Do you have a low credit score? You may be in for a little luck if you want to buy a home.

It’s easier to buy a house now than it was a decade ago. More homebuyers are qualifying for a mortgage with a low credit score than they did just after the Great Recession, partly because of more lax Federal Housing Administration loans. Higher debt is also being allowed more often by home lenders.

A study by the Fair Isaac Corporation, or FICO, which is the most widely used type of credit score among lenders, found that credit scores for new mortgage originations have been dropping since tighter credit policies were enacted after the housing crisis.

That sounds like an oxymoron — lower credit scores allowed by mortgage lenders who tightened underwriting standards — but the looser requirements are mainly allowed by FHA mortgage loans that are among the easiest to get for people with low credit.

New mortgage loans with credit scores less than 700 increased from 21.9 percent of all mortgages in 2009 to 29.7 percent in 2017. These include subprime loans for borrowers with scores in the 400s. New mortgages with FICO scores less than 750 increased from 41 percent to 53 percent during the same time.

FICO scores range from 300 — which shows severe credit history problems and a high risk of default — to a high of 850 — where missed payments and default risks are extremely low. The higher a credit score is, the better chance the loan applicant has of being approved at a low interest rate.

Loan originations for FICO scores of less than 650, which are considered mediocre or bad scores, increased from 9.1 percent in 2009 to 10.9 percent in 2017.

More debt, too

Bigger debt-to-income ratios, or DTI, have also been allowed in FHA loans, according to FHA data. DTI measures a home buyer’s ability to repay their loan. Household income is weighed against ongoing monthly debt such as credit cards, auto loans, personal loans and other obligations, plus mortgage payments. The higher the monthly debts, the more likely a borrower is to go delinquent on their new mortgage.

Spending half of your income on debt was often seen as a bad sign to lenders. FHA loans, however, allow it, with one of every four FHA loans between January and March 2018 having a DTI ratio of more than 50 percent. In 2013, it was about half that, with 12.7 percent of approved new FHA applications carrying such a high debt load. Another 30 percent had DTI ratios between 43 and 50 percent.

Why the shift?

The Urban Institute’s Housing Finance Policy Center has found that 5.2 million mortgages were “missing” between 2009 and 2014, meaning they would have been made if lenders had relaxed their strict underwriting standards after the recession.

FICO gave a few reasons for the drop in credit scores among new mortgages, starting with the fact that there are fewer refinances occurring now.

“Many high scoring consumers took advantage of the historically low mortgage rates observed in 2012-13 to refinance their mortgages,” FICO officials wrote. “Once the refinance boom ended in 2014, the volume shifted back to purchase mortgages, which tend to be a lower scoring population than the mortgage-experienced segment.”

Conventional mortgages still require a good credit score, with 41 percent of such home loans closing in August 2018 for borrowers with a credit score of 750-799, according to data from Ellie Mae, which processes 35 percent of U.S. mortgage applications.

FHA loans, however, are another story. Home loans insured by the FHA saw credit scores drop, from an average of 701 from January through March 2011 to 672 for the same period this year, according to FHA data.

FHA loans are typically the easiest types of mortgages to qualify for because they require a low down payment and credit scores as low as 500 are allowed.

Credit behaviors of mortgage borrowers

In its mortgage originations report, FICO looked at what mortgage borrowers did to change their credit score, whether for good or bad.

Of about 2.8 million people who opened mortgages between May and July 2017, 12 percent had a significant increase of 40 points or more to their credit score. Another 11 percent saw their score drop the same amount and the remaining 77 percent had a relatively stable score change of less than 40 points.

Its analysis found that people who raised their credit score mostly did it by reducing credit card balances by almost half. Those who saw their score drop added to their credit card balances by 97percent, or almost doubling their credit card debt.

Consumers with a decrease in their credit score were much more likely to have had a missed payment in the past year. Payment history accounts for 35 percent of total score calculation.

Credit score decreases also resulted from applying for new credit, with credit inquiries increasing 22 percent for those with a FICO score decrease. People with a credit score increase had their credit inquiries drop by 21 percent.

Opening several accounts in a short period of time is a greater risk of future missed payments, especially for people who don’t have a long credit history, according to FICO. New credit makes up about 10 percent of a FICO score.

Debt collecting is a profession that gets little love, but given the social good done by debt collectors who operate ethically and follow the rules, maybe it’s time that we show them some affection. If not that, we should at … Continue reading →

The Idaho Department of Finance is focusing on reducing regulatory burdens and providing a comprehensive review of its professional licensing system, including for financial services companies, in the coming months. Idaho’s Red Tape Reduction Act, an executive order signed by … Continue reading →

CONSUMERS tend to prioritise paying off their credit cards ahead of other unsecured products, according to a TransUnion study. Pixabay Consumer credit has continued to rise over the past two quarters of this year, which means that consumers are relying … Continue reading →

A recent report by NerdWallet found that 26% of Americans have made a late credit card payment (30 days late or more) in 2019. By NerdWallet’s calculations, that amounts to more than $3 billion in late fees alone. The report … Continue reading →

View photos Twitter More Facebook More Apple’s credit card is launching soon, and it looks like the highly anticipated card will come with a few unusual rules. Goldman Sachs, which partnered with Apple on the card, … Continue reading →

Let’s take a breather from credit cards for a moment as we look at new numbers from the Federal Reserve Bank regarding consumer debt. Today, the WSJ editorial board weighed in on student loans, wondering about “The Great Student-Loan Scam” … Continue reading →

If you monitor your credit using a free website, chances are, you’ve seen your VantageScore. However, you may not realize that this credit score is not your FICO score.

So what is a VantageScore credit score and how is it different from a FICO credit score? Is one better than the other? We’ll compare and contrast the two types of credit scores and discuss the merits of each in this article.

What Is a Vantage Credit Score?

The VantageScore credit score, sometimes referred to as a “Vantage credit score,” is a credit scoring model created in 2006 by the three major credit bureaus (Experian, TransUnion , and Equifax) to compete with FICO’s credit scoring models.

VantageScore is a tri-bureau credit score, meaning the exact same model is used at each credit bureau.

The most commonly used version of the VantageScore used by lenders today is the third iteration of the credit scoring model, VantageScore 3.0.

VantageScore Solutions, LLC has released VantageScore 4.0, which is supposed to be more accurate than previous versions, but since it takes lenders a long time to adopt new credit scoring models, most are still using VantageScore 3.0.

Who Uses VantageScore?

According to Experian, VantageScore is used by lenders for all types of loans except mortgages, where FICO is still the dominant player. The largest group of financial institutions that uses VantageScore is credit card issuers.

Non-financial institutions have also increasingly been adopting VantageScore, such as landlords and utility providers.

VantageScore is also widely used by consumer websites that provide educational credit scores and market credit products.

What Is My Vantage Score?

It’s easy to find out what your VantageScore is for free. Credit Karma provides free VantageScore 3.0 credit scores from TransUnion and Equifax, so all you have to do is create an account on creditkarma.com and log in to your Credit Karma account to see your free Vantage credit score.

Credit Sesame and NerdWallet are other sites that provide consumers with free VantageScore 3.0 credit scores from TransUnion.

You can view your free VantageScore with TransUnion and Equifax on Credit Karma.

VantageScore vs. FICO Score

The primary difference between VantageScore and FICO scores is what they are used for.

FICO scores have been in use for a longer period of time and, consequently, are most widely used by lenders to make lending decisions. According to U.S. News, FICO scores are used by 90 percent of “top lenders.”

While VantageScore credit scores are also used by some lenders, they are more well-known for their use as an educational tool.

Both FICO and VantageScore consider the same general categories of information from your credit report (although they use slightly different terms to describe them), which include:

Payment history

Utilization

Length of credit history/age

Mix of accounts/types of credit

New credit activity/recent credit

Since the scores share the same general categories, it is safe to assume that they will both be bolstered by the same common sense behaviors that lead to good credit, such as not using too much of your available credit and not missing payments.

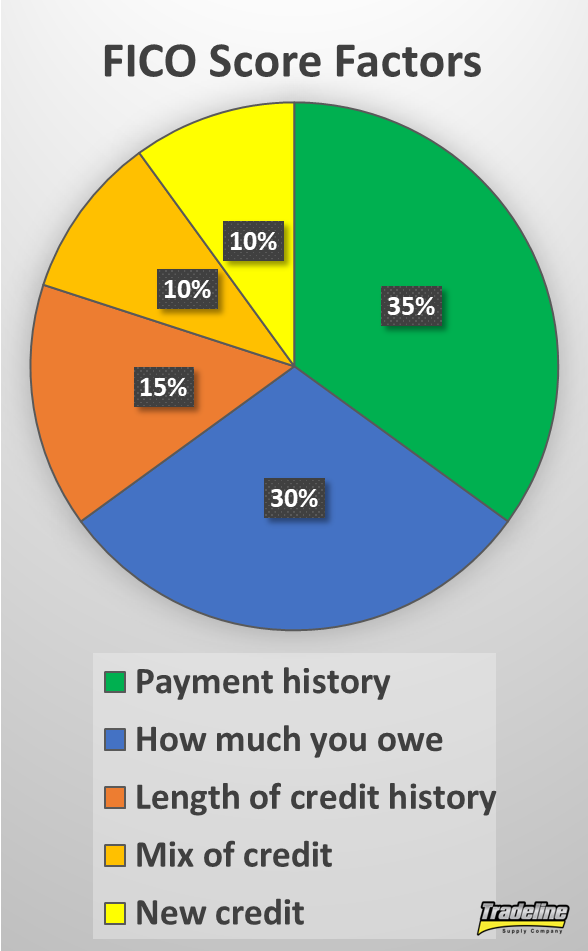

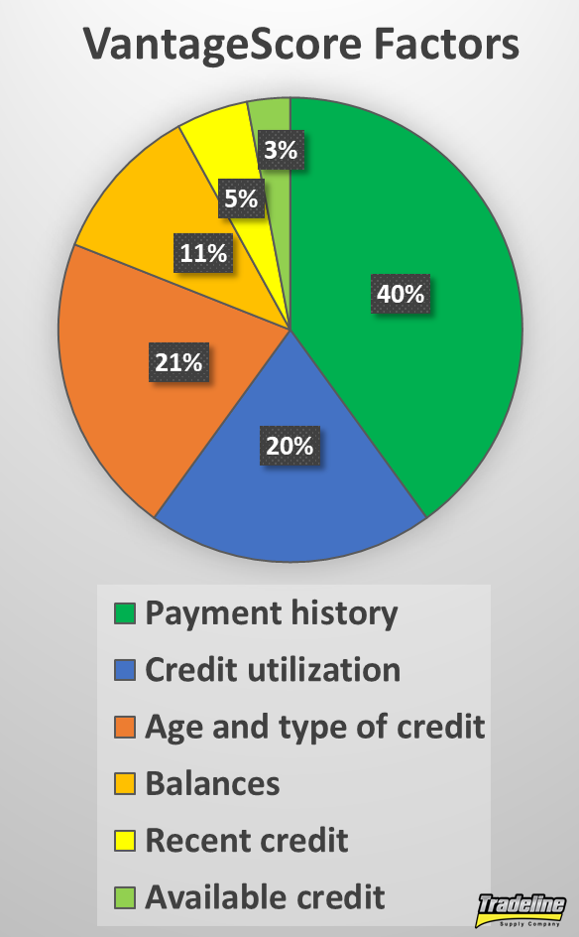

However, FICO and VantageScore assign slightly different weights to each category, as shown in the following table (percentage values are approximate).

FICO Score Factors

VantageScore Factors

Payment history, 35%

Payment history, 40%

Utilization, 30%

Credit utilization, 20%

Length of credit history, 15%

Age and type of credit, 21%

Mix of accounts, 10%

Balances, 11%

New credit activity, 10%

Recent credit, 5%

Available credit, 3%

FICO Score Factors

VantageScore Factors

In addition, within these broader categories listed above, the scoring models have different ways of assigning value to certain variables. Here are a few examples.

Inquiries

Hard inquiries can generally hurt your score by a few points because seeking new credit is considered risky behavior. When people are applying for some types of loans, such as mortgages, auto loans, and student loans, they tend to apply for multiple loans so they can shop for the best rates. Credit scoring models now have different ways of accounting for this behavior so as not to punish consumers for shopping around.

Newer FICO scores group inquiries of the same type together within a 45-day window. That means consumers could apply for 5 auto loans within 45 days and it would only count as one inquiry. Older FICO scores do this within a 14-day window.

FICO scores only apply this rule to student loans, mortgages, and auto loans—not credit cards. According to creditcards.com, the FICO scoring model also includes a 30-day “buffer” against hard inquiries, which means it ignores any inquiries that occurred within the last 30 days.

In contrast, VantageScore groups all inquiries within a 14-day window, regardless of the type of account. You could apply for some credit cards, a student loan, a mortgage, and an auto loan within 14 days, and it would only count as one inquiry.

Collections

Unpaid collections are always going to make a significant dent in one’s credit score, but paid collections and collections with small balances are treated differently between FICO and VantageScore.

With FICO 8, the credit score most widely used by lenders today, all unpaid and paid collections are damaging, regardless of the type of account. FICO 9, the newest FICO score, leaves out paid collection accounts and reduces the impact of unpaid medical collections specifically. Both FICO 8 and FICO 9 disregard collections when the original balance was less than $100.

VantageScore 3.0 and 4.0 are similar to FICO 9 in that they don’t count paid collection accounts and assign less importance to medical collections, but they do not make exceptions for collections with low balances.

Utilization

While utilization is treated fairly similarly with both scoring models, the specific thresholds that affect credit scores vary. VantageScore recommends keeping your credit utilization below 30%, while many experts believe that FICO scores suffer at lower utilization ratios.

Interestingly, the newer VantageScore 4.0 looks at the trends in your utilization over time, such as whether your balances have increased or decreased. FICO scores and previous VantageScore versions only look at the data that is in your credit report at the moment when your score is calculated and do not look “back in time.”

Other Differences Between VantageScore vs. FICO

Tri-bureau vs. single-bureau

With FICO, each credit bureau uses a different version of the score that is specific to that bureau. As a result, consumers often have different credit scores for each credit bureau.

VantageScore, however, was designed to work the same for all three credit bureaus in an effort to reduce the disparity in scores between credit bureaus.

Who can be scored

The two types of scoring models have different requirements for who can be scored.

FICO requires at least six months of credit history and at least one account reported within the last six months. That means if you’re just starting out in building credit, you’ll need to wait six months after opening your first account to establish a FICO score.

On the other hand, VantageScore is able to score consumers with only one month of credit history on at least one account reported within the last 24 months.

Credit score scale

Previous versions of VantageScore had a scale that was different from the scale that the FICO score uses. For example, VantageScore 2.0 ranged from 501-990. The VantageScore 3.0 range was changed to match the FICO credit score scale of 300-850.

However, they have slightly different rating scales within those credit score ranges, as you can see in the table below.

FICO Score

VantageScore 3.0

Credit Score

Rating

Credit Score

Rating

300-579

Very Poor

300-499

Very Poor

580-669

Fair

500-600

Poor

670-739

Good

601-660

Fair

740-799

Very Good

661-780

Good

800-850

Exceptional

781-850

Excellent

What Is a Good Vantage Score?

From the table above, we can see that a good VantageScore is between 661 and 780. Compare this to FICO’s good credit score rating, which is a narrower range of scores from 670 to 739.

720 would be considered a good credit score with both FICO and VantageScore. Photo by CafeCredit.com, CC 2.0.

Similarly, an excellent VantageScore credit score ranges from 781 to 850, while FICO’s “exceptional” credit rating ranges from 800 to 850.

Is There a VantageScore to FICO Conversion Formula?

Unfortunately, there is no Vantage to FICO conversion formula that can be used to calculate your FICO score from your VantageScore and vice versa.

As we learned in our comparison of VantageScore vs. FICO scores, the two scoring models assign different values to each credit score category and even have slightly different categories.

They also use different proprietary algorithms, the details of which are carefully guarded trade secrets.

To make things even more complicated, both FICO and VantageScore utilize “scorecards” or “buckets” to categorize consumers. Each scorecard has a different way of scoring consumers. In other words, the specifics of the credit score algorithms vary for different consumers even within the same version of a credit score.

Since each credit score is so complex and we as consumers do not have access to the secret algorithms, there is no reliable or accurate way of converting between the two.

Why Is My Vantage Score Lower Than FICO?

Since VantageScore and FICO scores differ in the weights they assign to each category and variable within the scoring model, it is likely that one will usually be lower than the other.

Since payment history is weighted more heavily with VantageScore than FICO (40% vs. 35%, respectively), a missed payment could bring your VantageScore down a bit more than your FICO score.

Another reason for having a lower VantageScore could be having unpaid low-balance collections on your credit report, which hurt your VantageScore but not your FICO 8 or 9 score.

However, what people tend to see more commonly is that their VantageScore is slightly higher than their FICO score because VantageScore seems to be more forgiving when it comes to credit utilization.

Which Credit Score Is Better?

Unfortunately, there is no straightforward answer to the question of which credit score is superior to the other. Each credit score has value for its respective purposes.

Although some people dismiss VantageScore as being a “fake” or inaccurate version of a FICO score, that’s not necessarily a fair comparison. Although both scores emphasize the same general credit principles, they have significant differences in the ways they treat certain factors. VantageScore is intended to be a competitor to FICO, not an exact replicate, so we shouldn’t expect them to be the same.

Since the same general principles shape how both scores work, however, oftentimes what helps one will help the other. This is why VantageScore has been so successful as an educational score offered by many free sites despite its differences from FICO.

While consumers may often have to pay to get their FICO score, they can monitor their credit and get a good idea of what is affecting their score for free using consumer websites that employ VantageScore. They can then take action that will help improve both their VantageScore and their FICO score.

Therefore, for general credit-building purposes, VantageScore is just as useful as FICO.

That said, it is important to keep in mind that most lenders still use FICO scores and many use earlier versions of FICO, which may be less comparable to VantageScore credit scores. If you are applying for a mortgage soon, for example, you’ll probably want to pull your FICO score in addition to your VantageScore, since mortgage lenders overwhelmingly use FICO in their lending decisions.

VantageScore and FICO scores are both important to get to know as a consumer, especially as VantageScore gradually becomes more popular with lenders.

What do you think about the VantageScore credit score? Have you compared yours to your FICO score? We’d love to hear your thoughts in the comments.

Danielle Douglas-Gabriel, The Washington Post Published 12:36 pm PDT, Thursday, August 1, 2019 A federal judge on Wednesday cleared the way for the Education Department to stop using private debt collectors and revamp the way it handles overdue student loans. Instead … Continue reading →