In Heredia v. Capital Mgmt. Servs., L.P., No. 19-1296, 2019 U.S. App. LEXIS 33444, at *4 (7th Cir. Nov. 8, 2019), the Court of Appeals for the 7th Circuit held that a debt collector’s reference to the possibility of issuing … Continue reading →

By the end of the Senate Judiciary Committee’s discussions, there were three possible ideas for reform proposals for the next legislative session: conversion of outstanding costs to civil debt, improved specialization of hearings to determine ability to pay and an … Continue reading →

123RF Payday loans have been such a blight on communities overseas, many countries have moved to cap the interest and fees they change. New Zealand is finally following suit. The next battle in the war against high-cost lenders was the fight … Continue reading →

CU organizations back legislation to exclude loans to veterans from the credit union MBL caps. (Source: Shutterstock) Two senators—one Republican and one Democrat—on Tuesday introduced legislation that would exclude loans to veterans from the credit union Member Business Loan cap. … Continue reading →

Q. My husband is 67 years old and doesn’t want to plan for retirement or even share his financial info with me. He doesn’t plan on retiring but he will have to stop sooner or later! Who can I speak with that can offer advice, a link to resources on this topic and/or next steps? Thank you in advance!

Dear Reader,

If your husband is not willing to share his financial information with you, it is possible that the same would be true with a financial advisor or a credit counselor. So, you have to plan with what you’ve got. In this case, relying on your husband’s Social Security benefits (if he is not collecting it already) to plan for the future.

If your husband continues to work beyond his retirement age, he will get the most out of his benefits. He could increase his Social Security income by 8% each year he continues to work until age 70. Married couples have more options to claim benefits, but you need to be informed to make the right choices and avoid losing some of your benefits. For more information about your benefits and options, create an account on the Social Security website to get all the details.

In addition to his Social Security income, you have to factor in all of your expected retirement income, plus any assets you have on your own or as a couple. Knowing where you stand can prepare you to avoid steep taxes and establish a realistic picture of what your income would be in the future. With this information, you can create a budget to determine how much money you’ll have to cover your living expenses during retirement. Share it with your husband so that he has a realistic idea of what the future can hold. He may be more willing to cooperate and start saving for the future. And if necessary, start streamlining your budget today. The sooner you make adjustments, the better. Good luck!

Sincerely,

Bruce McClary, Vice President of Communications

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

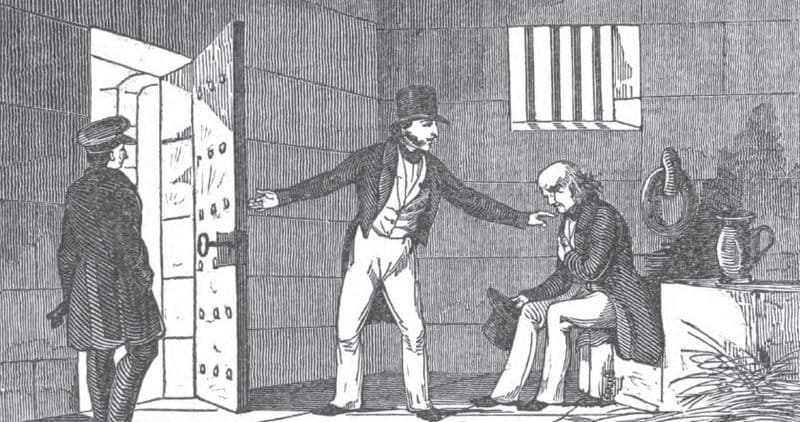

Nov 12, 2019 21 Min read time An American colonist being released from debtors’ prison. Image: Wikimedia Moral thinking about debt has fluctuated throughout U.S. history. Today’s calls for cancellation suggest it may be poised for transformation once again. “I wanted … Continue reading →

Bad credit is something we all fear, but what is actually considered poor credit and how could it affect you? In addition to explaining what bad credit is and why you need to avoid it, we’ll also provide some strategies in this article to help you fix bad credit.

What Is a Bad Credit Score?

The definition of “bad credit” varies depending on which credit scoring system you are talking about. Since FICO 8 is the scoring model most widely used by lenders, we will focus on FICO when discussing the question of what is considered bad credit.

The FICO 8 credit scoring system assigns consumers a number to represent their creditworthiness, with the lowest credit score possible being 300 and the high end of the scale being 850.

A high credit score shows lenders that they can be fairly confident that a consumer will repay debts because they have demonstrated responsible behavior when it comes to credit in the past.

A low credit score, on the other hand, means that someone represents a higher risk to lenders because they are thought to have a higher probability of defaulting on a loan.

According to Credit Karma, a FICO score between 300 to 579 is considered a poor credit score, while a fair credit score is between 580 and 669. In contrast, an excellent credit score is between 800 and 850.

Credit scores between 300 and 579 are considered poor credit.

What Gives You Bad Credit?

As we mentioned, a bad credit score means lenders perceive you as a high-risk borrower. Therefore, what causes bad credit is poor management of credit and risky behaviors that indicate you may have a higher probability of default.

For example, being late on payments or missing payments altogether can really hurt your credit because payment history is the most important factor of a credit score.

High credit card utilization can lead to bad credit. Photo by Natloans

What causes bad credit specifically? Here are some more examples:

Late or missed payments

Defaulting on a loan

Charge-offs Collection accounts

Judgments

Settlements

Bankruptcy

Foreclosures or repossessions

Maxed out or high-utilization credit cards

Too many inquiries at one time

Too much new credit

Sometimes people have bad credit because of things they can’t control, like having a medical emergency that leads to huge hospital bills that they can’t afford to pay. In fact, the majority of consumer debt in collections is medical debt, according to Magnify Money.

Bad Credit Loans

If you have bad credit, you’re likely going to have a hard time getting loans with favorable terms or possibly even getting approved for a loan in the first place. Since a bad credit score represents a high risk for the lender, loans for people with poor credit typically have higher interest rates and may require collateral or a down payment—if the lender is willing to approve the loan at all.

Personal Loans for Bad Credit

Payday loans can come with interest rates of up to 400%. Photo by Aliman Senai.

Personal loans for bad credit are few and far between. Usually, at least fair credit is needed to be considered for a loan. Bad credit loan lenders may charge very high interest rates since they are taking on a lot of risk by lending money to someone with poor credit. These higher interest rates may translate into thousands of dollars of additional interest payments over the term of a loan.

Very bad credit loans such as payday loans often have astronomical interest rates of up to 400%, which makes it nearly impossible for many consumers to get out of debt.

Bad Credit Car Loans

Bad credit auto loans, also known as subprime auto loans, are often considered “second-chance” loans because they are typically the next option for those who have been rejected for traditional auto loans. Although there is not necessarily an official dividing line between which credit scores are considered prime and subprime when it comes to auto loans, credit scores below 620 tend to be considered subprime.

Car loans for bad credit, similar to personal loans for bad credit, are associated with much higher costs than prime auto loans. Since lenders of second-chance auto loans are taking on additional risk, these loans often have significantly higher interest rates and more fees than auto loans for consumers with good credit. Additionally, car loans for bad credit may come with penalties for paying off the loan early.

Bad credit car loans can have triple or more the interest rate as prime auto loans. Photo by QuoteInspector.com.

According to Investopedia, “While there is no official subprime auto loan rate, it is generally at least triple the prime loan rate, and can even be five times higher.”

Credit Cards for Bad Credit

If you have bad credit, your options for getting a credit card will be limited, and you will most likely not be able to get the perks associated with premium credit cards, such as low interest rates, high credit limits, and rewards. Credit cards for poor credit may also come with annual or even monthly fees.

Subprime credit cards often require you to make a deposit with the lender as collateral. These cards are known as secured credit cards since they are secured by your deposit, which the lender can keep if you fail to make payments on the card. Sometimes, the lender may be willing to switch you to an unsecured card after you have shown a history of consistent on-time payments.

As we’ve seen with loans for bad credit, credit cards for bad credit, both secured and unsecured, will likely have high interest rates, sometimes as high as 30% or more.

How to Fix Bad Credit

Having a bad credit score is expensive. It makes getting any kind of credit more difficult and more costly because bad credit lenders tack on high interest rates and fees to compensate for the higher financial risk of poor credit loans.

Bad credit doesn’t just dramatically increase the cost of credit. It can also affect other aspects of your life, such as your insurance premiums, your ability to find housing, and even your job, since many employers now check prospective employees’ credit reports. Therefore, most people with bad credit want to fix it as soon as possible.

Here are some strategies that you can try if you need to fix bad credit.

Credit Repair

If you have bad credit as a result of identity theft or extensive errors on your credit report, you’ll likely need to undergo credit repair in order to clean up your credit file.

Some people opt to try their hand at DIY credit repair, while others may prefer to hire a trusted credit repair company to get help with the dispute process and potentially faster results. [Disclosure: This article contains affiliate links.]

Either way, it’s important to be aware of best practices when disputing credit report errors. It’s best to submit your dispute by sending a letter along with documentation to verify your identity and support your claim. Trying to dispute errors online or over the phone may not yield the best results.

In addition to disputing inaccurate information with the credit bureaus, it’s also important to contact the company that is furnishing the data so that the error doesn’t get reported again in the future.

Rebuilding Credit

Improving bad credit takes time and patience. While credit repair companies may claim to have tactics that can boost your credit fast, the reality is that these tactics are usually limited to removing inaccurate information from your credit report. If you remove everything from your credit report, what are you left with?

The best way to fix bad credit, beyond correcting inaccuracies, is to rebuild it with more positive credit history over time. In other words, you need to add more positive accounts to your credit profile and keep them in good standing while they age. At certain age levels, these accounts should begin to boost your credit profile with that positive payment history.

Rebuilding credit with positive credit history helps to fix bad credit.

One option that can help people re-establish credit is opening a credit-builder loan, which works in the reverse order of a traditional loan. Instead of receiving the loan amount up front and then making payments to the bank to pay off your debt, with a credit-builder loan, you make all the payments first and then receive the funds after you have finished paying off the loan. Since these loans are much less risky for lenders, they can be offered to those struggling with bad credit or lack of credit history.

Generally, though, building credit by opening new accounts can take at least two years to see much of a positive effect. The best way we have seen to bypass this two-year waiting period is by piggybacking on the good credit of others.

Have you been affected by bad credit? What did you do about it? Tell us your story in the comments.

Congressional lawmakers have introduced scores of bills this legislative session to help veterans across the country, including one to end the so-called widow’s tax and another to extend pensions to Medal of Honor recipients’ families. Speaking at the dedication of … Continue reading →

On November 4, the U.S. Court of Appeals for the Second Circuit affirmed a district court’s decision that a debt collector does not violate the FDCPA by sending notices to consumers that do not clarify that a debt is static. … Continue reading →

Add HMBradley to the list of Los Angeles-based startups looking to shake up the world of high finance typically dominated by East Coast giants with names like JPMorgan Chase, Citigroup, Morgan Stanley and Goldman Sachs. The new Santa Monica, Calif.-based … Continue reading →

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.

Bruce McClary is the Vice President of Communications for the National Foundation for Credit Counseling® (NFCC®). Based in Washington, D.C., he provides marketing and media relations support for the NFCC and its member agencies serving all 50 states and Puerto Rico. Bruce is considered a subject matter expert and interfaces with the national media, serving as a primary representative for the organization. He has been a featured financial expert for the nation’s top news outlets, including USA Today, MSNBC, NBC News, The New York Times, the Wall Street Journal, CNN, MarketWatch, Fox Business, and hundreds of local media outlets from coast to coast.