cheap, which compensates for most of … Continue reading →

The worst thing that can happen after you buy tradelines is not seeing your tradelines post to your credit report. Hopefully, your tradeline company offers a money-back posting guarantee, but of course, it’s better to have your tradelines post successfully the first time around.

Fortunately, there are a few things you can do to make sure everything goes smoothly when you buy tradelines. Here are our pointers on how to get tradelines to post.

1. Remove all fraud alerts and credit freezes from your credit report

Fraud alerts, credit freezes, and any other types of blocks on your credit file prevent new information from being added to your profile. This includes authorized user tradelines. Therefore, if you have a credit freeze, fraud alert, or some other type of block on your credit file, your tradelines will not post.

Before buying tradelines, make sure to contact the credit bureaus to remove any fraud alerts, credit freezes, or other blocks on your credit report so that new AU tradelines will not be blocked. Ideally, it’s best to wait about 30 days after removing all blocks to make sure that your credit file is completely clear.

2. Plan ahead and purchase your tradelines in advance

Try to plan your tradeline purchase ahead of time so you don’t miss the purchase by date.

Each of our tradelines has its own reporting period and corresponding “purchase by” date, which is the date by which you must purchase the tradeline in order for it to report on time. The purchase by date is typically 11 days before the reporting period begins in order to allow enough time to process your payment and add you as an authorized user to the tradeline.

Therefore, if you wait too long and the purchase by date has already passed for the current month, your tradeline may not post until the next reporting period a month later.

For this reason, it’s best to plan your purchase ahead of time so that you can be sure to purchase your desired tradelines before the purchase by date. Those who wait until the last minute to buy tradelines are limited to the tradelines with the soonest purchase by date.

Alternatively, some people are in such a rush to get tradelines that they don’t even pay attention to the purchase by date, and they don’t realize that they may have just purchased a tradeline that is not due to post for another month.

In order to ensure that your tradelines post in a timely manner, make sure to purchase them before the purchase by date.

3. Consider buying more than one tradeline as a safety precaution

While we offer a money-back guarantee in the case of a non-posting, unfortunately, non-postings inevitably do happen from time to time due to incorrect reporting by the banks and credit bureaus, which we have no control over.

If you need your tradelines to post within a specific time window and cannot wait for an exchange to be processed in the event of a non-posting, it is safest to hedge your bets by buying more than one tradeline.

Additionally, when buying multiple tradelines for this reason, you may want to choose tradelines from a few different banks. That way, if there is a problem with one particular bank, it will not prevent the rest of your tradelines from posting.

4. Choose a tradeline company that only works with the best banks and has the highest posting success rate

When it comes to tradelines posting, not all banks are equally effective. Some banks report authorized user accounts much more reliably than others. In fact, we only work with a select few banks that we have rigorously tested and found to have the best posting success rates.

Almost all the other tradeline companies out there work with many more banks than we do, which may sound like a good thing, until you consider the fact that most of these banks don’t report authorized user tradelines very well. Therefore, if you buy tradelines from these companies, there is a much higher chance of your tradelines not posting.

You’ll want to stick with the most reliable banks and tradeline companies to minimize your risk of a non-posting occurring.

5. Avoid buying tradelines from banks you may be blacklisted from

Sometimes, banks may “blacklist” certain customers that have a derogatory history with them, such as bankruptcies or collection accounts. If you have been blacklisted from working with a particular bank, this could prevent any tradelines from that bank from posting to your credit file, so you would want to choose tradelines from other banks to ensure successful posting.

If you are not sure about your status with a bank, but you have a collection or bankruptcy with them, it’s a good idea to avoid that bank as a precaution.

6. Use the correct address that is on file with the credit bureaus

Make sure to use the correct address when ordering tradelines.

The banks and credit bureaus use certain data points to verify the identity of the authorized user, and one of the most important data points is the AU’s address.

If you do not use the correct address that you have on file with the credit bureaus, they may not be able to match the tradeline with your credit profile, and this can prevent the tradeline from posting.

Before buying tradelines, check your credit report with each credit bureau to verify that they have your correct address on file, and be sure to use this same address when placing your tradeline order.

7. Avoid “address merging”

As we mentioned, most tradeline companies sell tradelines from many different banks, including banks that don’t report AU data very well. Because tradelines from those banks don’t post well, most companies engage in a questionable practice called “address merging” to try to get the tradelines to post more often.

Address merging is the practice of falsely claiming that the authorized user lives at the same address as the primary cardholder. This allows the account to be matched up to the AU using the shared address as an identifying data point.

While this strategy may improve their posting rates, we do not recommend this dangerous tactic, because lying about one’s address for financial gain is considered fraud and it could get you in trouble with the law.

It is important to be aware that some companies may be doing this without your knowledge and some may not even realize that they are getting their clients involved in fraud. When choosing a tradeline company, keep in mind that if they sell tradelines from a lot of different banks, it is likely that they participate in address merging.

Instead of getting involved in the risky practice of address merging, follow all of the other steps in this article to increase the odds of your tradelines posting as much as you can.

8. Triple-check your order information for errors before submitting your order

Before finalizing your purchase, go over your information again and make sure it’s free of errors.

While your address is a particularly important data point when it comes to the credit bureaus, it’s also important to make sure the rest of your personal information is correct when placing your tradeline order.

Unfortunately, some people submit their orders with typos or misspellings, and each error increases the odds that something could go wrong.

For example, sometimes people even enter their own name incorrectly! Obviously, if the name you provide with your order is not your actual name, then that can definitely increase the chances of your tradeline not posting because the credit bureaus may not be able to match the tradeline to your credit file.

There’s nothing more frustrating than having a non-posting occur simply due to a preventable user error. To ensure this doesn’t happen to you, before placing your order, look over your information and double- and triple-check it for accuracy.

We hope these tips on getting tradelines to post were helpful to you! Let us know what you think by leaving a comment below.

New York Gov. Andrew Cuomo has proposed a bill to license consumer debt collectors. The proposal comes as part of the governor’s 2021 “budget bill” and was introduced on Jan. 21. A copy is available here. The bill proposes an … Continue reading →

The United States Court of Appeals for the Sixth Circuit recently held that the anxiety felt by a debtor upon receiving a dunning letter was insufficient to bring a claim under the Fair Debt Collection Practices Act (“FDCPA”). See Buchholz … Continue reading →

BY MARY ELLEN KLAS Matt Holland, 32, of Spring Hill is one of two million Floridians who have had their driver’s license suspended because they couldn’t afford to pay the debt. He lost his license when he couldn’t pay $3,000 … Continue reading →