SAN FRANCISCO (CN) – A debt collector did not break the law by using government seals and letterheads to get people who bounced checks to pay restitution and take classes, a federal judge ruled Wednesday, but the company may have … Continue reading →

ShareTweetEmail Travis County Justice of the Peace for Precinct 5 Judge Nick Chu presides over court in 2018. GABRIEL C. PÉREZ / KUT Texas is chasing its tail when it comes to collecting court fees and fines, a new study … Continue reading →

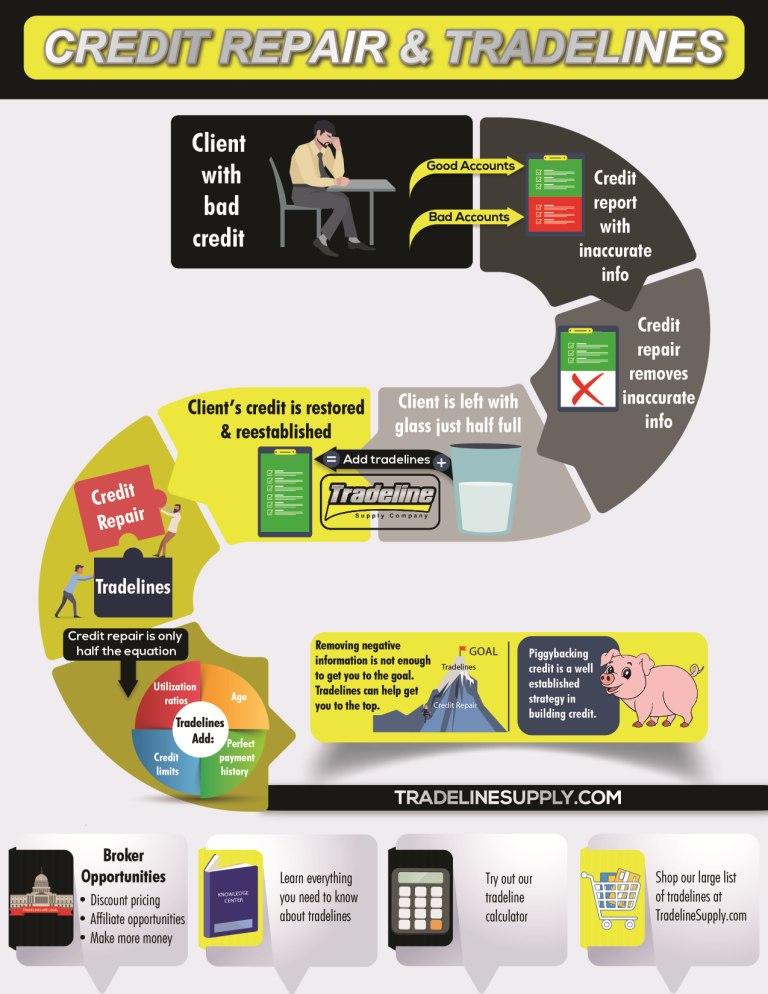

Perhaps the title “Credit Repair vs Tradelines” is not entirely accurate, but this is a common way that many consumers think of the two industries and even many credit repair companies as well. In truth, as our infographic illustrates, the two services really go hand-in-hand.

However, there are several differences that we will highlight in order to understand the full range of credit-related options. Be sure to check out our article below the infographic for all the details.

What Is Credit Repair?

The term “credit repair” can have different definitions depending on who you ask. Generally, however, credit repair is considered to be the process of mending poor credit that is a result of errors in your credit report or identity theft. This is accomplished by disputing inaccurate information in your credit file with the credit bureaus, who will investigate the claim and take appropriate action.

For example, if you have collections on your credit report that are being reported with inaccurate information, you can dispute the collection account and have it updated or removed from your credit report.

Sometimes people also use the term credit repair to mean fixing bad credit in general, using traditional methods such as bringing all accounts current and paying down debts.

For those who are seeking credit repair services through a company, you are probably interested in the process of repairing bad credit by disputing inaccurate negative information in your credit file. If your credit score is lower than the average range, going to a credit repair business may seem like an appealing option.

However, keep in mind that credit repair has its limitations. Since credit repair services focus on removing information from your credit file, once that is accomplished, there may not be much left in your file to show that you have a credit history at all. This is especially true of questionable credit repair companies who use dishonest methods to aggressively “sweep” your credit file of legitimate information.

In order to truly improve your credit score, it is important not only to remove inaccurate negative information but to also work on rebuilding your credit.

Credit repair focuses on removing inaccurate information from your credit report.

Tradelines vs. Credit Repair: What’s the Difference?

Addition and Subtraction

As we discussed above, credit repair can be thought of as the process of removing negative information from your credit report. In contrast, tradelines add information to your credit report.

A tradeline is simply any account in your credit file, so adding tradelines by definition bulks up your file. This can be helpful for people with short or thin credit histories, or those who are recovering from a period of bad credit and trying to rebuild their credit.

A short credit history means the age of your credit file is not very long, while a thin credit history means you have only a few accounts in your credit profile, if any. Credit scoring models factor in both the length of your credit history and your mix of credit, so having a thin or short credit file will likely result in a lower credit score rating.

Being added as an authorized user to tradelines that are in good standing and have a higher age (known as “seasoned” tradelines) could improve both of these factors by increasing your length of credit history and diversifying your mix of accounts.

In addition, seasoned tradelines for sale from a reputable company will have perfect payment histories and relatively low utilization ratios, which impact important components of your credit.

Tradelines can post to your report quickly, while the credit repair process may take longer.

How Long Does Credit Repair Take to See Results?

The credit repair process typically takes 1-6 months or longer, depending on how many disputes you need to make. Once you submit your disputes to the credit bureaus, they have 30 days to research the dispute and 5 more days to respond once they have completed the investigation. Sometimes, additional information may be needed, which can add more time to the process.

If you have a lot of errors to dispute, you may have to submit them a few at a time, which is why getting results can take several months.

Tradelines, however, can post to your credit report in as few as 11 days, and sometimes even faster. It just depends on the reporting period of the tradeline you are adding.

How Much Does Credit Repair Cost?

The cost of credit repair services can vary widely depending on the company, which services you need, and how long the process takes. Many credit repair organizations charge a monthly fee for their work in addition to an initial fee for pulling your credit reports. Typically, the monthly fees range between $60 to about $100 per month for basic credit repair services. [Disclosure: This article contains affiliate links.]

Purchasing tradelines, on the other hand, usually involves paying a one-time fee (unless you choose to extend the tradeline for additional time).

Is Credit Repair Worth It?

If you have bad credit, paying for a credit repair service is an option that you may want to consider, especially if you have a lot of errors on your credit report or if you have been the victim of identity theft and you need some help disputing fraudulent accounts.

If you do decide to hire a credit repair service to help you clean up your credit, make sure you research each company thoroughly and choose a legit credit repair company. Unfortunately, the industry has not earned the best reputation. Be sure to know your rights laid out by the Credit Repair Organizations Act (CROA) so you can protect yourself from being taken advantage of by shady credit repair companies.

Not everyone needs the help of a credit repair company to begin with. If you have one or two simple errors on your credit report, you may feel that you will be able to go through the credit repair process on your own and have those errors successfully removed or updated.

To answer the question of whether paying for credit repair is worth it, you’ll have to take a look at your credit report and decide whether the damage is extensive enough to warrant hiring a professional credit repair service or whether you want to try DIY credit repair.

How Credit Repair and Tradelines Work Together to Fix Your Credit

Credit repair and tradelines naturally go hand-in-hand. In one sense, tradelines pick up right where credit repair ends. Again, credit repair helps to “clean up” credit and tradelines help build or re-establish positive credit history.

One really should not exist without the other; the two techniques are most effective if done in tandem. Since credit repair removes information from your credit file, it may be necessary to add positive information to your file in the form of tradelines in order to truly rebuild your credit.

Tradelines can help to build or rebuild credit.

Buy Tradelines or Fix My Credit: Which Should I Do First?

It does not necessarily matter which one comes first. Both can exist at the same time.

However, if you have bad credit due to inaccurate derogatory information on your credit report, those variables will have an impact on your overall credit picture and could lead to tradelines having a diminished effect. In this case, the most effective course of action would be to repair your credit before adding tradelines.

On the other hand, it is never a bad time to have good things on your credit report. The timing of which strategy should come first ultimately depends on your individual situation and your own timeline.

For example, some credit repair programs take quite some time to accomplish. As we mentioned, is not uncommon for certain credit repair programs to take many months to complete. In these cases, tradelines may fit in at any given time during the credit repair process.

Credit repair and tradelines work best when used together as part of your overall credit strategy.

Why Don’t All Credit Repair Companies Offer Tradelines?

Surprisingly, not all credit repair companies sell tradelines or even know about tradelines. Sometimes tradeline companies are seen as competition to credit repair businesses because clients may end up spending money on tradelines as opposed to credit repair services.

However, as we have seen, credit repair works best when paired with tradelines. The best credit repair companies will provide you with all of the information and options that you need to make an informed decision about your financial future.

Conclusion

While tradelines and credit repair can both be effective in improving your credit, they are not the same thing. Rather, they are complementary strategies that work best when used together.

Don’t mistake tradelines for credit repair—think of tradelines as a way to build or re-establish credit. The best course of action for your credit is to evaluate your own unique situation and ask how tradelines can complement your credit repair strategy.

The House Financial Services Committee passed 8 bills, according to an announcement from Rep. Maxine Waters today: The Ending Debt Collection Harassment Act of 2019 (H.R. 5021), a bill by Representative Ayanna Pressley (D-MA), to amend the Fair Debt Collection … Continue reading →

The Department of Revenue team created last year to recoup millions owed to R.I. has so far recovered $196K. It’s been slow going for Rhode Island’s new team of state debt collectors. The Central Collections Unit, created last year to … Continue reading →

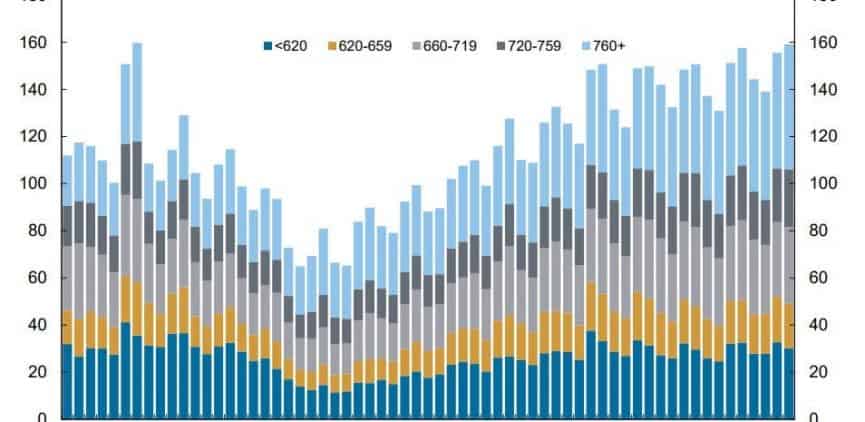

Let’s dive into some stats and charts from the New York Fed Third-Quarter Report on Household Debt and Credit. Key Points Aggregate household debt balances increased by $92 billion in the third quarter of 2019, a 0.7% increase, and now … Continue reading →

On November 4, the Second Circuit Court of Appeals in Dow v. Frontline Asset Strategies affirmed the September 24, 2018 Order of the United States District Court for the Eastern District of New York, which granted defendant Frontline’s motion for … Continue reading →

Q. I started trying to improve my credit a few years ago with credit cards but my job and an unexpected pregnancy led to nonpayment and defaulting on all of those accounts. How do I start rebuilding my credit?

Dear Reader,

The general strategy to rebuild your credit should include repaying your debts and getting a secured credit card to start developing new credit. This road is not always straight forward because your strategy will depend on your debts and your current financial situation. I suggest you start by determining how much you owe and to whom. You can get these details reviewing your credit reports (free at www.annualcredit.com) or contacting your creditors. Then, create a budget to determine how much income you’ll have to allocate toward a repayment plan.

While you are repaying your debts, you can apply for a secured credit card. These cards work like regular credit cards. The main difference is that you are required to make a security deposit when you open the account. Many banks offer these cards and have different features. Review them carefully, just make sure they report to the credit bureaus and that you understand any associated fees, if any. Once you have your secured credit card, use it strategically—make full, on time monthly payments and only use 30% of your available credit or less.

During the rebuilding process, sometimes it is hard to know what to do first. If you think you need extra help, contact an NFCC-certified credit counselor. A nonprofit counselor can provide the guidance you need so that you can focus on what’s really important– like becoming a mom. Help is nearby. Good luck!

Sincerely,

Bruce McClary, Vice President of Communications

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

US households are now sitting on a record $14 trillion in mortgages, credit cards, student loans and other forms of debt. Household debt ticked up 0.7% during the third quarter, the New York Federal Reserve said on Wednesday, continuing a … Continue reading →

The percentage of recent mortgage borrowers with subprime credit scores still resides in the single digits, but nearly doubled what is was in 2013, according to TransUnion. The share of home loans made in the second quarter to borrowers with … Continue reading →

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.