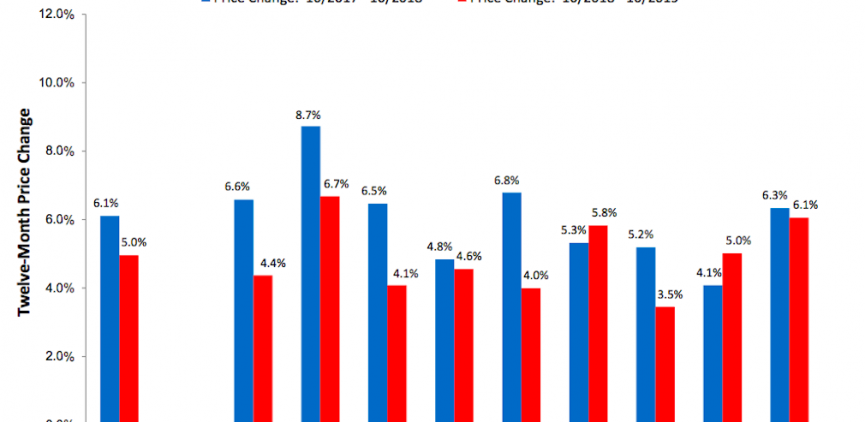

Home prices increased in October, rising only 0.2% from the previous month but up 5% from 2018, according to the latest monthly House Price Index from the Federal Housing Finance Agency. The FHFA monthly HPI is calculated using home sales price information from … Continue reading →

If you notice an error on your credit report, it’s in your best interest to get it fixed as quickly as possible. About 25% of Americans have an error on their credit reports, according to a 2012 study by the … Continue reading →

Photo: Getty In the debt collection industry, collectors are a company’s front-line offense and defense. They bring in revenue and are the first point of contact for debtors. The higher the productivity of your agents, the higher the income of … Continue reading →

The Texas collection agency calling patients about Ellwood City Medical Center debt is Better Business Bureau-accredited, but many remain uncertain whether they should pay the company. ELLWOOD CITY — The Texas collection agency calling patients about Ellwood City Medical Center … Continue reading →

If you don’t have any cash on you, walking by an ATM without enough money in your bank account to cover a withdrawal can be frustrating

Many credit cards, however, can be used to withdraw cash from an ATM, whether it’s your bank or not. Just like that, you can have some money in your pocket.

But don’t jump up to the first ATM you see and take out some cash with your credit card just yet. Called cash advances, these withdrawals are actually you borrowing cash on your credit card and must be repaid — usually with high fees and interest rates.

You first need to check that your credit card will work in an ATM.

Either call your credit card company or check the cardholder agreement that came with your card.

Look for the sections on “Cash Advance APR” and “Cash Advance Fee,” which is listed with dollar figures or percentages charged are a sign that your card can be used at an ATM.

Your credit card statement may list a cash advance credit line or cash advance credit limit, which is the maximum amount of cash you can take out. The credit limit for cash advances is usually smaller than your credit limit for regular purchases.

To use your credit card at an ATM, you’ll need to find or set the PIN that’s tied to your credit card. You may have gotten it when the card came in the mail. You may have to request it from the credit card issuer by logging into your account online or calling the phone number on the back of the card. It might take seven to 10 days to set up the PIN.

You may get charged a fee for using an ATM that is outside the network linked to the credit card. Check with your credit card provider or your bank to find out how much it is and if you can avoid it.

Is a Cash Advance From a Credit Card Bad?

Short-Term Problems of Cash Advances

Fees are the first thing you’ll pay on a cash advance. They’re usually based on the amount of cash you borrow, such as $10 or 5 percent of the amount, whichever is greater. That equates to a $10 fee for borrowing up to $200, or 5 percent of the amount borrowed if it’s more than $200.

Immediate interest charges are another reason to avoid cash advances. They don’t have grace periods — as your normal credit card purchases do for about a month— and the credit card company will start charging you interest on a cash advance as soon as you borrow the cash.

Cash advances have high APRs that are much higher than normal purchases. Expect to pay 25 percent interest on a cash advance, again, without a grace period.

Long-Term Problems of Cash Advances

High interest rates can turn into long-term problems if you don’t pay the cash advance off soon, but there are also other problems with cash advances that can follow you for years.

The first is that your credit card company may flag you as a risky borrower. Creditors consider people who use cash advances as being desperate for money, especially if they do a few of them.

Such risky behavior with your money can lead to you being unable to get higher lines of credit or good terms with the bank that gave you the cash advance. Your credit card’s interest rate could rise or your account closed.

A second long-term problem is that cash advances add to your credit card debt and is shown on your credit reports. If you already have high balances on your credit cards when compared to your total available credit, a cash advance can lower it more.

The more credit card debt you have compared to your total available credit — called credit utilization — the more it can hurt your credit scores. If you already have high balances on your credit cards, a cash advance can make raise your credit utilization rate and make you a bigger risk to creditors.

The higher the credit utilization rate, the greater the risk that you’ll default on a credit account within the next two years, according to FICO, a credit scoring company.

“Amounts owed” make up 30 percent of a credit score, and using more than 20 percent of the credit available to you is considered risky.

How to Avoid Some Cash Advance Fees

Interest charges on cash advances are unavoidable, but some fees can be eliminated through a few options.

If you have a credit card from Discover, it allows up to $120 to be borrowed in cash at checkout when you’re buying something. The money is categorized as a purchase instead of a cash advance, so you’ll avoid bank and transaction fees.

Your regular APR applies to the cash you get and there are no hidden fees, according to Discover. Called “Cash Over,” the transactions are limited to $120 every 24 hours with no monthly limit, though your local store may have allow less money to be cashed out over the purchase amount and may limit the number of times you can withdraw cash.

If you’re having difficulty finding an ATM linked to your bank so you can avoid ATM fees for withdrawing cash from your checking account through a machine that isn’t part of your bank’s network, find a bank that covers ATM fees at other banks. Some brokerage accounts offer free ATM use for customers, so setting up a brokerage account may be worthwhile.

If you’re really strapped for money, consider a balance transfer credit card. It can allow you to transfer a credit card balance and then pay it off without any interest charges for a year or more.

However, there are drawbacks to the cards, and fewer credit card companies are offering them. Be aware of the terms before switching to one.

If you decide to get a cash advance through your credit card, try to pay it back as soon as you can. Interest will start accruing immediately, and having debt get out of control will only add to your cash-flow problems.

Lara Briehl had a desperate client who was itching to accept an offer. The man was struggling to pay his bills, and an online lender had offered him a personal loan to pay off some 10 credit cards. Accepting, he … Continue reading →

This article was produced in partnership with ProPublica, a nonprofit newsroom that investigates abuses of power. AL.com this year is a member of the ProPublica Local Reporting Network. ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up … Continue reading →

By Jay Hancock, Kaiser Health News The American Hospital Association, the biggest hospital trade group, says it promotes “best practices” among medical systems to treat patients more effectively and improve community health. But the powerful association has stayed largely silent … Continue reading →

Losing something can put you in a panic. If it’s a credit card, losing it can be especially troublesome.

A thief who steals it or someone finds it could ring up charges on your credit card, which you may have to pay some of if you don’t report it lost soon enough.

And even if you get all the money back from credit card fraud, your credit score could be temporarily hurt if a thief quickly runs up a lot of charges on your card.

Worse than that is if someone uses the information from your lost or stolen credit card to create a fake identity in your name and uses the information to open a new account in your name.

People reported losing $1.48 billion to fraud in 2018 according to the Federal Trade Commission.

The first thing you should do when realizing your credit card is lost or stolen is to call the issuer and report it missing. We’ll get into how to do that later, but the simple thing to do is to call ASAP to report it missing.

The reason is the sooner you report it missing, the more you’ll be protected from being responsible for fraudulent charges and the chance that your information can be used by an identity thief. If the credit card is canceled, a thief can’t use it to buy things or create a new card.

Under federal law, if you report a credit card as missing before it’s fraudulently used, you’re not responsible for any unauthorized charges.

However, if a card is used by a thief before you report it missing, you could be responsible for some of those charges. The maximum liability amount is $50 under federal law. Some credit cards offer zero liability.

So if your missing card is still used after you report it missing, you won’t be liable for the charges you didn’t authorize. If your card wasn’t stolen but your credit card number was, you aren’t liable for any unauthorized charges.

How to Report a Missing Credit Card

Your credit card statement has instructions on how to report a missing card. Most companies have 24-hour, toll-free numbers. If your spouse has the same credit card, the phone number will be on the back of their card.

Call your issuer as soon as you realize your card is missing. Even if you think you might have misplaced it, you can still call your credit card company and ask it to suspend charges immediately but temporarily until you can determine if the card is really missing or if you’ve left it in the car or find it elsewhere.

Once you’ve determined that the card is gone, file a report by phone and follow the credit card company’s instructions. Also follow up with a letter to the company, providing your account number, date you noticed the card missing, and the date you filed the report.

You should check your card statement carefully for transactions you didn’t make. Report them to your card issuer as quickly as possible.

After you’ve reported a missing card, your card issuer will send you a new card, usually within a few days and sometime overnight.

If you have automatic payments tied to your credit card, such as for a phone bill, call your creditors or go online and update your accounts.

What To Do If You Lose Your Debit Card

If you lose a debit card, the consequences can be a lot worse, so you need to call your bank as soon as possible to report it lost or stolen.

Debit cards, which pull money immediately out of your checking account when used, must be reported missing within two business days of learning of their disappearance so that your liability is limited to $50.

Longer than that and up to 60 days after your next bank statement is sent to you, and you’re responsible for up to $500 in losses. Wait more than 60 days after your statement is sent to you, and all losses are your responsibility.

Thieves can quickly drain accounts linked to debit cards. Even if you quickly report the card lost, it can take awhile to get your money back from the bank.

Other Hassles of Lost Credit Cards

With the $50 liability limit set by federal law on missing credit cards, you may assume it’s OK not to report it missing. Not true. If you don’t report it missing, other problems could crop up.

Thieves who steal credit cards often start using them as quickly as they can so they can buy things before the card is canceled by the bank. But if it’s not reported missing soon, they can keep ringing up charges that you’ll have to dispute with your credit card company.

If you have a good credit card company, they’ll notice the fraudulent charges and alert you immediately. But if more purchases accumulate, you’ll spend more time trying to fix things.

A lot of fraudulent charges could also hurt your credit score temporarily. Once the fraud is found and resolved, your score should return to normal.