Randal K. Quarles, vice chairman for supervision of the Federal Reserve Board of Governors, said the Fed will be looking at all of the effects the Current Expected Credit Losses accounting standard has on the industry and on individual institutions. … Continue reading →

Here’s a number that may shock you: about one in five American adults do not have a credit score.

About 26 million consumers are what the Consumer Financial Protection Bureau calls “credit invisible,” which means they don’t have any credit history. Another 19 million consumers have credit records that cannot be scored by a commonly used credit scoring model.

Added together, that means 45 million consumers in our country—nearly one in five adults—lack a credit score.

Without a credit score or a sufficient credit record, it can be extremely difficult to navigate modern society. Credit scores indicate a consumer’s credit risk and therefore serve as the basis for most lending decisions, along with income. It can be difficult or even impossible to obtain credit without one.

Credit scores may also be used by landlords to evaluate prospective tenants, by insurance providers to determine rates, and by utility companies when assessing deposits. Employers may pull prospective employees’ credit reports in order to make hiring decisions.

Therefore, consumers who are credit invisible or credit unscorable may face serious challenges in obtaining credit, housing, insurance, utilities, and employment.

Unfortunately, but perhaps not surprisingly, the problem of credit invisibility is concentrated among certain demographics of consumers.

In this article, we’ll address who is most impacted by credit invisibility and the consequences of lacking credit history. In addition, we will discuss potential solutions to this issue and explain how tradelines can help consumers become credit visible.

Defining Credit Invisibility and Unscorability

The Consumer Financial Protection Bureau published a report on credit invisibility in 2015 in which the Bureau determined how many Americans are lacking credit histories.

For the report, they analyzed a nationally representative data set containing the anonymized credit reports of nearly 5 million consumers. The CFPB purchased these anonymized credit reports from one of the major credit bureaus.

By subtracting the number of credit records in a census tract from the total number of adults living in the census tract, they were able to estimate the number of credit invisible consumers in each census tract.

Nearly 20% of consumers in the U.S. do not have a credit score due to a lack of credit history.

Overall, the CFPB found that more than 80% of the adult population in the United States (188.6 million consumers) have credit records with at least one of the major credit bureaus that contain enough information to be scored by the commercially available credit scoring model used for the CFPB’s research.

In contrast, 8.3% of adults have credit records that cannot generate a credit score using this credit scoring model. This group of 19.4 million consumers is divided about equally between consumers whose credit reports do not contain enough information to be scored (“insufficient unscored”) and consumers whose credit history is not recent enough to be scored (“stale unscored”).

This leaves 11% of the adult population who are completely credit invisible, meaning they do not have a credit record at all with any of the major credit reporting agencies.

What Are the Consequences of Being Credit Invisible or Unscorable?

The credit reporting agencies and credit scoring companies have been extremely successful in marketing their products to other industries. As a result, credit checks are now a standard procedure in many essential aspects of modern life. This means that being credit invisible can have devastating consequences for consumers.

Credit May Be Unattainable or Very Expensive

The “credit catch-22” is that in order to qualify for credit, you must already have a history of using credit. Lenders want to see a pattern of responsible borrowing before they take the risk of extending you credit.

Therefore, the obvious problem with having no credit history or minimal credit history is that it bars access to mainstream credit products such as loans and credit cards.

This lack of access to conventional credit options leads credit-invisible and unscored consumers to turn to “alternative financial service providers” (AFSPs), which include businesses such as payday lenders, pawn shops, and check-cashing stores. Unfortunately, services provided by AFSPs typically come with much higher costs than traditional credit products offered by banks.

Consumers who are credit invisible may turn to high-cost AFSPs such as payday lenders if they cannot access traditional credit products.

As most consumers do, those who are credit invisible or unscorable have legitimate credit needs, but unfortunately, their options are usually limited to high-cost AFSPs.

Housing May Be Difficult to Find and More Costly

Renting a home almost always involves a credit check for the prospective tenants. Often, landlords will simply reject applicants who do not have a credit record.

Some landlords may accept tenants who don’t have any credit history, but since it’s financially risky for them, they will likely charge more for the deposit or ask the tenant to prepay multiple months of rent.

Utility Providers and Wireless Carriers May Require a Deposit

Providers of utilities such as gas, electricity, water, trash, internet, and phone service also typically conduct credit inquiries on consumers. Knowing your credit score helps these companies judge how likely they think you are to pay your bills on time.

If you don’t have a credit score, they can’t make that judgment with confidence. To hedge their bets, the utility companies may ask you to pay a larger deposit upfront.

Insurance Could Be More Expensive

Credit scores are often considered as a factor when insurance companies decide on your rates for auto insurance as well as homeowner’s insurance, according to credit.com. If they can’t use a credit score to help determine your rate, they may end up charging you more.

Who Is Most Likely to Be Credit Invisible or Unscorable?

As you may remember if you’ve read our article on the topic of equal credit opportunity, the likelihood of being credit invisible isn’t the same for all consumers. In fact, there are strong correlations between credit invisibility and race, age, geography, and income.

Black and Hispanic Consumers Are More Likely to Lack Credit History

The CFPB discovered that consumers who are Black and Hispanic are more likely to be credit invisible or unscorable.

Compared to consumers who are White or Asian, Black and Hispanic consumers are more likely to be credit invisible or to have credit records that cannot be scored, according to the CFPB’s report.

Only 9% of White and Asian consumers are credit invisible, compared to about 15% of Black and Hispanic consumers. Similarly, only 7% of White adults have unscorable credit records, in comparison to 13% of Black adults and 12% of Hispanic adults.

The CFPB observed that this pattern was consistent across all age groups, which demonstrates that the differences between racial groups are established early on and never go away.

Credit Invisibility Is Correlated With Age

Younger consumers are far more likely to lack credit history than older adults. The CFPB report states that the vast majority (80%) of 18 to 19-year-olds are either credit invisible or have unscored credit records.

For the 20 to 24-year-olds age group, less than 40% are credit invisible or unscored. After the age of 60, however, this percentage begins to increase with age, although it’s not clear exactly what causes this effect.

Because credit history is gradually established over the course of one’s life, it makes sense that credit invisibility and unscored credit records would be more prevalent among young adults.

Income May Affect the Ability to Acquire Credit History

The CFPB found a strong correlation between income and having a credit record that can be scored. In low-income neighborhoods, nearly 30% of consumers are completely credit invisible, while another 15% are unscorable. In total, nearly half of consumers in low-income areas either have no credit history at all or not enough credit history to generate a credit score.

In contrast, in higher-income neighborhoods, only 4% of consumers are credit invisible and an additional 5% have credit files that cannot be scored.

These results aren’t particularly surprising. Income is often even more important than credit score when it comes to qualifying for credit. Even without having any credit history, a consumer with a high income will likely find it easier to qualify for credit than a low-income consumer and thus is more likely to open credit cards or take out loans than a low-income consumer.

Rates of credit invisibility are especially high in low-income neighborhoods.

On the other hand, since low-income consumers may have difficulty accessing traditional sources of credit, they may turn to AFSPs such as payday lenders, which typically do not report to the credit bureaus. This hypothesis may help partly explain why there is such a stark difference in the likelihood of credit invisibility between higher-income and lower-income consumers.

When consumers in low- and moderate-income neighborhoods do become credit visible, according to the CFPB, they tend to make the transition later in life than consumers in middle- and upper-income neighborhoods.

In addition, the CFPB report on “Becoming Credit Visible” concluded that consumers who reside in low-income neighborhoods are three times as likely than consumers in high-income neighborhoods to first acquire credit history from non-loan items such as collection accounts or public records (27% of low-income consumers versus just 8% of high-income consumers).

In contrast, consumers in upper-income neighborhoods are much more likely to start their credit records by opening credit cards.

Since the non-loan credit products are generally derogatory items like collections, this statistic suggests that low-income consumers are far more likely to start off their credit history with bad credit. The negative marks could hinder these consumers from being able to qualify for credit for a long time, which means they would likely have few, if any, opportunities to improve their credit profile with on-time payments toward loans or credit cards.

Geographic Regions of Credit Invisibility

Another CFPB report, this one from 2018, looked at geographic patterns in credit invisibility, such as differences between urban and rural areas as well as the problem of “credit deserts.”

Credit Deserts

Credit invisibility tends to be more common in rural areas.

A “credit desert” is generally defined as an area that lacks access to traditional financial service providers. However, they may have access to AFSPs such as payday lenders.

In these areas, rates of credit invisibility may be higher due to a lack of access to traditional sources of credit.

Urban vs. Rural Areas

The highest proportion of credit invisible consumers is found in rural areas, even in upper-income neighborhoods. This may be related to a lack of access to the internet in rural areas.

What Is Being Done to Solve Credit Invisibility?

Credit invisibility in America is a serious problem that is not going to be solved overnight. It’s going to take overarching structural changes to address the root causes of credit invisibility and credit inequality.

Let’s explore the potential solutions currently being researched by the U.S. government and by the credit scoring and reporting companies to address credit invisibility and credit inequality.

Government Programs to Support Credit Access

In the CFPB’s Annual Financial Literacy Report for 2019, the Bureau described their efforts to support inclusion and serve historically underserved communities by assisting local governments that are working to address credit invisibility in their cities.

These municipal programs typically focus on helping consumers build good credit by providing consumers with credit education, credit services, and credit products.

The CFPB worked with four cities in the fiscal year 2019 (Atlanta, Georgia; St. Louis, Missouri; Shawnee, Oklahoma; and Klamath Falls, Oregon), so it appears that government efforts to combat credit invisibility thus far have been localized and small-scale.

Alternative Credit Data

Using alternative data, consumers may be able to get credit for their rent and utility payments.

Alternative credit data is data derived from sources other than traditional credit reporting information. This may include data from ASFPs, utility payments, rent payments, full-file public records, and financial information that consumers can choose to share, such as bank account information (known as “consumer-permissioned data”).

While alternative data does have the potential to help millions of consumers become credit visible, for a majority of them, that may not be a good thing. FICO’s preliminary research using their alternative data scoring model showed that two-thirds of newly scored consumers ended up with a score that was below 620, which is considered bad credit.

Having bad credit can be even worse than having no credit, so for these consumers, the use of alternative data would hurt more than it helps.

Furthermore, the National Consumer Law Center has argued that the negative effects of such a credit scoring system would disproportionately impact people of color and low-income consumers.

Alternative data may represent a possible solution to credit invisibility, but it should be implemented in a way that does not simply perpetuate and amplify the credit inequality that consumers already struggle with.

How to Become Credit Visible

It’s clear that credit invisibility, lack of access to credit, and inequality in the credit system are not going away anytime soon.

For now, however, we can at least discuss some strategies that individual consumers can use to start building credit and transition from being credit invisible to credit visible in a way that sets them up for success.

Becoming Credit Visible Through Credit Piggybacking

It’s incredibly difficult to get approved for a primary account when you don’t have any credit history to show lenders that you can be trusted. However, you can start to build credit history even without opening a primary account by piggybacking on someone else’s credit.

Piggybacking on another person’s credit can help consumers transition out of credit invisibility.

Credit piggybacking is when you become associated with someone else’s credit record for the purpose of building credit. This is actually a fairly common way for consumers to start establishing credit.

In “Becoming Credit Visible,” the CFPB noted that about 15% of consumers opened their first credit account with a co-borrower, while another 10% first created their credit record by becoming an authorized user on someone else’s tradeline. This means that in total, about one in four consumers initially gain credit history with the help of someone else via credit piggybacking.

There are three main ways to credit piggyback.

1. Get a Cosigner or Guarantor

When you can’t get credit on your own, having someone who has good credit who can vouch for you as a cosigner or guarantor can make a huge difference in your chances of being approved for credit.

However, it can be difficult to find someone to take on this role, since it not only requires someone with good credit but someone who would be willing to be on the hook for your debt if you cannot repay it.

2. Open a Joint Account With Someone

A joint account is an account that you share with another person. Both parties have access to the account and both people can be held responsible for the debt.

If you know someone with good credit who is willing to open a joint account with you, their positive credit history can help the two of you get approved, similar to getting a cosigner or guarantor. Since both parties jointly share responsibility for the account, you should only open an account with someone you trust completely.

Joint credit cards are not very common, so your options for opening a joint account may be limited.

3. Become an Authorized User on a Credit Card With Age and Positive Payment History

Credit invisible consumers can add credit history to their credit reports by becoming authorized users on seasoned tradelines.

While the previous two credit establishment strategies involve opening a new primary account, which means you’d be starting out with no credit age, the authorized user method provides a shortcut to gaining years of credit history.

When you become an authorized user on a seasoned tradeline (an account with at least two years of age), often the full history of that account is reflected in your credit report as soon as the next reporting date for that account. In other words, you can add years of credit age and positive payment history to your credit file in just a few weeks and sometimes even faster.

The CFPB’s research showed that 19% of consumers (about one in five) had at least one authorized user account on their credit record, and over half of these consumers had transitioned out of credit invisibility as a result of one of their authorized user accounts. On average, consumers gained at least two years of credit history from authorized user accounts.

Not all banks report authorized user data, but when you buy tradelines from Tradeline Supply Company, LLC, you can be confident that we only work with banks that have been proven to reliably report authorized user information.

In addition, authorized user tradelines can increase the total credit limit of your profile.

For these reasons, the authorized user strategy is the fastest and easiest way for those who lack credit history to start building credit.

Once you’ve established some credit history through credit piggybacking, you can look into opening your own primary accounts.

Credit-Builder Loans

A credit-builder loan is a good option for those without credit history since they are easier to get approved for than traditional loans.

A credit-builder loan is a type of installment loan designed for those who are just starting out on the path to building credit. Lenders are able to offer these loans to consumers with thin credit files or no credit history because they are set up so that the borrower makes all the payments toward the loan before receiving the funds.

See our article on credit-builder loans for more information on how they work and whether a credit-builder loan could help you.

Secured Credit Cards

Those with limited credit history may also benefit from opening a secured credit card. Secured credit cards require you to make a security deposit, the amount of which then becomes your credit limit. Secured cards typically have low credit limits, but they can help you build credit by reporting your payment history to the credit bureaus.

Retail Store Credit Cards

A retail store credit card may also be a good option for those who do not have a credit history, as they tend to be easier to get approved for than bank credit cards. Just be careful not to carry a balance from month to month since retail cards also tend to have higher interest rates.

For example, the CFPB’s report on becoming credit visible found that low-income consumers were significantly less likely than higher-income consumers to use credit piggybacking methods to establish credit.

Consumers in low- and moderate-income neighborhoods were found to be 48% and 25% less likely, respectively, than consumers in middle-income neighborhoods to become credit visible through a joint account.

Similarly, consumers in lower-income neighborhoods who had recently transitioned out of credit invisibility were less likely to have authorized user accounts on their credit files compared to those in higher-income areas.

In addition, lower-income consumers were less likely to become credit visible via an authorized user tradeline. Lower-income consumers who did have their credit records created as a result of an authorized user tradeline gained less credit history than higher-income consumers.

Since credit piggybacking requires you to partner with someone who has decent credit and/or income, it would seem that perhaps low-income consumers simply do not have access to these resources and partnerships within their social networks.

In the words of the CFPB, “…a lack of co-borrowers may be an important contributor to credit invisibility in low- and moderate-income neighborhoods.”

Today, authorized user tradelines are affordable and accessible to more consumers than ever before.

As we learned earlier, credit invisibility is significantly more prevalent among Black and Hispanic consumers. Altogether, the data suggest that consumers who are Black, Hispanic, or low-income are at a severe disadvantage when it comes to establishing credit and building a credit history.

These are just a few of the many ways in which inequality is manifested throughout the credit system. Simply put, privileged consumers have the opportunity to build credit through credit piggybacking while many others are denied this opportunity.

Historically, the strategy of building credit by becoming an authorized user was primarily limited to the wealthy. Today, however, a marketplace exists where consumers of all backgrounds can take advantage of the benefits of authorized user tradelines.

In addition, there is a wealth of information online that consumers can use to educate themselves on the credit system and start off on the right foot when it comes to building credit.

As a leader in the tradeline industry, Tradeline Supply Company, LLC has opened the door to equal credit opportunity for thousands of consumers. By offering some of the lowest tradeline prices in the industry, we have made tradelines more affordable and accessible to the consumers who need them most.

When a lawyer sends a demand letter for a client, does that make her a debt collector? That’s the question in a lawsuit by a Dallas-area attorney who became embroiled in a billing dispute with a roofing company that worked … Continue reading →

An estimated 30,000 student loan borrowers thought their private loans were discharged when they declared bankruptcy years ago — but their student loan lender, Navient, disagreed. Navient continued collecting for those loans, and now the borrowers are suing in the … Continue reading →

A group of Democratic lawmakers — including Sen. Elizabeth Warren (D-Mass.), a presidential candidate — are seeking information from the IRS about the agency’s plans to implement a requirement that it exclude low-income taxpayers and certain recipients of Social Security … Continue reading →

Ford reported quarterly results on Tuesday. SHANNON STAPLETON/Reuters Ford Motor Co. shares nosedived on Tuesday after it handed investors a weaker-than-expected 2020 forecast, warning that quality problems, lower profits at its credit arm and continued investments in unprofitable self-driving cars … Continue reading →

Revolving accounts and installment accounts are both important account types when building credit, but they are not equally powerful when it comes to your credit score. Which type of account has a greater impact on your credit score? Keep reading to find out.

Revolving Debt vs. Installment Debt: Definitions Revolving Credit Account Definition

A revolving credit account is an account that allows you to “revolve” a balance, which means you do not have to pay the full outstanding balance on the account every month.

Revolving accounts typically have a credit limit up to which you can charge up to. You can choose how much to borrow from the account; you do not have to use the full credit limit. Once you make payments against the balance, that amount of credit is then available for you to use again.

Revolving accounts include lines of credit and credit cards.

Installment Credit Definition

Installment credit, in contrast, is credit where the full loan amount is disbursed at one time. You then make regular payments of a fixed amount toward the debt over a certain period of time.

Installment debt includes mortgages, auto loans, student loans, personal loans, credit-builder loans, and any other type of loan that has a regular payment schedule of fixed payments.

How Installment and Revolving Debts Affect Your Credit Score Revolving Accounts and Your Credit Score

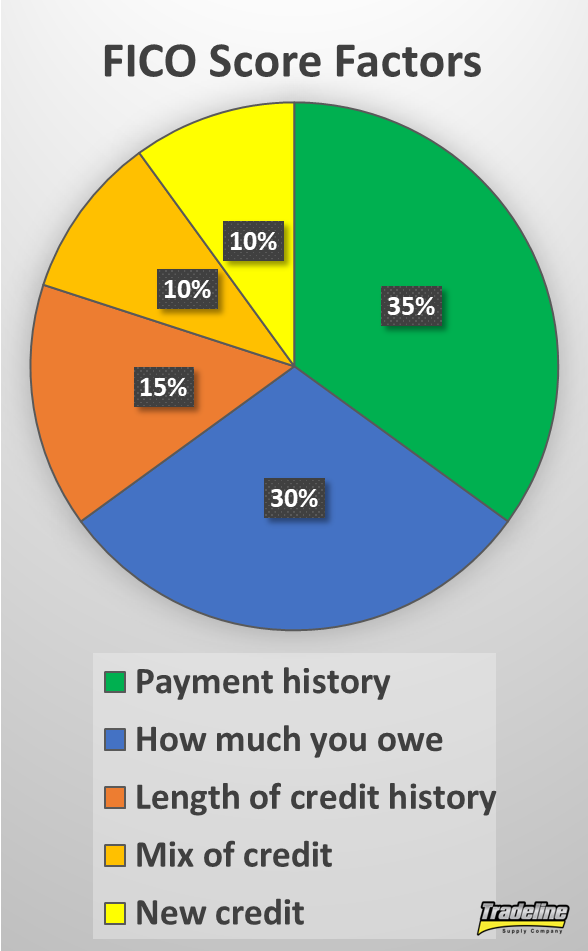

Five main factors are considered by FICO scores.

As you know from our article on credit scores, there are five main factors that influence your FICO score:

Revolving accounts can have a significant effect on each of these five factors.

As far as payment history, it’s important to pay your bills on time every single month just like any other account. However, with revolving accounts, you do not have to pay off the full balance every month. Instead, there is likely a minimum payment amount that you will be required to make. If you make a payment that is less than the minimum payment, your account will still be considered delinquent.

A lot of the power of revolving accounts comes from their influence on your utilization. This is because the credit utilization factor of your credit score places much more importance on the utilization of your revolving accounts.

Having high revolving utilization means that you are using a large portion of your available credit, which indicates to lenders that you might be at an increased risk of default. That’s why high credit utilization is bad news for your credit score.

If you run up a balance on a credit card and then only pay the minimum payment each month, you will be increasing your credit utilization. Since utilization makes up 30% of your FICO score, carrying a balance on your revolving accounts can seriously reduce your score.

Credit age is also important since it goes hand-in-hand with payment history. The longer you keep your revolving accounts open, the better. Even after they are closed, they can still continue to age and impact your average age of accounts.

Having a few different revolving accounts is also beneficial to your credit mix. Consumers with FICO scores of 785 and up have an average of seven credit cards in their credit files, including both open and closed accounts. In fact, if you don’t have enough revolving accounts, you can get dinged for a “lack of revolving accounts,” because without them there is not enough information to judge your creditworthiness, according to Discover.

Having too many inquiries for revolving accounts or too many new revolving accounts can hurt your credit score. Typically, each application for a revolving account is counted as a separate inquiry.

Installment Loans and Your Credit Score

When it comes to your credit score, installment loans primarily impact your payment history. Since installment loans are typically paid back over the course of a few years or more, this provides plenty of opportunities to establish a history of on-time payments.

Since installment loans typically don’t count toward your utilization ratio, you can have a high amount of mortgage debt and still have good credit.

Having at least one installment account is also beneficial to your credit mix, and installment debt can also impact your new credit and length of credit history categories.

What installment loans do not affect, however, is your credit utilization ratio, which primarily considers revolving accounts. That’s why you can owe $500,000 on a mortgage and still have a good credit score. This is also why paying down installment debt does not help your credit score nearly as much as paying down revolving debt.

This is the key to understanding why revolving accounts are so much more powerful than installment accounts when it comes to your credit score. Credit utilization makes up 30% of a credit score, and that 30% is primarily influenced by revolving accounts, not installment accounts.

In addition, with a FICO score, multiple inquiries for certain types of revolving accounts (mortgages, student loans, and auto loans) will count as just one inquiry as long as they occur within a certain time frame. As an example, applying for five credit cards will be shown as five inquiries on your credit report, whereas applying for five mortgage loans within a two-week period will only count as one inquiry.

Why Are Revolving and Installment Accounts Treated Differently By Credit Scores?

Now that you know why revolving accounts have a more powerful role in your credit score than installment accounts, you might be wondering why these two types of accounts are considered differently by credit scoring algorithms in the first place.

According to credit expert John Ulzheimer in The Simple Dollar, it’s because revolving debt is a better predictor of higher credit risk. Since credit scores are essentially an indicator of someone’s credit risk, more revolving debt means a lower credit score.

Since revolving accounts like credit cards are usually unsecured, they are a better indicator of how well you can manage credit.

Why is it that revolving debt better predicts credit risk than installment debt?

The first reason is that installment loans are often secured by an asset such as your house or car, whereas revolving accounts are often unsecured. As a result, you are going to be less likely to default on an installment loan, because you don’t want to lose the asset securing the loan (e.g. have your car repossessed or your home foreclosed on). Since revolving accounts such as credit cards are typically unsecured, you are more likely to default because there is nothing the lender can take from you if you stop paying.

In addition, while installment debts have a schedule of fixed payments that must be paid every month, revolving debts allow you to choose how much you pay back each month (beyond the required minimum payment). Since you can decide whether to pay off your balance in full or carry a balance, revolving accounts are a better reflection of whether you choose to manage credit responsibly.

How to Use Revolving Accounts to Help Your Credit

Since revolving accounts are the dominant force influencing one’s credit, it is wise to use them to your advantage rather than letting them cause you to have bad credit.

Here’s what you need to do to ensure your revolving accounts work for you instead of against you:

Make at least the minimum payment on time, every time. Don’t apply for too many revolving accounts and spread out your applications over time. Aim to eventually have a few different revolving accounts in your credit file. Keep the utilization ratios down by paying off the balance in full and/or making payments more than once per month. Use our revolving credit calculator to track your utilization ratios. Avoid closing revolving accounts so that they can continue to help your credit utilization.

Revolving Accounts vs. Installment Accounts: Summary

Revolving accounts are given more weight in credit scoring algorithms because they are a better indicator of your credit risk. Revolving accounts play the primary role in determining your credit utilization, while installment loans have a much smaller impact. High utilization on your revolving accounts, therefore, can damage your score. With a FICO score, inquiries for installment loans are grouped together within a certain time frame, while inquiries for revolving accounts are generally all counted as separate inquiries. Therefore, inquiries for revolving accounts can sometimes hurt the “new credit” portion of your credit score more than inquiries for installment accounts. Use revolving accounts to help your credit by keeping the utilization low and keeping the accounts in good standing.

What is credit piggybacking? If you’re not sure what this strange term could possibly mean, you’re definitely not alone.

Credit piggybacking, also referred to as “credit card piggybacking” or “piggybacking credit,” is a commonly used credit-building strategy. However, many people are still unaware of how to access this strategy and use it to their advantage.

In this article, we’ll define what piggybacking for credit means and how it can help your credit.

Credit Piggybacking Definition

The general definition of credit piggybacking is building credit by sharing a credit account with someone else. For example, spouses, business partners, and parents and children are all common examples of people who often share credit.

There are three main ways in which credit piggybacking can take place, which we discuss in more detail in “The Fastest Ways to Build Credit”:

Opening an account with a cosigner or guarantor is one way to piggyback on someone’s good credit.

Opening an account with a cosigner or guarantor, which is someone who promises to be responsible for the debt if the primary borrower cannot repay it. If the cosigner or guarantor has good credit, the borrower may be able to qualify for credit that they could not qualify for on their own or qualify for better terms. Opening a joint account with another person, which means both parties have full access to the account and are both held fully responsible for the account. By opening a joint account with a partner who has good credit, a person with less-than-ideal credit may be able to open an account that they wouldn’t have qualified for on their own or get more favorable terms. Becoming an authorized user for the purpose of credit card piggybacking, meaning you are not responsible for the debt, but the entire history of that account may be reflected in your credit file, regardless of when you were added to the account.

When people talk about piggybacking credit, they are usually referring to the method of piggybacking using authorized user tradelines.

How Does Authorized User Piggybacking Work?

Here’s how piggybacking works as an authorized user:

When you are added as an authorized user to someone’s credit card, often (depending on the bank), the full history of that account will then be shown in your credit report, regardless of when you were added to the card. Therefore, piggybacking can almost instantly add years of perfect payment history to the authorized user’s credit file. Authorized user tradelines can affect many important credit variables, such as your average age of accounts, age of oldest account, overall utilization ratio, number of accounts, mix of accounts, and more. Historically, only the wealthy and privileged were able to use piggybacking as a credit-building strategy. Now, there is a marketplace where tradelines can be bought and sold, which is helping to democratize the credit system and provide equal credit opportunity.

The issue of piggybacking went all the way to Congress, which upheld consumers’ rights to use authorized user tradelines.

Is Piggybacking Credit Legal?

While Tradeline Supply Company, LLC does not provide legal advice, we can provide evidence that supports the idea that piggybacking credit is legal.

Firstly, piggybacking for credit is an extremely common practice that has been in use since the advent of credit cards. Studies estimate that 20-30% of Americans who have credit records have authorized user accounts in their credit file.

In addition, about 25% of people who have credit reports initially established their credit files by piggybacking in one way or another.

Many banks actually encourage consumers to add authorized users for the express purpose of boosting their credit scores.

You may have heard about FICO trying to take away authorized user privileges in 2008. But what you probably didn’t hear about was FICO backing down after a congressional hearing that involved the Federal Trade Commission and Federal Reserve Board.

During the hearing, FICO admitted that they could not legally discriminate between spousal AUs and other users, because this would unlawfully violate the Equal Credit Opportunity Act.

Since the U.S. Congress has upheld consumers’ rights to use authorized user tradelines, it seems reasonable to conclude that authorized user tradelines are legal.

However, it is important to get your tradelines from a reputable source. Some tradeline companies use illegal credit profile numbers (also known as CPNs) to mislead creditors as well as consumers. That’s why consumers should only work with tradeline companies that don’t use or sell CPNs—learn more about CPNs and why Tradeline Supply Company, LLC does not accept them.

Does Piggybacking Credit Still Work?

As we discussed in “Do Tradelines Still Work in 2020?”, credit piggybacking still works, and we think it will be around for a long time.

Piggybacking credit is a well-established credit-building strategy that has been defended in Congress and promoted by banks. It is a significant part of our credit system.

Thanks to the Equal Opportunity Credit Act, authorized user tradelines are still a very important factor in credit scoring models.

Not only that, but even if FICO were to devise an algorithm intended to exclude piggybackers, it would be quite some time before lenders could implement it on a large scale. The slow-moving financial industry is still using FICO scores that were developed decades ago.

Piggybacking companies bring together buyers and sellers of authorized user tradelines.

What Do Piggybacking Companies Do?

Friends and family will often allow each other to piggyback, but for many people, it’s difficult to find someone with good credit to piggyback on. A third party can play a role in helping to connect people who are looking to purchase seasoned tradelines with people who have high-quality tradelines to offer.

Piggybacking companies, more commonly referred to as tradeline companies, simply facilitate the buying and selling of authorized user tradelines.

The tradeline company acts as an intermediary by marketing the tradelines to consumers, protecting the identities of the clients, and preventing fraud.

At Tradeline Supply Company, LLC, we provide an innovative platform through which users can buy and sell tradelines entirely online. We also provide educational resources so consumers can familiarize themselves with the credit system and how piggybacking works.

How Long Does Piggybacking Credit Take Before I See the Tradelines on My Credit Report?

The account you are piggybacking on can show up on your credit report in as little as 11 days, depending on several factors relating to the particular tradeline.

Each piggybacking tradeline has its own reporting cycle, and Tradeline Supply Company, LLC provides a “purchase by date” before which you must purchase your tradeline in order for us to guarantee that it will post in the coming reporting cycle. If you miss the purchase by date, it will simply show up in the following cycle.

If you have purchased a seasoned tradeline that you believe has not posted, first, check to make sure that the entire reporting period has passed, then check your credit reporting service again to verify that it still has not posted. If you take these steps and determine your tradeline has not posted, please reach out to us for support and we will rectify the situation.

Can Piggybacking Hurt Credit?

If credit piggybacking is done incorrectly, it can actually backfire and hurt your credit.

Because the full history of the credit account is reflected in the credit file of the piggybacker, that means any derogatory factors will show up, too.

For example, if the account has any late or missed payments, that could hurt the authorized user rather than help. Similarly, a high utilization ratio on the account could also damage the authorized user’s credit.

That’s why we recommend going with a reputable piggybacking company who guarantees a perfect payment history and a low utilization ratio (15% or lower) on all tradelines. This will virtually eliminate the risk of your credit being hurt by these factors.

The only other way piggybacking could hurt your credit is if you choose the wrong piggybacking credit card. It’s essential to choose the right tradelines for your credit file. To do this, you’ll need to figure out your average age of accounts and how adding a tradeline could affect this statistic.

For example, if your average age of accounts is five years and you decide to piggyback on a tradeline that is two years old, this would bring down your average age of accounts, which is the opposite of what you want to achieve with tradelines.

Fair Isaac Corp. (FICO) FICO, -1.36% is changing how it calculates credit scores, and the new criteria reveal some of the trouble spots in Americans’ financial health. Two of the most substantial changes in the new scoring models, FICO Score … Continue reading →

Here’s a number that may shock you: about one in five American adults do not have a credit score.

Here’s a number that may shock you: about one in five American adults do not have a credit score.