Nearly one in four customers of the major credit-card companies were unable to make monthly payments this spring, according to a survey released on Thursday (Sept. 17) by J.D. Power. J.D. Power’s May and June survey of more than 6,700 … Continue reading →

The operators of a student loan debt relief scheme will pay at least $835,000 to settle Federal Trade Commission allegations that they charged illegal upfront fees and made false promises to consumers struggling with student loan debt. The settlement resolves … Continue reading →

Lloyds Bank has teamed with ConnectedFi in order to provide brokers with quicker asset finance credit decisions by using automation, according to Financial Reporter. Lloyds will now integrate its asset finance application programming interface (API) into the FinTech software company’s … Continue reading →

Consolidation and refinancing are two commonly-discussed debt repayment solutions. Though these terms are sometimes used interchangeably, there are some important differences between the two and considerations that go into choosing which one is best for you. Adding to the complication is that “consolidation” is often associated with credit card debt while “refinancing” is often used to describe a particular mortgage repayment strategy. In reality, most types of debt can be consolidated or refinanced. Each of these options may be a viable strategy for your credit card debt. Here is a closer look at the two approaches, with an emphasis on how you might use them for credit card debt.

Debt Consolidation

We have discussed debt consolidation quite a bit lately, including smart strategies you can use to consolidate debt and its impact on your credit score. Here is a quick refresher. Debt consolidation is the process of paying off two or more existing debts with a new debt, effectively combining the old debts into one new financial commitment.

As a simple example, imagine you have three credit cards: A, B, and C. Let’s say you open a new balance transfer credit card (we’ll call that card D). You can transfer the balances from card A, B, and C to card D—meaning that A, B, and C now have zero balances. Now, you will make payments toward card D, and that will be your only credit card obligation (assuming you close card A, B, and C or don’t use them). That’s consolidation.

Its primary benefit is that it simplifies repayment and makes your debt easier to manage. In our example, sending one payment each month would be easier than three. A secondary benefit is that consolidation can be used to get better terms on your debt, which makes repayment faster. For example, assume that card D had a promotional, zero-percent interest rate while cards A, B, and C had been racking up interest with rates over 15 percent. Just keep in mind that consolidation does not always get you better terms. It depends on your credit score and the purpose of your consolidation.

Refinancing

Refinancing is simply changing the finance terms on a debt obligation. Typically, this occurs by taking out a new loan or other financial product with the different terms. The most basic example is a mortgage refinance. There are different types of mortgage refinances, but we will focus on the “rate-and-term” refinance. This has been incredibly popular in recent years given the historically low interest rates that have been available. It works like this: let’s say a homeowner has a mortgage at 4 percent interest but wants to refinance to a lower rate, say 3.5 percent. The homeowner could basically take out a new mortgage to pay off the original mortgage. The new loan would have new terms, meaning a new interest rate (here it would be 3.5 percent) and potentially a new repayment period.

What about for credit cards? You do not hear about “refinancing credit cards” as often, but it is possible and quite common. It can be difficult to decipher the difference between refinancing credit card debt and consolidating it. The confusion comes from the fact that different industries, companies, and individuals use this financial vocabulary in different ways. For instance, some companies may refer to balance transfers as credit card refinancing, and will only use “debt consolidation” to refer to a strategy involving a consolidation loan.

But, that does not quite hold true. Balance transfers are often used to consolidate multiple debts. Instead, think of it this way: All consolidation involves refinancing, but not all refinancing involves consolidation. The primary distinction is based on the number of debts you have. You cannot consolidate a single debt, because you do not have other debts to combine it with. However, you can refinance it. On the other hand, if you move multiple debts into a new debt, you will have new repayment terms (meaning you refinanced) but you have also consolidated into a single debt obligation.

There is, arguably, one other form of refinancing. However, it does not adhere to the strict, traditional definition. As mentioned above, refinancing typically involves a new financial obligation that replaces an old obligation. However, it could also involve keeping the financial obligation you already have, but negotiating the terms. In the credit card context, you may be able to negotiate a lower interest rate on your credit card, for example. That is effectively a refinancing of the credit card debt without taking on a new debt.

One argument against considering this to be a “refinance” is that often the negotiated terms are temporary. Your creditor might lower the interest rate for a short period of time because of a hardship you are experiencing, but that is much different than agreeing to a fundamental change to the interest rate for the rest of your time as a card holder.

What About a Debt Management Plan?

You might think of a debt management plan (DMP) as combining the best features of consolidation and refinancing. A DMP does not technically consolidate your debts, but it allows you to pay one monthly payment for all your credit cards on the plan. You pay the credit counseling agency one payment, and they distribute that payment to your creditors. It also has the perk of a being an effective “refinance” because your debts are often charged lower interest rates while on the plan.

The Takeaway

The various terms used to describe debt repayment options can create some confusion. At the end of the day, the exact language does not matter as much as the outcome. Keep in mind that managing your debt is important and consolidating your payments may make the management easier. Also, the terms of your debt are important because they will affect how affordable the debt is and how quickly you can pay it off. There are a variety of repayment strategies that incorporate these variables. If you would like help thinking through the strategy that may be best for you, contact a credit counselor for free assistance.

Your credit score is a seemingly simple three-digit number, but it can have a major impact on your finances. Without a high score, you may not be able to pursue some of your major financial goals. Or even if you can, those goals can actually turn into major challenges if you’re stuck with high interest rates because you had a low score. If you are preparing to improve your credit, you need to know the general ranges for scores so that you can set a specific goal for yourself. There are various tiers of credit scores, and being in a higher tier will generally bring the reward of better terms.

First, What’s the Average?

We’re going to talk about credit score categories in a moment, such as “poor,” “fair,” and “good.” But first let’s take a look at the average credit score. One initial point of clarification—while there are two major credit scoring models—FICO and VantageScore—we will focus primarily on the FICO score in this article, though we will make brief mention of the VantageScore as well. There are actually multiple FICO scoring models, and lenders use a variety of them, but the information here specifically relates to FICO® Score 8.

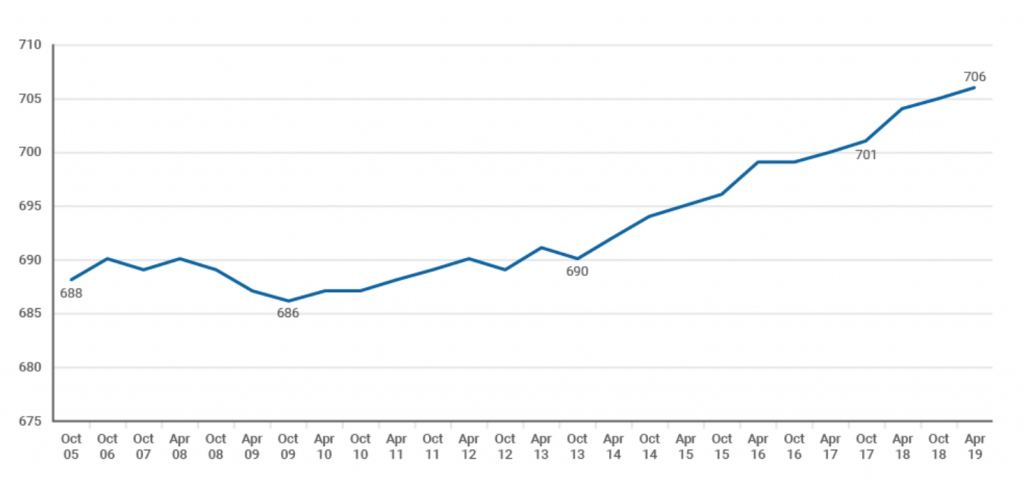

FICO most recently reported that the average credit score is 706. Credit scores nationwide can fluctuate significantly depending on the state of the economy. Back in 2009, the average was 686. COVID-19 and other economic factors may have a negative impact on the national average, but only time will tell. The average can be a useful baseline for comparing your own score. But, don’t let the average discourage you if your score is lower, because there are many ways to increase your score.

Source: FICO.com

The Breakdown

Using the FICO 8 scoring model, the credit bureaus agree (see Experian’s post here and Equifax’s here) to the following breakdown for score ranges. Again, remember that your lender may use a different model which could result in a slightly different breakdown. But, this should give you a good general idea of what to aim for.

Poor

A poor credit score is a score between 300 and 579.

Fair

A fair credit score is a score between 580 and 669.

Good

A good credit score is a score between 670 and 739.

Very Good

A very good credit score is a score between 740 and 799.

Excellent

An excellent credit score is a score between 800 and 850.

If you are curious about the breakdown for VantageScore 3.0, it looks like this:

Interestingly, the VantageScore ranges are narrower on the low end of the spectrum (including both a “very poor” and “poor” range, and broader on the high end (including only a “good” and “excellent,” without a “very good” range).

Why the Ranges Matter

Now that you know the ranges, here are three important reasons that they matter.

Access to Credit and Other Services

If your score is too low you may not have access to credit or, at the very least, you will likely have obstacles to credit. A score in the “very poor” range may mean that any applications for credit are denied. Your best bet may be a secured credit card, which requires you to make a deposit. While this is not ideal, a secured card can be an important tool in rebuilding your credit.

Also, remember that getting credit is not the only concern. Access to other products and services often depends, in part, on your credit history. Being in the “very poor” range can limit your ability to rent an apartment, enter certain contracts, or even get a job.

Favorable Credit Terms

Even if you can get credit, you will want the credit terms to be as favorable as possible. Bad credit terms, like high interest rates, will make your debt more expensive. They will also limit your purchasing power, which can prevent you from buying the home or car you want. Every time your score improves from one category to the next (say from “fair” to “good”), that should be paired with lenders offering you more favorable terms.

Here is a look at estimated mortgage rates by credit score and a look at auto loan rates by credit score. Note: these tools use different ranges and terminology for scores (for instance, the auto loan chart has ranges from “deep subprime” to “super prime”), but the general point still applies.

Goal Setting

Knowing the general credit score ranges can help you plan your goals for the future. Make a plan to check your credit score frequently, but especially as you make major changes (paying off a debt, opening a new card or loan, or changing your credit limit). You will also need to check your credit report often, as that report is the basis for your score. Keeping a close eye on these will help ensure that you move your credit in the right direction.

Want a free credit report review? An NFCC-certified counselor can review your credit report with you, and help you make a game plan for improving your financial standing. Learn more about the free credit report review, or get started here.

Millions of Americans are grappling with student debt on top of the challenges posed by the coronavirus pandemic and the economic recession. Unlike other categories of personal debt, most student loans are nondischargeable absent a showing that the debtor is … Continue reading →

PARSIPPANY, N.J., Sept. 8, 2020 /PRNewswire/ — Snellings Law LLC, a leading technology-driven debt collections and commercial litigation firm focused on helping businesses recover money owed to them throughout New Jersey, is proud to announce the launch of its newly redesigned … Continue reading →

Will it keep them from retiring altogether? Credit card debt is never a good idea. When you’re young, though, it’s a lot easier to rebound from financial mistakes. As we get older, it can be harder to recover from financial … Continue reading →

PIERRE, S.D. (KELO) — A company that since 2015 has worked to corral money that people owe to South Dakota state government now plans to step aside. State Administration Commissioner Scott Bollinger gave the news Wednesday to the Legislature’s Government … Continue reading →

If you’re out of work because your position was cut during the pandemic, you are certainly not alone. Many service-based industries have made substantial job cuts since March, and the employment landscape is constantly shifting beneath our feet. Hopefully, you are already taking the basic steps of staying in touch with your state unemployment office to make sure you receive your benefits. That office should also be able to point you to many resources that could help in your job search. However, you might also consider that some industries and sectors in the economy are hiring right now and may be more stable in the future. Here are some jobs you may consider moving forward.

Sectors that Jumped in August

The most recent report from the Bureau of Labor Statistics showed that a few industries made impressive hiring gains in August. Government hiring was up significantly, mainly due to positions related to the census. Retail added almost 250,000 jobs, professional and business services accounted for 197,000 new positions, 174,000 people started jobs in leisure and hospitality, 90,100 people were hired in health care and social assistance, and the transportation and warehousing sector added 78,100 jobs.

Some of these sectors, most notably leisure and hospitality, were hit hard by the pandemic and many of these “new” jobs might just be filling roles that went away when the pandemic began. Still, these numbers provide some hope for workers seeking employment in restaurants, bars, and other travel or hospitality settings.

Big Employers

The current environment, with future economic uncertainty still looming, may make the perfect time for joining a large established company. Large employers can often offer stability when others cannot. This is particularly true when the company’s business model is well-suited for the realities of the life during the pandemic. Enter Amazon.

Amazon’s hiring plans have made major headlines this year. As MarketWatch reports, just this month Amazon announced 33,000 new jobs in its corporate and technology divisions, and today it announced 100,000 new positions. This is actually the fourth major hiring announcement Amazon has made this year.

Amazon is not the only company on a hiring spree this year. Other companies with business models related to online shopping and shipping/transportation having been doing quite well and hiring new workers.

And that industry is not the only game in town, either. Companies in other industries are hiring, too. the Muse has published a list of large companies hiring during COVID-19, covering a wide array of industries and job types.

Small Businesses

Working for a large company has its perks, but you may also want to consider smaller businesses. Some small businesses are beginning to hire more regularly, after weathering the initial storm of the pandemic. Before COVID-19, the low unemployment rate had made it hard for some small businesses to attract and retain good employees. Now that more people are looking for jobs, good opportunities at small businesses may be more competitive.

If a small business made it through the pandemic and is hiring full-time positions now, that may be a positive indicator of the company’s stability moving forward. Definitely don’t count out successful, smaller employers.

Pandemic-Proof Occupations

One way to think about a job search is by asking who is hiring now. Another way is to think about which jobs are pandemic-proof. The disruption of the pandemic has divided jobs into those that are “essential” and those that are not. With a potential second wave on the horizon, or even without a second wave, many job-seekers may prefer the stability that comes with an essential role.

The Economic Policy Institute has labelled the following sectors “essential.” That is not to say that these sectors did not experience declines this year. Instead, it is an indicator that they were most resilient. It could be a smart move to transition to one of these career fields, though most will require specific skill-sets and training:

Food and agriculture

Emergency services

Transportation, warehouse, and delivery

Industrial, commercial, residential facilities and services

Health care

Government and community-based services

Communications and IT

Financial sector

Energy sector

Water and wastewater management

Chemical sector

Critical manufacturing

Moving Forward

Being out of a job is difficult, but there are some promising signs that hiring will continue improving in certain sectors. Consider learning any new skills required, dusting off your resume, and taking advantage of the opportunities that are available in the job market now. Even if landing a dream job is not an option right now, you will likely be much better off by getting full-time employment and then continuing to look for a better fit in the future.

If your employment situation is having a negative impact on your personal finances and credit, talk to a credit counselor for free help.